Economic Weekly 19/2026, May 15, 2026

Published: 15/05/2026

Table of contents

The population decline in Poland is greater than the Central Statistical Office (GUS) had forecast

at the end of 2025, Poland’s population stood at 37.3 million

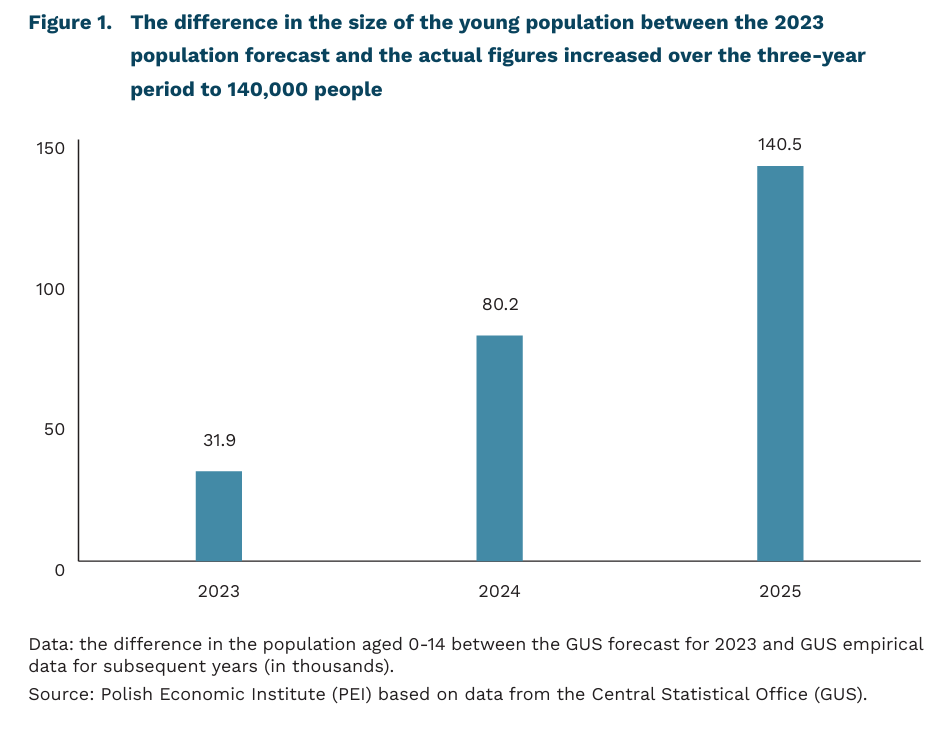

the actual figure for the number of young people in 2025 was 140,000 lower than the 2023 forecast

the total fertility rate in Poland has fallen by 0.23 over the last three years

At the end of 2025, Poland’s population was 156,000 lower than the previous year. According to the latest report from the Central Statistical Office (GUS), 37.3 million people [1] were living in the country in 2025. Consequently, Poland’s population fell by 0.42% over the course of the year. The decline in population is more pronounced in towns, where the year-on-year population change in 2025 stood at -0.55%, whilst in rural areas it was -0.22% cent year-on-year. Of all the provinces, only the Lesser Poland Province recorded a population increase, although this amounted to a mere 0.01% year-on-year. All provinces recorded a natural decrease (i.e. the number of deaths exceeded the number of births).

Poland’s population is falling faster than the 2023 forecast had predicted. According to the population forecast published by the Central Statistical Office (GUS) in mid-2023, the population was expected to reach 37.412 million in 2025. Thus, after three years [2], the difference stood at 80,000 people. Although this figure does not seem large in the context of our country’s total population, an upward trend is evident in the difference between the actual figures and the forecast – from 2023 to the latest readings, it stood at 15,000, 43,000 and 80,000 respectively in each year.

The forecast made three years ago underestimated the decline in the young population. In 2025, the actual number of people aged 0 to 14 stood at 5.5 million, which was 140,000 fewer than had been forecast as recently as 2023. At the same time, if we look at the population aged over 65, it turns out that in this case the actual figure exceeded the forecast by 30,000 people. A similar situation to that of the oldest age group occurred in the 15-64 age group – here too, the empirical figure was 30,000 higher than the forecast would suggest.

In an additional population projection, the Central Statistical Office (GUS) forecasts that by 2060, Poland’s population may stand at just 28.4 million. The 2025 report assumes that the fertility rate will remain at the 2024 level in the coming years and decades. Under this assumption, Poland’s population will number fewer than 37 million by 2030.

On the one hand, the underestimation of forecasts highlights just how difficult it is to create demographic models, but it also underscores the decline in the birth rate in our country. The main factor behind the underestimation of the forecast three years ago was the falling total fertility rate. Between 2021 and 2024, this rate fell from 1.330 to its lowest level in the modern history of measurements – 1.099. Therefore, the accuracy of the 2025 simulation will be determined by the trend in the total fertility rate.

