Economic Weekly 11/2026, March 20, 2026

Published: 20/03/2026

Table of contents

The race for strategic raw material stockpiles is accelerating

616 the total level of oil stockpiles held by IEA member states, expressed in days of net imports

USD 12 billion the planned financing for Project Vault, the U.S. strategic reserve of critical minerals

92% the estimated share of China in global copper stockpiles

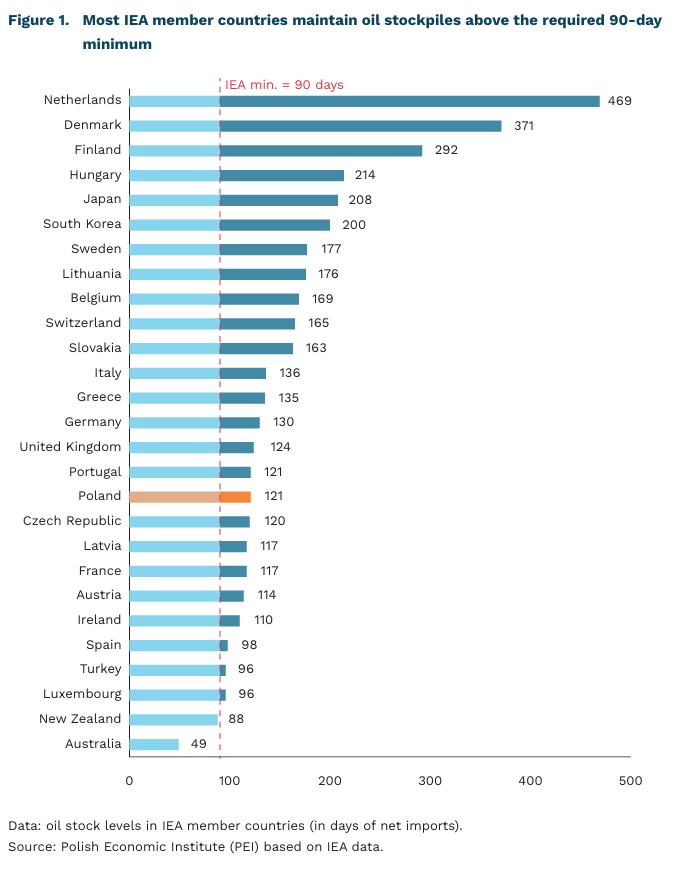

In response to disruptions in the oil market caused by the paralysis of shipping through the Strait of Hormuz, the International Energy Agency (IEA) announced on 11 March 2026 the release of 400 million barrels. This corresponds to roughly four days of global oil production. Of this amount, 172 million barrels are to come from the U.S. Strategic Petroleum Reserve.

The Israeli–U.S. strike on Iran has underscored the importance of strategic oil reserves, which include both public stockpiles and mandatory reserves held by fuel companies. The United States, which has been a net exporter of crude oil and petroleum products since 2020, holds reserves amounting to 411 million barrels, equivalent to 125 days of net imports. In Europe, stock levels remain above the IEA-required minimum (90 days). Germany, France, and Poland, for instance, maintain 130, 117, and 121 days of net import cover, respectively. South Korea and Japan – countries with virtually no domestic production and heavily dependent on Middle Eastern oil imports – hold reserves equivalent to 200 and 208 days of net imports, respectively.

In the case of China, which remains outside the IEA system, an Institut Montaigne report estimates stock levels at 140-150 days, including underground storage. Half of these reserves (750 million barrels) are held by four major Chinese oil companies. Other Asian countries are in a more constrained position: Thailand (98 days), India (74 days), the Philippines (50-60 days), Indonesia (65 days), and Vietnam (20 days), although these figures are not fully comparable methodologically with the IEA reporting system.

