Economic Weekly 21/2026, May 29, 2026

Published: 29/05/2026

Table of contents

Profitability of Polish enterprises improved in Q1 2026

3.8% was the net turnover profitability ratio among medium-sized and large enterprises in Q1 2026

6% year-on-year was the increase in total revenues of non-financial enterprises employing at least 50 persons

9% year-on-year was the growth in enterprise investment outlays in Q1 2026

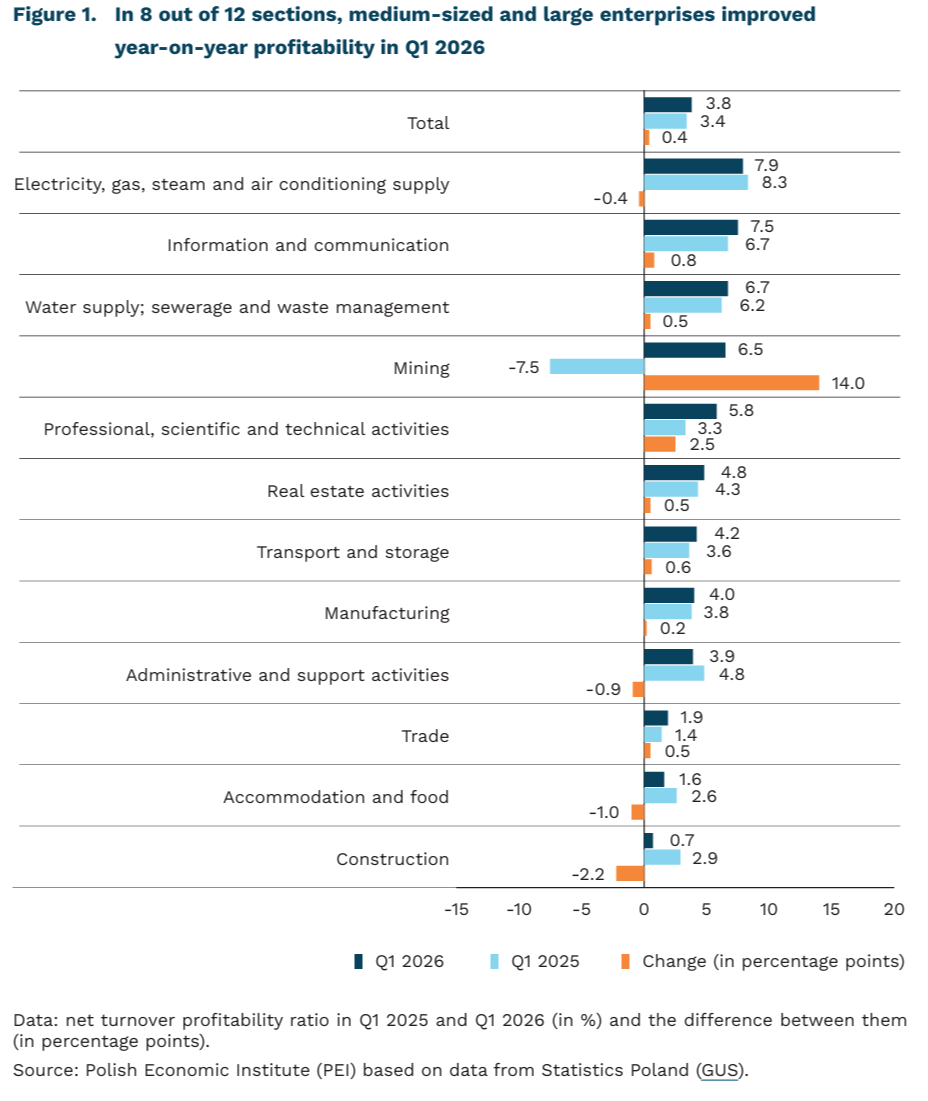

The first quarter of 2026 brought an improvement in the financial situation of medium-sized and large non-financial enterprises, according to data from Statistics Poland (The first quarter of 2026 brought an improvement in the financial situation of medium-sized and large non-financial enterprises, according to data from Statistics Poland (GUS). The net turnover profitability ratio reached 3.8%, up by 0.4 percentage points compared with the same period of 2025. The improvement in profitability resulted mainly from revenues growing faster than operating costs. Compared with Q1 2025, total revenues increased (by nearly 6%), while the cost level indicator slightly decreased year-on-year (by 0.6 percentage points, to 95.1%). Changes in the cost structure may also have contributed to the improvement in enterprises’ performance. The share of materials and energy consumption was 2 percentage points lower year-on-year and accounted for 40% of total enterprise costs. The share of labour costs increased slightly. These costs, including wages, salaries, social insurances and other benefits, accounted for nearly 22% of total costs incurred. Despite the increase in labour costs, companies were able to maintain improved profitability due to stronger revenue growth and a reduction in part of their other operating costs.). The net turnover profitability ratio reached 3.8%, up by 0.4 percentage points compared with the same period of 2025. The improvement in profitability resulted mainly from revenues growing faster than operating costs. Compared with Q1 2025, total revenues increased (by nearly 6%), while the cost level indicator slightly decreased year-on-year (by 0.6 percentage points, to 95.1%). Changes in the cost structure may also have contributed to the improvement in enterprises’ performance. The share of materials and energy consumption was 2 percentage points lower year-on-year and accounted for 40% of total enterprise costs. The share of labour costs increased slightly. These costs, including wages, salaries, social insurances and other benefits, accounted for nearly 22% of total costs incurred. Despite the increase in labour costs, companies were able to maintain improved profitability due to stronger revenue growth and a reduction in part of their other operating costs.