Underestimates, albeit to a lesser extent, are also evident in the number of deaths. These two factors – namely, a faster-than-expected decline in the fertility rate and a slower, albeit steady, increase in life expectancy – will continue to drive the ageing of the population and a consequent decline in the population in the coming years.

- According to the national definition of residence, the population includes persons who have been living in Poland for at least three months. Immigrants staying in Poland on a temporary basis are not included in the population, whereas permanent residents of Poland who are temporarily abroad are included in the population figures.

- In the 2023 forecast, it was the first for which no empirical data was available.

Jędrzej Lubasiński

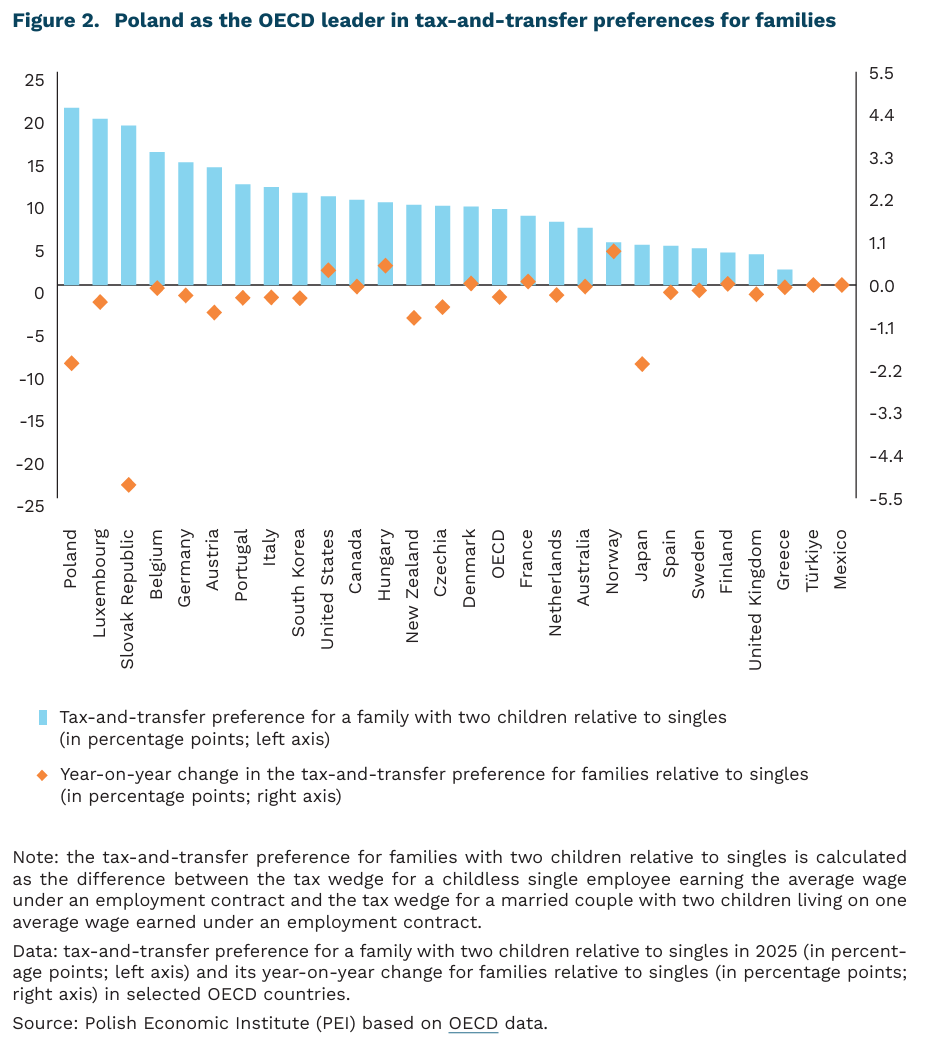

Poland ranks first in the OECD in terms of the scale of tax reliefs and financial transfers for families with children

35.1% of total labor costs in the OECD in 2025 was the tax wedge for a single person earning the average wage

8.9 percentage points lower on average was the tax wedge in the OECD for a family with two children living on one average salary compared with a single person earning the average wage

20.8 percentage points lower was the tax wedge in Poland for a family with two children living on one average salary compared with a single person earning the average wage

After the pandemic period of tax reliefs and extraordinary fiscal support, OECD countries are returning to higher effective taxation of labor income. According to the latest OECD report, the tax wedge [3] for a childless single employee earning the average wage increased in 2025 for the fourth consecutive year, reaching an average of 35.1% of total labor costs across OECD countries. This is the highest recorded level of this indicator since 2016. Among all OECD member states, effective taxation of labor income for singles increased in 24 countries in 2025 compared with 2024, with the largest rises recorded in the United Kingdom (2.45 percentage points), Estonia (1.95 percentage points), and Germany (1.34 percentage points). At the same time, the highest tax wedge for singles was recorded in Belgium, Germany, and France – at 52.5%, 49.3%, and 47.2% respectively.