Countries are increasingly working on analogous solutions for other raw materials, particularly critical minerals. On 2 February 2026, the U.S. administration announced Project Vault, intended to become the largest civilian strategic minerals reserve in U.S. history. Its financing is to follow a public–private model, comprising USD 10 billion from the Ex-Im Bank and USD 2 billion from the private sector. On 12 January 2026, Australia, in turn, announced the creation of a Critical Minerals Strategic Reserve worth AUD 1.2 billion, initially covering antimony, gallium, and rare earth elements. The Australian model does not rely on physical stockpiling, but rather on securing rights to domestically extracted resources and reselling them in times of crisis. Japan has also maintained a system of critical minerals stockpiling since 1983. In the European Union, at the end of 2025, the European Commission proposed a joint purchasing mechanism and announced the creation of the EU Critical Raw Materials Centre, which is expected to support the development of strategic reserves of critical raw materials. However, the effectiveness of these efforts is constrained by China’s dominant position in global critical minerals value chains.

China holds some of the largest stockpiles of strategic metals in the world. It accounts for nearly 92% of global copper inventories, reflecting the scale of demand from the Chinese economy – China is estimated to be responsible for close to 60% of global consumption of this resource. Iron ore stockpiles are estimated at 142 million tonnes, aluminium at 650-900 thousand tonnes, nickel at around 160-200 thousand tonnes, and cobalt at approximately 10 thousand tonnes. This dominance is the result of a long-term strategy to build resource security, including through international engagement. Between 2000 and 2021, China allocated nearly EUR 54.7 billion to financing mining projects in more than 20 developing countries, primarily focused on cobalt and copper extraction, and to a lesser extent on nickel and lithium.

Dominik Kopiński

The number of people working exclusively under contract of mandate is growing

1.5 million people in Poland were employed exclusively under contract of mandate agreements in September 2025

438,000 foreign nationals were employed exclusively under contract of mandate agreements in September 2025

37% of people working exclusively under contract of mandate are either young or of retirement age

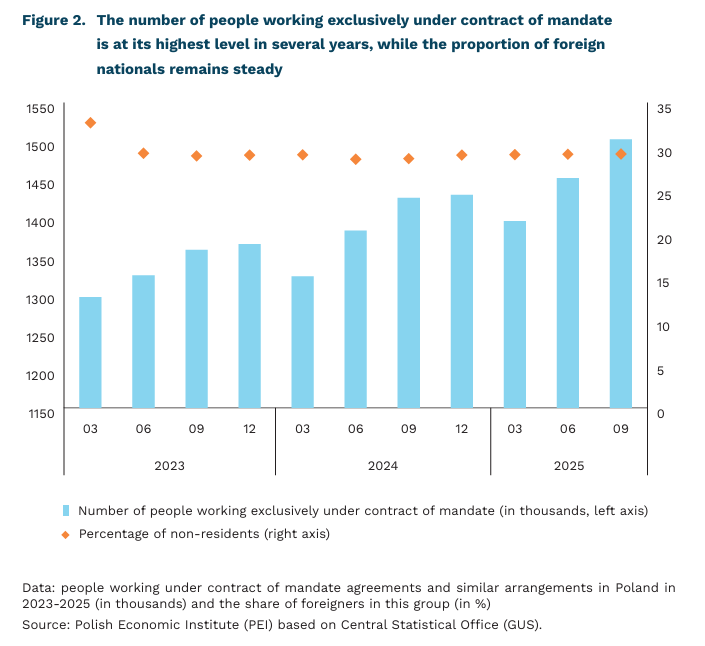

As of the end of September 2025, the number of people in Poland employed exclusively under contract of mandate agreements or similar arrangements stood at 1.5 million. This is the highest figure since the Central Statistical Office (GUS) began publishing results based on administrative data. On an annual basis, as of the end of the third quarter of 2025, 5.4% more people were working under such contracts. Since GUS began publishing this type of data – i.e., since the beginning of 2023 – the group of people working exclusively under contract-for-service or similar arrangements has increased by 207,000 people from 1.3 million.

More than one-third of those working exclusively under contract of mandate agreements are either young people or those of retirement age. Both groups – that is, people under 26 and those who have reached the age of 65 for men and 60 for women – each accounted for just over 18% of all workers employed solely under contract-for-service or similar agreements. Together, this accounted for a 37% share. The largest cohort consisted of 26-year-olds – numbering nearly 44,000 people (the only group to exceed 40,000).