In the period from January to March 2026, the highest net turnover profitability was recorded by enterprises involved in electricity, gas, steam and air conditioning supply and by enterprises operating in information and communication activities (8% each). The highest increase in profitability compared with Q1 2025 was recorded by mining enterprises (an increase of 14 percentage points), which had reported negative profitability a year earlier (-8%). Such a change may have resulted from the low base effect, as well as from rising prices in the sector. The largest deterioration in profitability was recorded in construction (a year-on-year decrease of 2.2 percentage points). Despite sustained demand, the sector continues to face high labour costs and relatively low margins.

The first quarter of 2026 also brought an increase in enterprises’ investment activity – investment outlays amounted to PLN 42.4 bn and were nearly 9% higher (at constant prices) than in Q1 2025. The largest increase in investment outlays (at current prices) was recorded by enterprises involved in transportation and storage (an increase of 49%), which was partly the result of the low base in 2025, when enterprises’ investment activity was weaker. The sharpest decline in investment expenditure was recorded in enterprises operating in real estate activities (by 27%), while in Q1 2025 they had recorded a high year-on-year increase (by 94%). This may be related to the high base effect and greater caution among enterprises towards capital-intensive projects or those requiring a long payback period.

The improvement in the financial situation of enterprises in Q1 2026 was related both to revenue growth and to the gradual recovery of companies’ investment activity. The Monthly Business Climate Index (MIK) data for the first quarter show that enterprises remained cautious. Among large enterprises, positive sentiment prevailed over negative sentiment throughout the quarter, while among medium-sized enterprises the beginning of the year brought a predominance of positive assessments, which weakened in February and March in favour of negative sentiment. At the same time, the MIK component concerning financial liquidity remained above the neutral level (100 points) throughout the quarter, while investment assessments remained relatively low (63.2-98.3 points), although still clearly higher than in May 2025, when the investment index amounted to 40.4 points for large enterprises and 51.7 points for medium-sized enterprises. This may indicate that enterprises were gradually rebuilding their willingness to invest, but remained cautious towards more capital-intensive projects.