However, the increase in effective taxation of labor income was not distributed evenly across different types of households. The case of families with children is particularly noteworthy, as their tax wedge increased faster than that of singles. For a married couple with two children living on one average wage, the tax wedge in the OECD increased by an average of 0.46 percentage points in 2025, reaching 26.2% of total labor costs. The net burden on lower-income single parents increased even more strongly – for a single parent with two children earning 67% of the average wage, the tax wedge rose by an average of 0.52 percentage points and reached 16.3% in 2025. This therefore indicates an erosion of the tax-and-transfer advantage enjoyed by families relative to singles, a trend that has now continued for the second consecutive year across OECD countries.

Meanwhile, Poland ranks first in the OECD in terms of the scale of tax-and-transfer preferences for families with children. In 2025, the difference between the tax wedge of a married couple with two children living on one average wage and that of a single person amounted to 20.8 percentage points in Poland, compared with the OECD average of 8.9 percentage points. Family benefits play a key role in the Polish case, as they are among the highest in the OECD and significantly reduce the effective burden on households raising children.

The increase in the effective taxation of labor income in OECD countries is to a large extent the result of tax-and-transfer systems failing to adjust to high inflation. The period of elevated inflation triggered by the COVID-19 pandemic and the Russian invasion of Ukraine drove up nominal wages, while tax systems were often not fully indexed. As a result, the mechanism of bracket creep came into effect – taxpayers moved into higher effective tax burdens despite the absence of formal tax rate increases. At the same time, the real value of some family tax reliefs and transfers declined where they were not indexed to inflation, which further increased the tax wedge for households.

3. According to the OECD methodology, the tax wedge is calculated as the share of total labor costs accounted for by personal income tax (PIT), employee and employer social security contributions, and payroll taxes, minus social benefits.

Hubert Pliszka

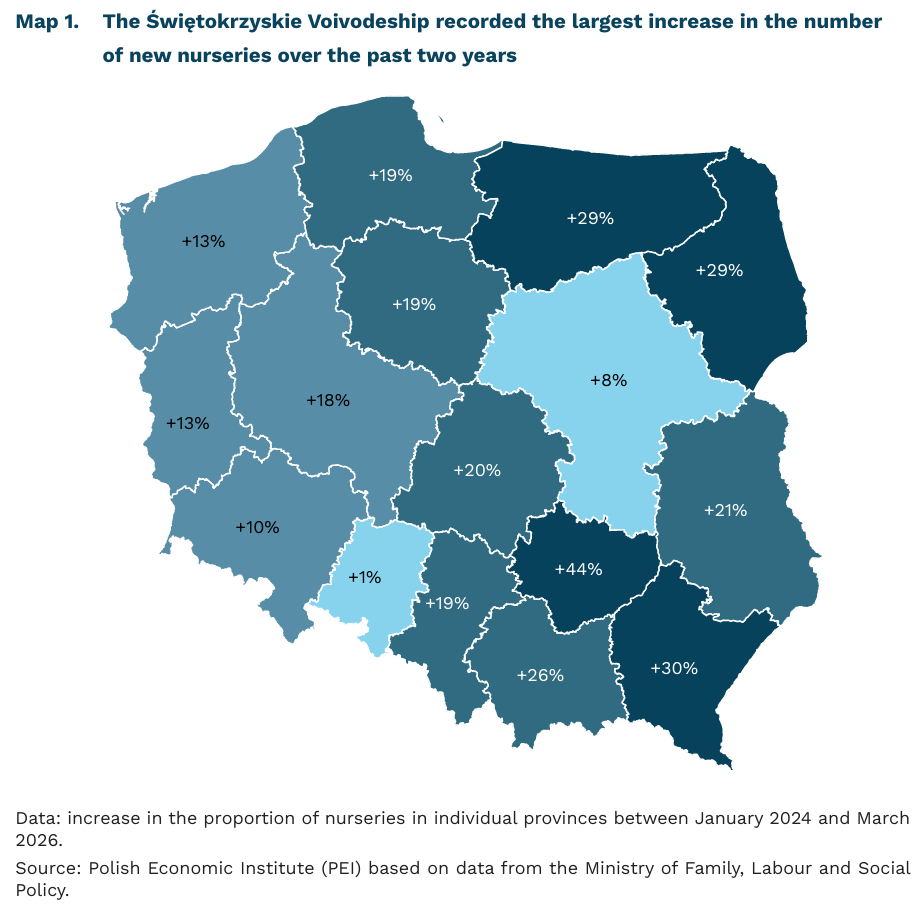

Greater availability of nurseries in Poland may increase the labor force participation of mothers of young children

17% increase in the number of nurseries and children’s clubs in Poland between 2024 and March 2026

44% increase in the number of nurseries and children’s clubs in the Świętokrzyskie Voivodeship over the last two years (from 4,189 to 6,014 facilities)