The proportion of foreigners among those working exclusively under contract of mandate agreements or similar arrangements remains at a similar level. According to data from the Central Statistical Office (GUS) for September 2025, foreigners accounted for 29% of all workers in Poland employed exclusively under contract of mandate or similar arrangements. This structure has remained relatively stable since 2023. Overall, out of the 1.1 million foreigners working in Poland, 437,400 were employed exclusively under contract of mandate agreements and similar arrangements. This represents a 7.4% increase compared to September 2024 (2 percentage points higher than the overall rate for those working exclusively under such agreements).

While the number of people working under contract of mandate agreements has been rising for several years, the popularity of specific task contracts is declining. In 2025, 1.3 million such contracts were signed, which is 6.5% fewer than the previous year. This is also the lowest level since the registry for specific task contracts was launched in 2021. The number of contractors during this period decreased slightly from 337,000 to 318,000. In 2025, foreigners accounted for 6% of contractors under specific-task contracts.

Experts indicate factors limiting the role of SMRs in the development of Poland’s nuclear energy sector

3 SMRs are currently in operation around the world – one each in China, Japan and Russia

17-53 GWe of the SMRs capacity the EU plans to build by 2050

by 2030 a GE Vernova Hitachi BWRX-300 reactor in the province of Ontario, Canada is planned for commissioning; this type of reactor could also be built in Poland

Small modular reactors (SMRs) are attracting interest in light of the challenges posed by the energy transition. According to their proponents, such energy sources could enable the faster scaling up of nuclear power development worldwide due to their characteristics. Companies developing SMRs emphasise that, thanks to their relatively low power output and mass production, a reduction in investment costs will be possible, enabling them to be built or operated by private enterprises (e.g., energy-intensive industries).

However, experts in the nuclear sector point to a number of factors that could limit the role of SMRs in Poland’s energy transition, at least in the medium term. This is evident from the responses gathered during a Delphi survey conducted for a PEI report due to be published in April this year. The experts involved highlighted numerous barriers that could significantly hinder the development of SMRs in our country. Among the most frequently cited is – as in other countries – a lack of experience with the new technology (pilot projects, so-called FOAKs), which entails the risk of higher-than-expected investment costs, as well as lengthy and non-optimised administrative procedures. These factors may mean that small reactors do not necessarily gain an advantage over large-scale ones. Furthermore, the experts highlighted the unfavourable regulatory environment in the EU (compared to the conditions for renewables) and the limited capacity of domestic companies to undertake investments that are significantly more capital-intensive than those in renewables.

There are currently[2] three small modular reactors in operation worldwide – one each in China, Japan and Russia. In Western countries, the most advanced project appears to be the BWRX-300 unit under construction in Canada, which is expected to come online by the end of this decade. Its actual implementation is well underway, as construction work has already begun and the manufacturing of critical components, such as the reactor vessel, has been commissioned. At the same time, dozens of different SMR technologies are being developed globally, including the French Nuward and the British Rolls-Royce SMR. Despite the high level of interest in this technology, however, it is necessary to overcome cost, scheduling and regulatory barriers, as well as to establish an efficient supply chain, for the numerous projects currently underway to come to fruition.

In Poland, the first SMR is set to be built in Włocławek and commissioned at the start of the next decade. The investor – Orlen Synthos Green Energy – has announced plans to build at least two small nuclear units[1] in Poland with a combined capacity of 0.6 GWe by 2035. In February this year, OSGE signed an agreement with the supplier of the BWRX-300 reactor technology, GE Vernova Hitachi, to develop a Polish version of this reactor. This will enable it to be adapted to Polish regulations and safety standards, ultimately making it a reference design for all planned reactors of this technology in Poland. At the same time, work is underway at the Ministry of Energy on a roadmap for SMRs, which is intended to facilitate their development in Poland.