Aleksandra Wejt-Knyżewska

Only one in eight pensioners is in work

13.7% of pensioners were in work among all pension recipients in 2025

76% of working women of retirement age receive a pension

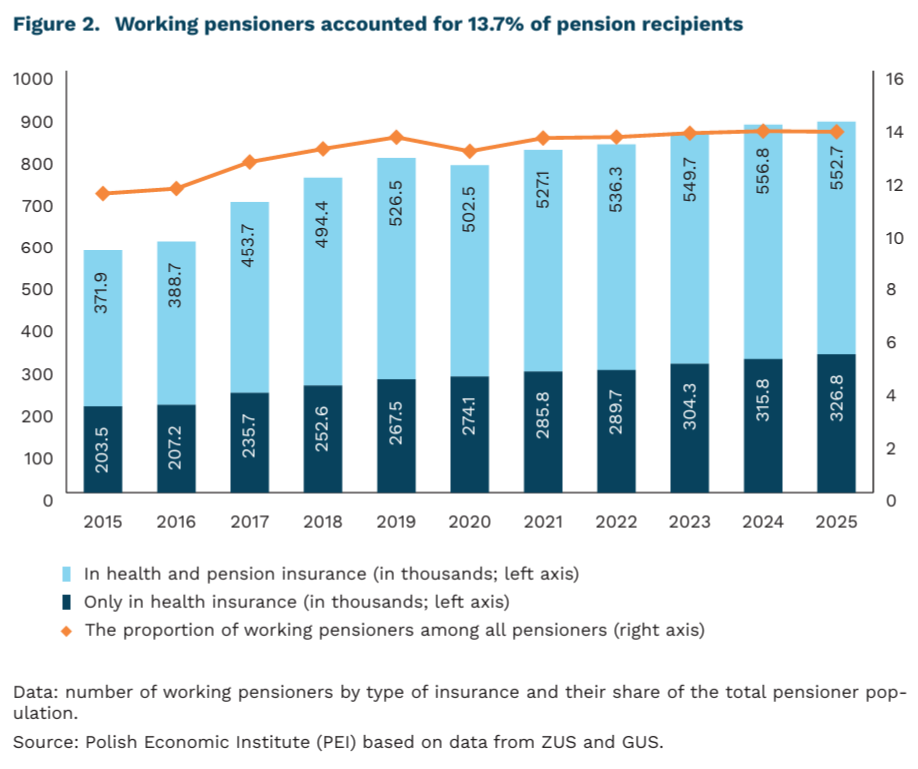

The proportion of working pensioners in Poland has remained stable for the past three years, standing at 13.7% of the population receiving pensions. At the end of 2025, 879,500 people were simultaneously receiving a pension and in paid employment. Over recent years, this figure has been steadily rising, and has increased by 53% over the last ten years, reflecting the fact that in 2015, 575,000 pensioners were in paid employment. However, this increase does not translate into a higher employment rate among pensioners, as we are simultaneously observing a rise in the population of people receiving pensions. At the same time, in Poland, the majority of all working people of retirement age have opted to receive a pension at the same time: by the end of 2025, 76% of working women of retirement age and 91% of working men of retirement age were claiming their pension entitlements. The remaining individuals continued to work without claiming a pension.

Among working pensioners – both women and men – the largest group consists of people who are just over the statutory retirement age. Among working women receiving a pension, 45% were aged 60-64, whilst among working male pensioners, 51% were aged 65-69. The highest proportion of working pensioners was employed in the health and social care sector – 17.2% of all working pensioners. The next highest sectors in terms of pensioner employment were retail (12.5%), manufacturing (10.5%), education (10.1%), and administrative and support services (7.5%).

Extending the working life of people reaching retirement age generally increases the value of their future pensions. However, this effect depends on two factors. Firstly, it depends on whether pension contributions are deducted from their earnings. In Poland in 2025, almost two-thirds of working pensioners were covered by pension insurance, whilst just over a third paid only compulsory health insurance contributions. People who do not pay contributions on their earnings do not add new contributions to their accumulated pension capital.

The second factor affecting the value of a future pension is the decision regarding when to start claiming it. A person of retirement age who continues to work whilst claiming a pension will receive a lower pension than someone who has chosen to work without claiming the pension at the same time. The decision to start drawing a pension means that only the pension itself and newly paid contributions will be subject to annual indexation, rather than contributions accumulated prior to retirement. Meanwhile, the indexation rate applied to pension capital is usually higher than the rate used to index the pension amount itself. Furthermore, in addition to increasing the value of the accumulated pension capital itself, postponing the start of pension payments reduces the expected number of years for which the pension will be received, which also results in a higher pension amount. So, whilst the fact that the majority of working pensioners in Poland are covered by pension insurance is beneficial from the point of view of their future financial situation, the fact that only a small proportion of people of retirement age choose to defer the start of their pension is less so.