17.9% of children under the age of three in Poland attended nurseries in 2023

Over the past two years, the number of nurseries and children’s clubs providing care for children under the age of three in Poland has increased by 17%. This is primarily the result of the Active Toddler program, which uses European funds (including the National Recovery Plan) to support the creation and operation of childcare facilities for the youngest children. In some voivodeships, the increase in the number of nurseries and clubs was particularly dynamic: in the Świętokrzyskie Voivodeship the number of facilities grew by as much as 44%, while in the Podkarpackie, Podlaskie, and Warmińsko-Mazurskie voivodeships the increase was around 30%. One of the program’s goals is also to provide nursery care in municipalities where no such facilities previously existed. Whereas at the beginning of 2024 such municipalities accounted for 45%, by March 2026 the share had fallen to 29%.

Research conducted in Germany indicates that an increase in the number of childcare centres translates into higher labor force participation among mothers and improved earnings. This is illustrated by a recently published detailed analysis of a similar program implemented in West Germany between 2005 and 2014. As a result of the reform, the share of children under the age of three receiving nursery care increased from nearly zero to more than 30%. The authors of the study show that in administrative units comparable in size to Polish counties, where the number of nursery places grew rapidly, mothers were more likely to participate in the labor market, worked more days, and earned higher incomes. The estimated overall effect of the reform was a reduction in the motherhood earnings gap after childbirth by 4.5 percentage points. The gap is defined as the difference between a mother’s actual earnings and what she would have earned had she not given birth.

During the period studied, this gap decreased in Germany by a total of 8 percentage points, meaning that the expansion of nursery care alone accounted for more than half of this improvement. These results are driven, among other factors, by the fact that mothers in counties with better access to nursery care were more likely to remain employed in well-paid companies and occupations, rather than moving after childbirth into part-time work or lower-paid sectors. The increase in mothers’ earnings persists for many years after childbirth, indicating a lasting and cumulative improvement in career trajectories.

According to available data from Poland’s Central Statistical Office (GUS), in 2023 (just before the launch of the Active Toddler program), 17.9% of children under the age of three in Poland attended nurseries. Poland therefore still has considerable room for growth in the share of children attending nursery care – in West Germany the figure currently exceeds 30%, while in East Germany it is over 50%. In Poland, the low share of children in nurseries is accompanied by low labor force participation among mothers of the youngest children. As indicated in a report by the Polish Economic Institute (PEI), only 62% of mothers of children aged 1-3 in Poland are economically active, compared with 98% of fathers. However, the current scale of nursery network expansion, supported by international experience, offers hope for effectively increasing mothers’ labor market participation, which remains one of the main objectives of the Active Toddler program.