The EU also recognises the potential of small modular reactors and published a dedicated strategy in March this year. The strategy indicates that such energy sources will be particularly important not only in the electricity sector, but also in district heating and industry. The document emphasises that harmonisation of actions at EU level will be critical, leading to the development of a European supply chain (including fuel cycle services) and regulatory cooperation between nuclear regulatory authorities. The strategy includes f inancial support for innovative nuclear technologies (200 million EUR) and staff training through the establishment of an EU Net-Zero Academy for Nuclear Technologies. The aim of the strategy is to deploy SMRs at the start of the next decade (and to scale them up to 17-53 GWe by 2050), though it makes the achievement of this goal contingent upon the introduction of instruments in Member States to mitigate investment risk.

There are currently[2] three small modular reactors in operation worldwide – one each in China, Japan and Russia. In Western countries, the most advanced project appears to be the BWRX-300 unit under construction in Canada, which is expected to come online by the end of this decade. Its actual implementation is well underway, as construction work has already begun and the manufacturing of critical components, such as the reactor vessel, has been commissioned. At the same time, dozens of different SMR technologies are being developed globally, including the French Nuward and the British Rolls-Royce SMR. Despite the high level of interest in this technology, however, it is necessary to overcome cost, scheduling and regulatory barriers, as well as to establish an efficient supply chain, for the numerous projects currently underway to come to fruition.

- However, OSGE obtained the necessary approvals for six such units.

- As of 17th March 2026.

Wojciech Żelisko

Poland is rapidly closing the productivity gap with the EU average

34% was the cumulative increase in labor productivity in Poland between 2015 and 2025

72.1% of the EU average will be reached by Poland’s labor productivity in 2027

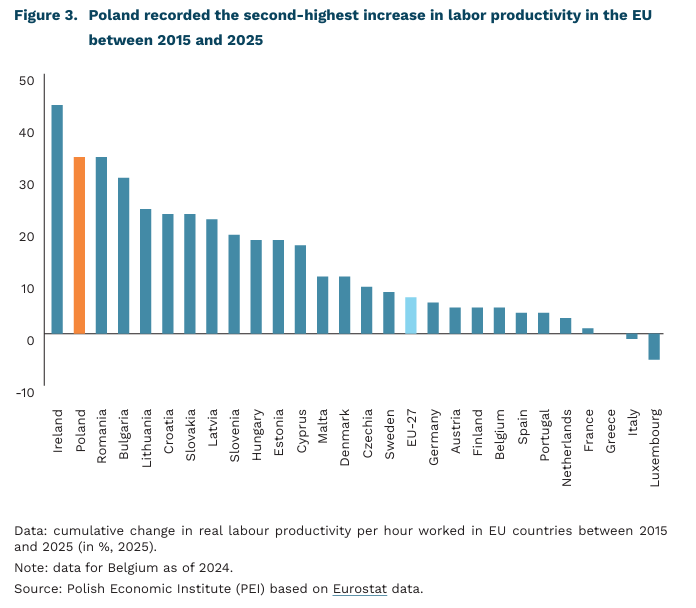

Over the past ten years, Poland has ranked 2nd in the EU in terms of cumulative growth in labour productivity. Labour productivity, measured as real GDP per hour worked, rose by as much as 34% between 2015 and 2025, which corresponds to an average annual growth rate of nearly 3%[3]. Ireland was the EU leader in productivity growth, with a cumulative increase of almost 44%. However, it should be noted that Ireland’s GDP statistics are systematically inflated by multinational corporations registered there, which leverage favourable tax regulations.

Such dynamic convergence in labour productivity in Poland is primarily driven by inf lows of foreign direct investment, rapid technology transfer and adoption, as well as the low base effect. Increasing trade openness and integration into global value chains have also played a significant role – processes that accelerated markedly after Poland’s accession to the EU. It is emphasized that this convergence has been accompanied by productivity growth across all sectors, especially those with strong export exposure.