Paula Kukołowicz

In 2026, global sales of electric cars will reach a 28% market share

21 million electric cars were sold worldwide in 2025, accounting for 25% of total car sales

29% of cars sold in the EU-27 in Q1 2026 were electric cars

13.5% was the share of electric cars in car sales in Poland in Q1 2026

15% of cars sold in the EU-27 in April 2026 were Chinese brands

In 2025, global electric car sales reached 21 million units and exceeded a 25% share of global car sales. According to forecasts by the International Energy Agency (IEA), sales will rise to 23.4 million units, representing a 28% share, in 2026, and to 49-55 million units (46-53%), in 2035, depending on public policy assumptions. In 2025, the global electric car fleet of 75 million vehicles reduced oil demand by a total of 1.7 mb/d (million barrels per day). According to IEA estimates, depending on the scenario, the use of electric cars will reduce oil demand by 9 mb/d under the current policies scenario and by as much as 15 mb/d under the net zero scenario.

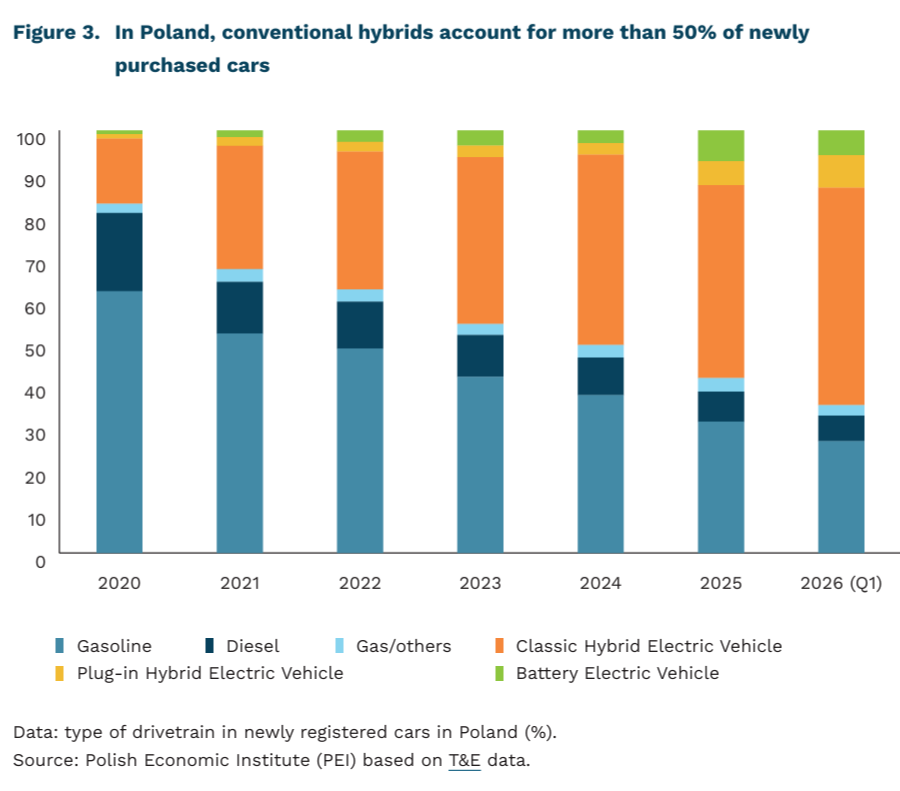

In Q1 2026, electric car sales in the EU-27 were close to the global average and stood at 29%, including 19.3% for battery electric vehicles (BEVs), and 9.5% for plug-in hybrids (PHEVs). Denmark recorded the highest share of electric car sales at 81%, including 80% for BEVs and 1% for PHEVs. This was 12.5 percentage points higher than in whole 2025.

In Poland, the share of electric car sales in Q1 2026 stood at 13.5%, including 5.8% for BEVs and 7.7% for PHEVs. Although this result is below the EU average, it is worth noting that as many as 51.5% of cars registered in Q1 were conventional hybrids (compared with an EU average of 38.6%). This is a fairly characteristic transitional stage in the shift away from purely combustion engine vehicles in some EU countries; shares above 50% can also be observed in Hungary, Romania, Cyprus, Greece and Italy.

The growing electric car market is being driven by rapid growth in China. In 2025, Chinese brands accounted for 60% [1] of global sales. Production in 2025 exceeded domestic demand, which led to a doubling of Chinese exports to 2.5 million cars. 55% of electric cars purchased outside Europe and the United States came from Chinese exports. Compared with 2024, this represented a 130% increase in sales in Southeast Asia, 60% in the Middle East and 5% in South America.