Agnieszka Wincewicz-Price

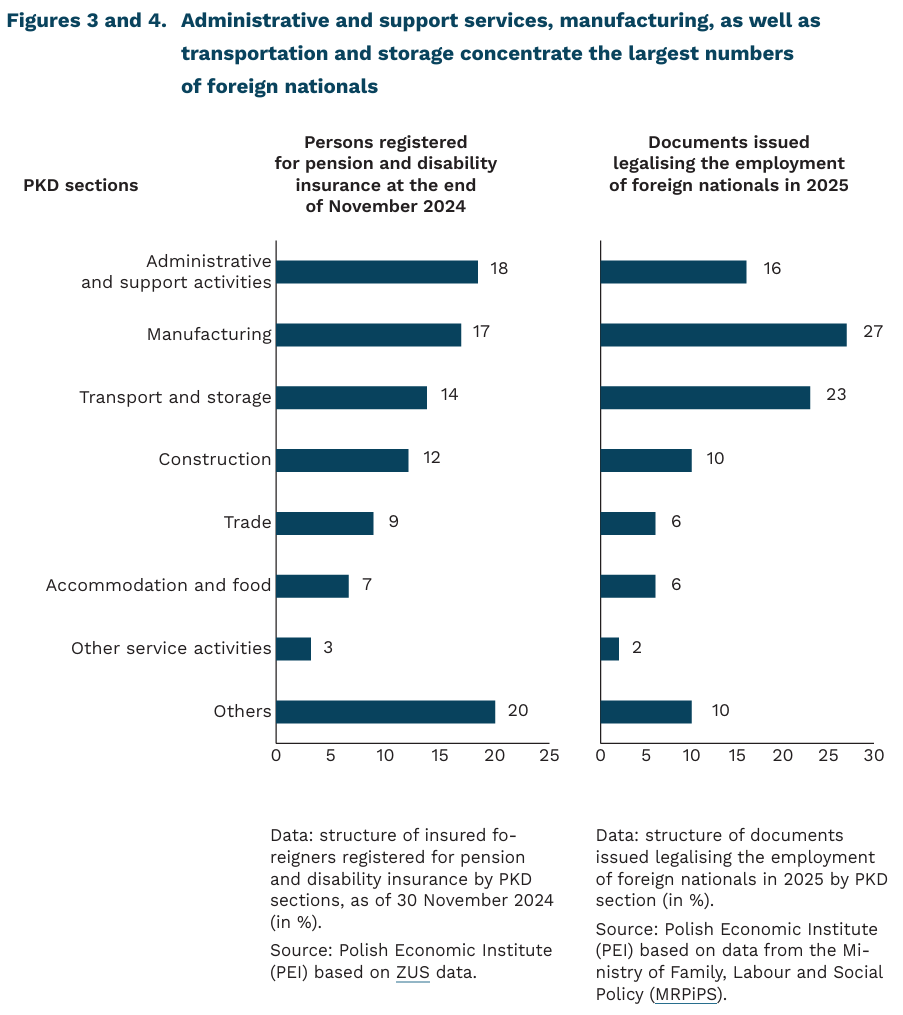

Foreigners are becoming a permanent part of the Polish labour market

1.289 million foreigners in Poland were registered for pension and disability insurance in 2025

8% was the share of foreigners among all persons covered by pension and disability insurance in 2025

66% of all documents issued to legalise the employment of foreigners related to manufacturing, transport and storage, as well as administrative and support services

At the end of 2025, the number of foreigners in Poland registered for pension and disability insurance reached 1.289 million people, according to data from the Social Insurance Institution (ZUS). Compared to 2024, this represents an 8% increase, whilst compared to 2015, the number of insured persons has risen nearly sevenfold. Most of them were employees (57%), and 7% were persons conducting non-agricultural economic activity. The largest group of foreigners in the Polish labour market were Ukrainian nationals (67%), and more than every tenth foreigner was a citizen of Belarus (11%). Georgians, Indians and Colombians each accounted for 2% of the total. Among all persons covered by pension and disability insurance, foreigners accounted for 8%, while among all employed persons their share amounted to 6%.

The highest share of foreigners registered for pension and disability insurance was recorded in the administrative and support service activities sector, where at the end of November 2024 they accounted for 18% of all insured foreigners [4]. Together with manufacturing as well as transport and storage, these sectors concentrated nearly half of all foreigners covered by social insurance in Poland (49%). A similar pattern was evident in the documents legalising the employment of foreign nationals issued in 2025 [5], of which a total of 1.634 million were issued. Of these, 27% concerned employment in manufacturing, 23% in transportation and storage, and 16% in administrative and support service activities. The largest number of documents was issued for workers performing simple jobs, industrial workers and craftsmen, as well as machine and equipment operators and assemblers.

The presented data indicate that labour migration plays an important role in the functioning of selected sectors of the economy. At the same time, the results of the Monthly Business Climate Index (MIK) show that entrepreneurs operating in the construction and TSL sectors relatively more often point to problems related to the availability of workers. This may contribute to higher demand for employees, which is reflected in the high concentration of foreigners and the large share of issued documents legalising employment. At the same time, relatively easier access to employment in some sectors may additionally increase the scale of foreign employment. In the context of projected demographic changes, including a declining working-age population, persistently low fertility rates (see the text above entitled „The population decline in Poland is greater than the Central Statistical Office (GUS) had forecast”) and the ongoing ageing of society, ZUS forecasts indicate the growing importance of foreigners for maintaining the current level of the demographic dependency ratio.

4. The most recent data on the number of persons covered by pension and disability insurance who declared a nationality other than Polish in their registration submitted to ZUS, broken down by PKD sections, are available as of the end of November 2024.

5. Documents legalising the employment of foreigners include work permits, seasonal work permits, declarations on entrusting work to a foreigner, as well as notifications on entrusting work to a citizen of Ukraine. The number of issued employment legalisation documents is not equivalent to the number of foreigners who actually took up employment in Poland. The same person may have been included in the statistics multiple times, for example in the case of a change of employer. In addition, possession of a document authorising employment does not mean that the foreigner actually started work.