Data on labour productivity trends in the EU show that the situation varies across countries. The cumulative increase in labour productivity in the EU between 2015 and 2025 amounted to less than 7%, corresponding to an average annual growth rate of only 0.67%. Meanwhile, countries that experienced a decline in labour productivity during this period include Italy and Luxembourg (by 1.2% and 4.5%, respectively).

Despite strong growth over the past decade, Poland is not yet a leader in labour productivity within the EU. In 2024, Poland’s labour productivity amounted to 66.4% of the EU average, placing it 4th from the bottom among EU countries. The European Commission forecasts that by 2027 Poland will reach 72.1% of the EU average in labour productivity, overtaking economies such as Portugal and Croatia.

3. An alternative measure of labor productivity is GDP per employed person. However, due to the significant variation in the prevalence of part-time work across the EU – and thus the limited reliability of this indicator – it was decided not to include it in the analysis.

Hubert Pliszka

25% of companies took steps to reduce operating costs in 2026

45% of companies plan to take steps to reduce costs in 2026

35% of service companies intend to reduce costs in 2026

68% of companies consider labour costs to be a major or very major barrier to doing business

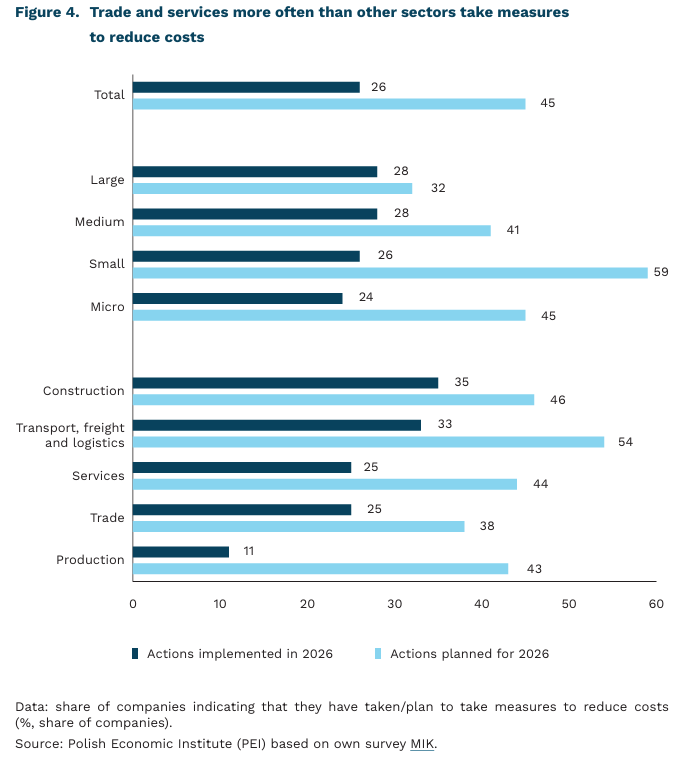

Slightly more than 25% of companies took steps to reduce operating costs in the first two months of 2026, according to the March MIK (Monthly Business Climate Index) survey. In addition, as many as 45% of companies plan to undertake such measures later this year. Cost reduction ranked second (after wage increases) among actions taken by companies since the beginning of the year, and first among actions planned for the coming months.

The sectors that most often decided to reduce operating costs were services (35%) and trade (33%). Construction and manufacturing opted for such a step somewhat less often (25% each), while transport, freight and logistics companies did so the least frequently (only 11%). As for plans for the rest of the year, the highest share of firms planning to reduce operating costs was recorded in trade (54%), and the lowest in manufacturing (38%). Cost-cutting was undertaken with a similar frequency across companies of different sizes, though large and small companies opted for it slightly more often (28% each). When it comes to plans to reduce costs, medium-sized firms stood out: as many as 59% planned to take such actions in 2026. Large firms were the least likely to report such intentions (32%).

Compared with the situation two years ago, the share of companies that have undertaken measures to reduce operating costs is significantly lower (35% in 2024 vs. 26% in 2026), although the share of companies planning such actions in the coming months remains at a similar level. Two years ago – just as this year – cost-cutting was the second most frequently mentioned action taken by companies. In 2024, it was most often reported by medium-sized and micro-enterprises, as well as companies in the transport, freight and logistics and manufacturing sectors.