The share of Chinese electric car brands is also growing in Europe. Although European brands still dominate in terms of sales – Volkswagen with 426,000 vehicles sold, BMW with 337,000 and Mercedes with 261,000 – BYD ranked eighth, with sales of 187,000 electric cars. In April 2026, all Chinese brands combined exceeded a 15% market share for the first time.

The global increase in demand for electric cars is being driven to a large extent by energy crises, including the latest crisis related to the conflict between Iran and the United States. The falling purchase cost of electric cars, combined with a lack of confidence in the stability of fossil fuel prices – over the past four years, there have been two long periods during which the price of Brent crude exceeded USD 100, a situation not seen since 2013 – will translate into further growth in interest in electric cars. This interest will remain high even if the Strait of Hormuz is reopened. At the same time, the increasing saturation of the Chinese market with domestic production may lead to further growth in exports and a rising share of Chinese brands in foreign markets, especially in developing countries.

- Including foreign brands that have located part of their production in China, the combined share of electric cars produced there is 75%.

Adam Juszczak

The U.S. bond market remains under the influence of the Middle East conflict

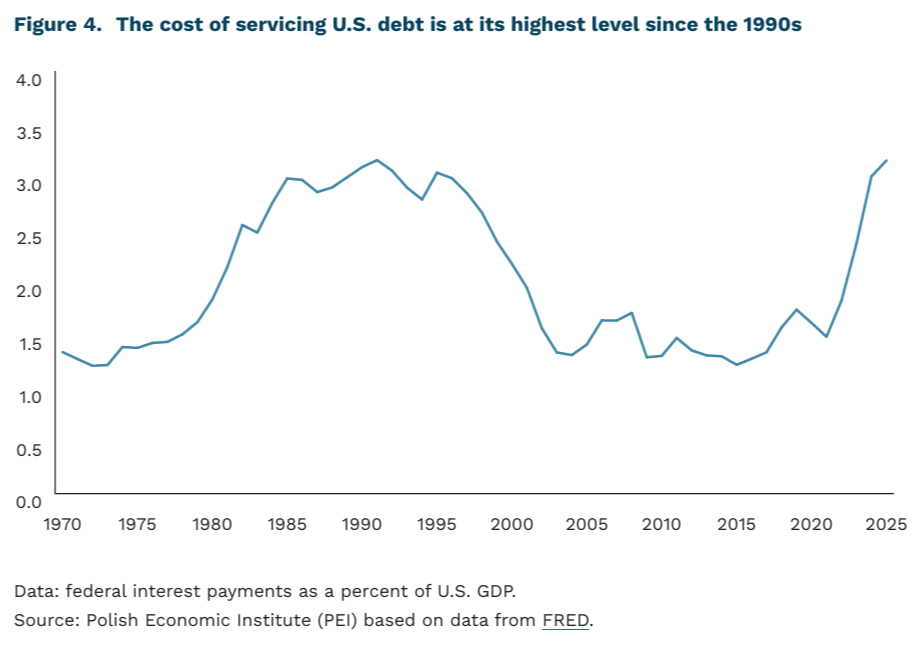

3.2% of GDP was the cost of servicing U.S. debt

4.69% was the yield on 10-year U.S. Treasury bonds

Until the escalation of the conflict in the Middle East, investors in the debt market had been following a fairly straightforward narrative: inflation was expected to gradually fade, the Fed was expected eventually to move toward further interest-rate cuts, and the Treasury bond market was expected to price in the prospect of easier monetary policy. Recent weeks, however, have shaken this scenario, above all in the United States, where the Treasury market has begun to test Washington’s resilience to higher financing costs.

The situation in the U.S. Treasury market is therefore tense, with elevated volatility. The yield on 10-year bonds exceeded 4.5% in recent days and briefly touched 4.69%, the highest level since January 2025, before stabilizing at around 4.56% toward the end of the week. Meanwhile, the yield on 30-year bonds exceeded 5.19%, a level not seen since 2007. The source of the tension is not only the ongoing conflict with Iran and its impact on inflation expectations. U.S. fiscal pressure and political uncertainty are also playing an increasingly important role in the background. The Fed minutes clearly showed a more hawkish tone, some policymakers began to allow for the possibility of rate hikes if inflation remains above target, and the market pushed back earlier expectations for cuts.