Aleksandra Wejt-Knyżewska

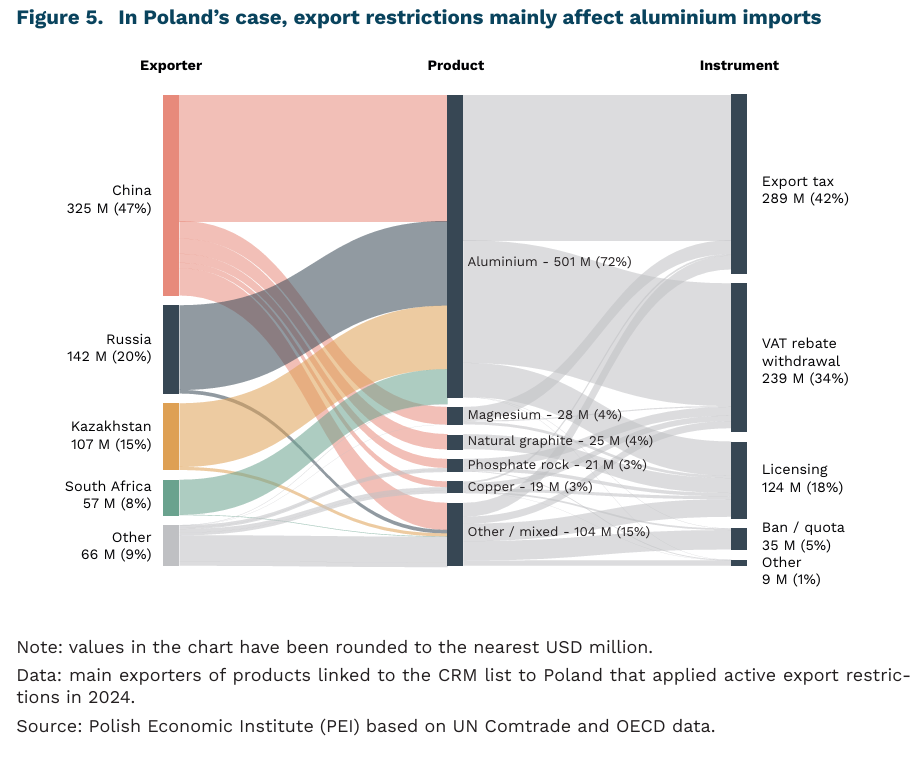

Global export restrictions on critical raw materials have only a minimal impact on Poland

16% the global share of CRM trade covered by export restrictions in 2022-2024, up from 12.4% in 2009-2011

USD 697 million the value of Poland’s imports of raw materials from countries applying active export restrictions in 2024

64% the share of Poland’s imports of natural graphite and magnesium originating from countries applying active export restrictions

Since 2009, the number of export restrictions on critical raw materials has increased fivefold, according to the latest OECD report. Although in 2024 the year-on-year growth rate slowed to 0.6%, restrictions remained at a historically high level and covered a broader group of resource-rich countries, especially in Africa and Asia. In 2022-2024, at least one restriction applied to 16% of global trade in critical raw materials (CRMs), compared with 12.4% in 2009-2011. The highest exposure concerned cobalt and manganese – around 70% of their global exports – as well as graphite, rare earth elements and tin, at 47%, 45% and 41%, respectively.

In 2024, Poland’s raw-material imports linked to the EU list of critical raw materials amounted to USD 14.6 billion, of which USD 697 million, or 4.8%, was covered by export restrictions on specific products. “Heavy” exposure to restrictions – including export bans, quotas and licensing requirements – stood at 1.05%, or USD 154 million. Three countries together accounted for around 82% of the total value: China – 46.6%, or USD 325 million; Russia – 20.4%, or USD 142 million; and Kazakhstan – 15.4%, or USD 107 million, mainly unwrought aluminium. In value terms, codes related to aluminium dominated, accounting for around 72% of imports from countries applying restrictions, or USD 501 million. These imports came mainly from China, Kazakhstan, South Africa and Russia, although they represented only 9% of Poland’s total imports in this category. Russian primary aluminium was banned by the EU in March 2025, subject to a transition period and a quota. In 2024, imports from Russia also included small quantities of unwrought nickel, worth USD 5.3 million.

Aluminium accounts for as much as 72% of Poland’s raw-material import exposure to export restrictions; once it is excluded, exposure falls to 2.1%. Almost half of the affected imports come from China, which applies the broadest range of instruments: export quotas, export taxes, withdrawal of VAT rebates and licensing requirements. In 2024, China accounted for USD 24.6 million of Poland’s USD 38.5 million imports of natural graphite in powder or flakes, and USD 28.4 million of USD 55.9 million imports of magnesium and magnesium products. China’s dominance in these categories is unsurprising: it controls more than 90% of global magnesium production and 70% of graphite production. Other categories with exposure above 50% include phosphorites and phosphates from Morocco, China, Vietnam, Algeria and Tunisia, as well as tungsten and germanium from China.

Low exposure to export restrictions does not mean low supply risk for Poland. First, exposure measured in this way may be understated, as a substantial share of Poland’s raw-material imports passes through other European countries, which may obscure the actual origin of raw materials and semi-finished products. Second, export restrictions affect only a small share of imports and a relatively narrow set of products – mainly aluminium, natural graphite, magnesium, phosphorus and phosphorites, and copper. A separate challenge concerns raw materials that are not subject to export restrictions but are dominated by a single supplier. In 2024, this applied, among others, to unwrought alloyed nickel from the United States, which accounted for 99% of imports; ferroniobium ores from Brazil, also 99%; and sodium borates from Türkiye, 97%. Diversification measures should therefore be a priority, including increased raw-material recovery; see the text below, “Aluminium recycling as a response to its growing consumption”. This is especially important in categories of particular significance for the Polish economy where a single supplier holds a dominant share.