The need to reduce costs in 2026 was most often declared by sectors in which labour costs make up a significant share of operating expenses. Companies have been complaining for some time about rising burdens in this cost category – labour costs have been identified as the main barrier to business activity for the past two years. In the MIK survey, with over two-thirds of companies pointing to labour costs in MIK surveys (in March 2026, this was 68% of companies). NBP data also indicate that more than 60% of entities feel wage pressure. At the same time, the MIK survey shows that companies have not cut wages (fewer than 1% of companies reduced pay), and the vast majority have not laid off employees either (only 6% of companies reduced employment), instead trying to reduce operating costs in other ways. They seek to optimise the use of existing resources, which often involves introducing process automation and making broader use of new technologies.

Anna Szymańska

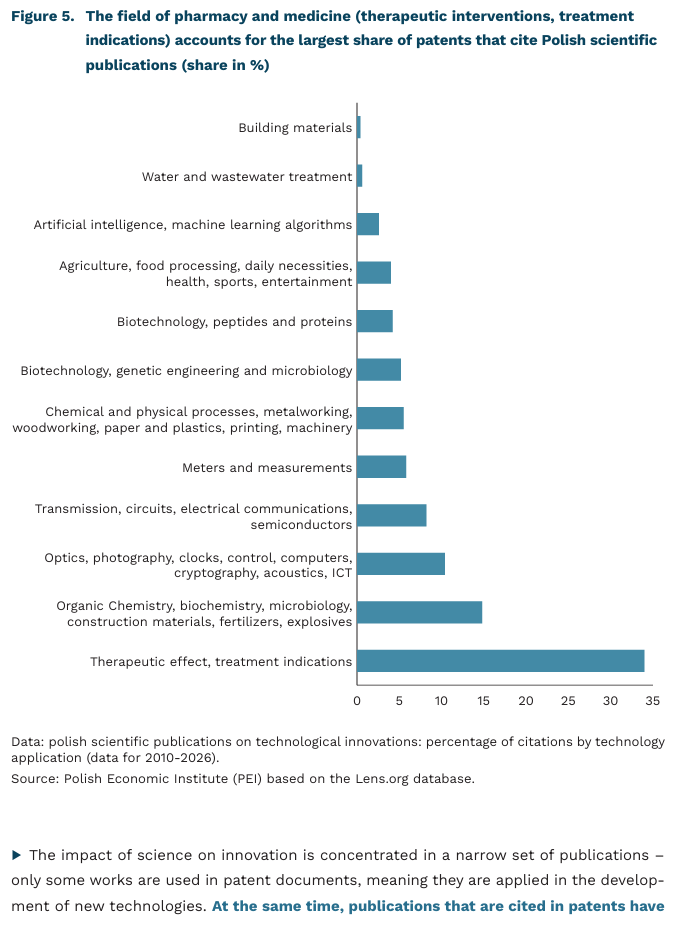

Low proportion of Polish scientific publications in patents

2.3% of Polish scientific publications have been used in patents (data from Lens.org, 2010-2026)

publications that are incorporated into patents receive an average of 2.8 patent citations

34% of patents are related to pharmacy and medicine, 15% to meters, optics, computers, and ICT, 8% to electronics and semiconductors, and 3% to AI

Of the 777,612 Polish scientific publications (i.e., those in which at least one author is affiliated with an institution in Poland), including articles in scientific journals, conference papers, preprints, and books, 17,691 were cited in patent documents[4]. This means that approximately 2.3% of publications were used as a source of knowledge to create specific solutions, which shows that most scientific output is theoretical in nature.

The impact of science on innovation is concentrated in a narrow set of publications – only some works are used in patent documents, meaning they are applied in the development of new technologies. At the same time, publications that are cited in patents have an average of 2.8 patent citations, indicating that some research results are applied in several technological solutions.