The Fed also noted an increase in the yields of 2- and 10-year Treasuries. According to the minutes, the rise in 2-year bond yields since the start of the Middle East conflict was primarily the result of higher inflation expectations, partly offset by a decline in the expected real interest rate. This is a picture of a negative supply shock, where more expensive oil and energy push up inflation while at the same time worsening the outlook for real growth. The long end of the yield curve looked different. In the case of 10-year bonds, the impact of higher expected inflation was much smaller, while the risk premium played a larger role. At the same time, the central bank noted that long-term inflation expectations remain anchored close to the 2% target, which means that the market is not yet questioning the Fed’s credibility, but is beginning to price in a more persistent supply shock.

The rise in yields is not limited to the United States. Similar moves can be seen in Europe and Japan, in some cases reaching multi-year and historical records. The yield on UK 30-year gilts reached 5.78% on May 5, the highest level since May 1998. In addition to the oil shock, pressure on gilts is being amplified by local concerns about fiscal credibility. The German 10-year Bund also tested 3.2% in mid-May, the highest reading since May 2011. Futures markets are currently pricing in two ECB rate hikes in 2026, instead of the cuts expected before the outbreak of the conflict. The strongest change can be seen in the Japanese market, where 30-year government bonds set a historical record of 4.2% and remain around 3.9%, while 10-year bonds reached levels not seen since October 1996.

The common denominator of these moves remains the combination of the oil shock and local fiscal concerns, which are forcing investors, regardless of currency area, to demand a higher risk premium for holding long-term bonds. The consequence is an increasingly high interest bill for governments. The larger the share of state revenues absorbed by interest payments, the less room remains for investment and economic policy, putting pressure on governments to carry out fiscal reforms.

Piotr Kamiński

Investment support programme through 2035 promotes modern sectors and investment quality

PLN 4.5 billion proposed budget of the new Programme for the Development of Investment in the Polish Economy until 2035

1,434 foreign greenfield projects announced in 2016-2025 in sectors broadly related to the macro-sectors of the Programme for the Development of Investment in the Polish Economy until 2035

79.4% share of investment outlays by foreign-owned firms in the previous programme