Dominik Kopiński

Aluminium recycling as a response to its growing consumption

between 18% and 57% increase in global copper consumption for power grids by 2030, according to the IEA

8th Poland’s ranking worldwide in copper exports in 2025

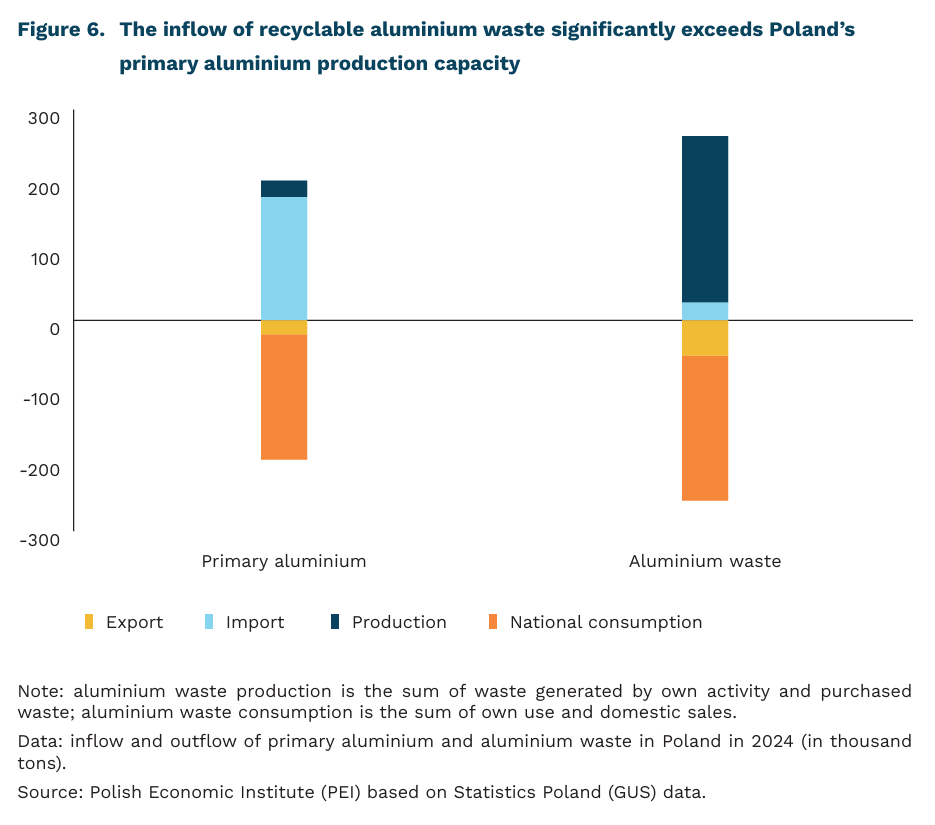

98.4% share of imports in aluminium consumption in Poland in 2024

The advancing energy transition and the development of clean technologies are increasing demand for copper and aluminium – metals that are particularly important for the construction and modernization of electricity grids. The International Energy Agency (IEA) estimates that global copper consumption for electricity grids will rise by between 18% and 57% between 2024 and 2030, depending on the scenario adopted. The IEA also forecasts a significant increase in demand for aluminium, especially in the context of rising copper costs. Although copper has long been the preferred material in power grid construction due to its higher conductivity, it is more than three times heavier than aluminium and more expensive. Replacing copper with cheaper aluminium could therefore help reduce costs.

While demand for both materials is growing, the Polish copper and aluminium sectors are in markedly different situations. In 2025, Poland was the world’s 8th largest exporter of copper and the largest within the European Union, with copper exports valued at USD 2.8 billion. In 2024, exports accounted for 50.2% of Poland’s refined copper production, indicating that the domestic sector more than covers national demand. In the case of aluminium, Poland is a net importer, and domestic metal production covers only 13% of national consumption. This highlights Poland’s strong dependence on aluminium imports. At the EU level as well, the share of imports in meeting demand is significantly higher for aluminium (54%) than for copper (17%). In 2025, Poland was the world’s 10th largest importer of aluminium. Although many EU countries (the Netherlands, Sweden, Denmark, and Germany) are among Poland’s suppliers, it should be noted that 10% of Poland’s aluminium imports in 2025 came from Russia. In addition, countries applying trade restrictions also account for a significant share (see the above text entitled “Global export restrictions on critical raw materials have only a minimal impact on Poland”).

In the context of rising demand for raw materials and other resources, recycling is increasingly being identified as both a response to circular economy objectives and a tool for strengthening sovereignty amid China’s growing dominance in the extraction and processing of strategic raw materials. In Poland in 2024, the inflow of recyclable aluminium waste was 10 times greater than domestic primary aluminium production. This indicates substantial potential for the management of such waste, particularly in strategic areas such as the expansion and modernization of energy infrastructure. At the same time, the development of processing capacities for recycled raw materials and materials could reduce risks related to trade dependencies and supply concentration.