Scientific knowledge from Poland is utilized by the academic community, research institutes, and the private sector alike. Among patent holders citing publications from Poland, universities and research institutes from the United States and France predominate, as well as technology and biotechnology companies from the U.S., Germany, and Luxembourg.

An analysis of patents based on Polish scientific publications reveals a clear concentration in the fields of medicine, pharmacy, chemistry, and biochemistry. The largest group consists of patents related to therapeutic effects and treatment indications (34%). Next are technologies related to meters, optics, computers, and ICT (10%), indicating the influence of Polish science not only in medicine and pharmacy but also in technical fields. One can also observe a growing diversification of knowledge transfer pathways and the gradual integration of digital competencies into traditional research sectors.

At the same time, it is worth noting the fewer but strategic niches and specializations, including those in the fields of electronics and semiconductors (8%), as well as artificial intelligence (3%), which may have significant innovation potential. It is precisely in this direction that PIE intends to conduct further research. Their limited representation in the patent landscape may suggest that the Polish innovation system still does not sufficiently leverage the potential of more advanced technologies, which require a larger scale of investment and stronger integration with global industrial ecosystems.

4. The collection includes publications from 2010 to 2026 with at least one author affiliated with Poland. Most of the publications date from before 2022, as it takes time for them to be cited in patents. The process of developing and registering a patent is lengthy, so the most recent works do not always appear immediately in patent documents.

Magdalena Lesiak

Family university traditions influence the number of children born to graduate women in the United Kingdom

17% this is how much lower the completed fertility rate is among female university graduates in the UK whose parents did not attend university, compared to those whose at least one parent did

7.6% this is how much higher the probability of childlessness is among female university graduates in the UK whose parents did not attend university, compared to those whose at least one parent completed higher education

An increasing number of studies point to the inaccuracy or oversimplification of the claim that educated women choose not to have children or have fewer children than women without higher education. In one of the recent issues of The Economic Weekly, we wrote about Scandinavia, where the negative relationship between women’s higher education and fertility has practically disappeared, and the United States, where a positive impact of mothers’ education on children’s well-being has been demonstrated.

Results of a study conducted in the UK last year highlight another important factor that nuances the thesis about the negative impact of women’s higher education on the number of children they have. An analysis of the educational paths and fertility of 8,000 women born in 1970 showed that women without a family tradition of higher education (none of their parents attended university) had, by age 46, on average 17% lower fertility and a 7.6% higher probability of remaining childless than women whose at least one parent had attended university. The study also found that although highly educated women whose parents attended university (at least one of them) delay the decision to have their first child compared to women without higher education, after the age of 35 the number of children they have is similar to that of women without higher education. In contrast, women who are pioneers of higher education in their families do not make up this gap.

Interestingly, no differences were observed in the number of children born to highly educated women who were the first in their families to attend university and those who continued a family tradition of higher education. This means that differences in average fertility between these two groups result from a higher rate of childlessness among the former.

Analysis of comprehensive data from the British Cohort Study showed that childlessness among women who were the first in their families to pursue higher education is linked to personal factors from early life, such as self-esteem or their mother’s employment, rather than labor market conditions, financial barriers, or health status. The fertility gap (i.e., unrealized reproductive preferences) is particularly evident among women who, in early adulthood, did not express strong preferences for motherhood and whose mothers did not work.

The authors of the study note that women who are pioneers of higher education in their families face specific challenges on their education and career paths that may influence their decisions about motherhood. They often come from less affluent families, have limited access to information, are more burdened by the need to earn money while studying, and may have caregiving responsibilities toward older family members. They also face psychological strain related to social isolation and tend to receive lower pay.

The findings of this study suggest that supporting the social mobility of women pursuing higher education – particularly in balancing professional responsibilities with motherhood – may help simultaneously address declining fertility and shortages of skilled workers.

In light of the cited British study, the causes of the negative correlation between women’s level of education and fertility in Central and Eastern European countries require more advanced analysis. The mere fact of having or pursuing university degree does not provide a sufficient explanation for low fertility.

Agnieszka Wincewicz-Price