Marianna Sobkiewicz

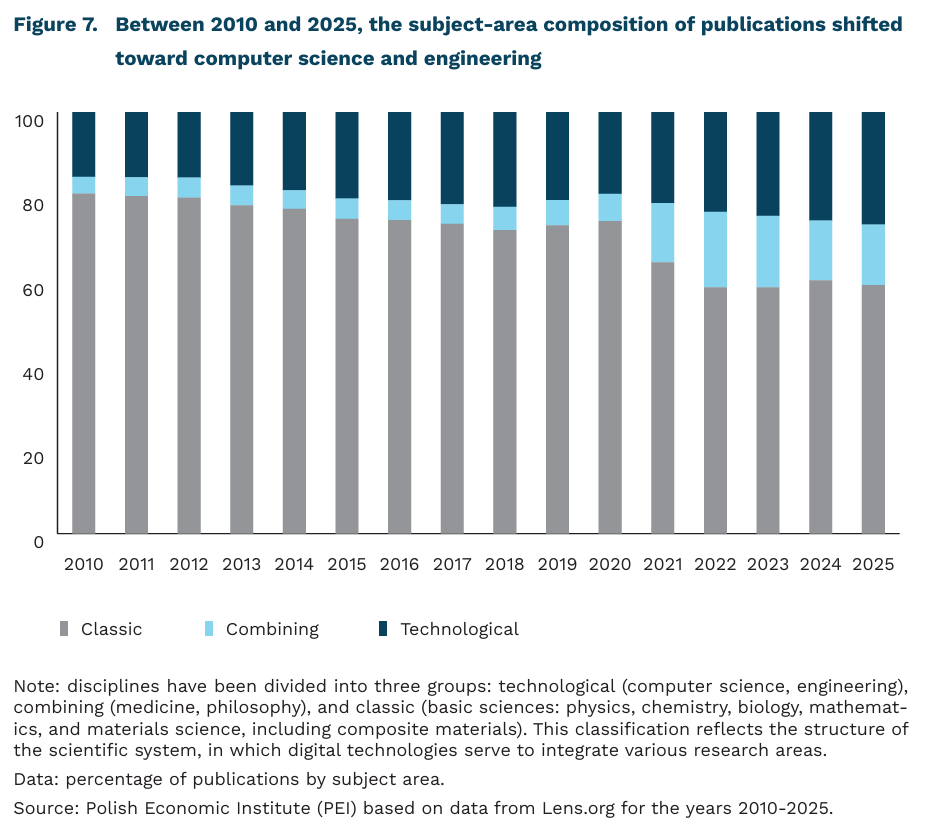

The growing role of computer science is changing the structure of research

the share of computer science and engineering in the subject-area breakdown of scientific publications (within the technology ecosystem) increased by 12 percentage points between 2010 and 2025

the share of basic sciences in the subject-area breakdown of scientific publications (within the technology ecosystem) decreased by 14 percentage points between 2010 and 2025

The importance of publications in computer science and data-driven fields has been growing in the Polish technology ecosystem (as reflected in publications from Polish research institutions) since 2018 [6]. The share of computer science increased from 9% in 2010 to 20% in 2018, and in subsequent years remained at 15-19%, constituting one of the largest subject areas. Engineering also gained in importance. At the same time, a restructuring of the entire subject structure of publications is evident. In the initial period (2010-2017), chemistry, materials science, and biology dominated. After 2018, the share of medicine began to rise, which may indicate the increasingly widespread application of digital technologies and data analysis methods in health-related fields, as well as the impact of the pandemic after 2020. At the same time, the share of philosophy increased, which is likely related to the inclusion of ethical and social issues in discussions about digital technologies as their applications expand.

Digital technologies are no longer functioning as separate specializations and are increasingly permeating various fields of science, linking them through shared tools, data, and analytical methods. A more detailed analysis of the topics indicates that some technologies integrate various fields of science. This applies, among others, to artificial intelligence, machine learning, and robotics, which are characterized by a relatively high diversity of interdisciplinary connections.

The model of scientific communication varies across disciplines. In computer science and engineering, preprints and conference proceedings play a greater role, which is associated with a faster dissemination of results, whereas peer-reviewed research articles generally dominate the publication landscape (approx. 90%). In recent years, the role of conference proceedings has diminished, with their share falling from approximately 6-10% in 2010-2018 to 2-4% after 2021, while the importance of preprints has increased from approximately 3% in 2018 to about 10% in 2023-2025. These changes may result both from the development of the open science model and increased publishing activity, as well as from changes in the indexing of sources and repositories.

Science is no longer a collection of separate disciplines; it functions as an integrated system in which technology serves as one of the unifying factors. The structural shifts we are observing suggest a transition from a traditional model based on relatively distinct fields to a convergent framework that utilizes shared tools, data, and analytical methods.

6. The analyzed data concerns a selected, filtered set of publications from Lens.org focused on technological areas (as of May 8, 2026, totaling 410 239 records). This means that they do not reflect the full structure of science globally, but rather a specialized “slice” related to the identification of technological niches in Poland.

Magdalena Lesiak