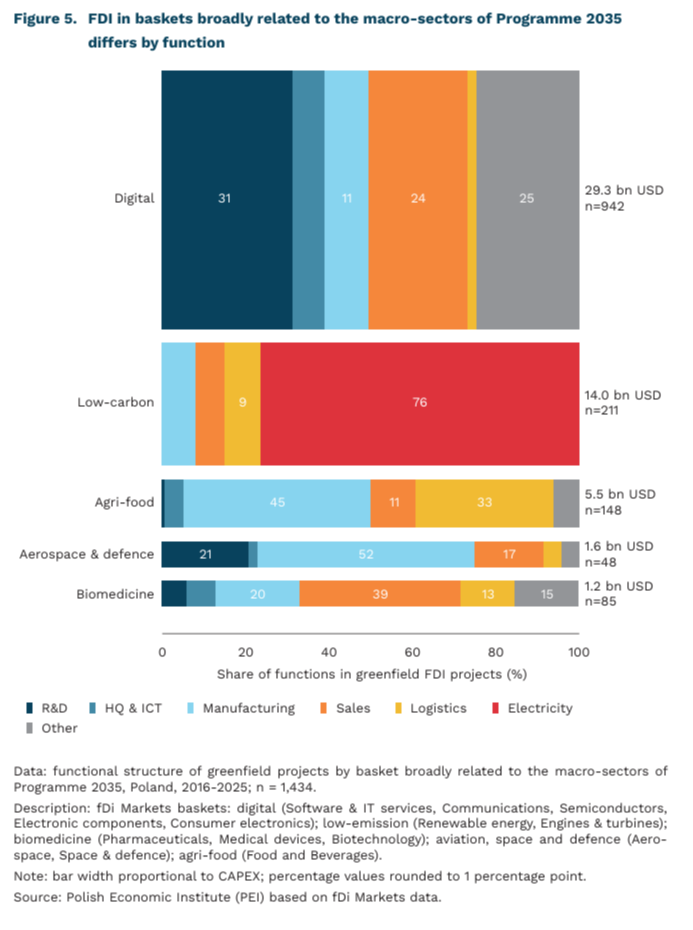

The Programme for the Development of Investment in the Polish Economy to 2035 (Programme 2035), currently at the review and consultation stage, places greater emphasis on the quality of investment in Poland. The draft programme identifies six priority macro-sectors: digital technologies, microelectronics and photonics; low-emission technologies; biotechnology and biomedicine; precision agriculture and the food sector; the aviation and space sector; and the defence industry. Compared with the previous programme, covering 2011-2030, a necessary condition for receiving support under one of the three tracks – “key sectoral and technological investment” – is that the investment be carried out in one of the above macro-sectors. A stronger quality-based mechanism is also introduced: the level of support depends on the number of indicators fulfilled, including, among others, R&D activity, cooperation with start-ups, robotisation, renewable energy sources, and local linkages. The budget initially earmarked for investment support is also significantly higher, at PLN 4.5 billion, compared with PLN 3.5 billion under the old programme, where 79.4% of outlays went to companies with foreign capital.

Over the past ten years, more than one third of all foreign greenfield investment projects reported by fDi Markets went into baskets broadly related to the macro-sectors of Programme 2035 [2]. The mapping of projects to these baskets is based on fDi Markets sectors, while their quality profile was assessed on the basis of the “Business activity” category, which describes the dominant function of a project in the value chain. In terms of estimated investment outlays, or CAPEX, the digital basket clearly dominated, with USD 29.3 billion, accounting for approx. 57% of the total investment value; within this basket, R&D projects accounted for 31.4%. At the opposite end is the biomedicine basket, where nearly 40% of projects mainly perform sales functions. The low-emission basket is a separate case, with “electricity” as the largest business activity. In the aviation, space and defence basket, R&D projects accounted for 20.8%, while the agri-food basket is dominated by manufacturing and logistics.

Programme 2035 represents a significant step forward compared with its predecessor, strengthening the qualitative assessment of projects. However, the quality criteria focus primarily on meeting specific conditions related to the investor’s activities and expenditures, rather than on classifying the project’s function in the value chain. The minimum threshold of five indicators may be reached through different combinations of criteria, covering technological elements, such as R&D, as well as environmental ones, such as renewable energy sources, or security-related ones, such as cybersecurity. fDi Markets data also show that investment projects flowing into baskets broadly related to the macro-sectors of Programme 2035 perform very different functions in the value chain. The quality criteria could therefore be supplemented with an assessment of this function, allowing projects with different modernisation potential to be better differentiated.

2. Because the fDi Markets baskets are not identical to the macro-sectors of the new programme, which narrows them down to technologically advanced segments, these estimates should be treated as approximations.

Dominik Kopiński

Lootboxes known from digital games generate addiction risks

20.3 billion USD estimated global consumer spending on lootboxes and virtual currency packs in games in 2025 (Statista)

77% of polish pupils in a pilot study by the Mentalnie Równi Foundation reported exposure to content encouraging the purchase of lootboxes

Lootboxes known from popular digital games use addictive gambling mechanisms. They are based on a simple model: a player pays for the chance to receive a random reward of varying value that can be used in the game. There is no certainty as to when the player will receive the most desired item. This is known as a variable reinforcement schedule, a mechanism familiar from slot machines: irregular and random rewards strongly reinforce the desire to continue playing and, in this case, to buy more lootboxes. Laboratory experiments confirm that rare rewards in lootboxes trigger stronger arousal than common rewards, a more intense response in the reward system, and a greater desire to open further lootboxes.

Other studies show a negative association between lootbox use and mental wellbeing, including among players in Poland. Even modest spending on lootboxes is associated with a higher risk of severe psychological distress. The results of a study conducted in Poland show that risky use3 of lootboxes is linked to more severe symptoms of gaming addiction and problem gambling. Lootboxes are not merely a gambling mechanism, but part of a broader monetisation system in digital games that shapes the risk of behavioural addictions: both to gaming and to gambling. Global consumer spending on lootboxes and virtual currency packs is estimated to have risen rapidly from around USD 15 billion in 2020 to USD 20.3 billion in 2025.

Children and young people are particularly exposed to these types of mechanisms in games. Most pupils in the pilot study by the Mentalnie Równi Foundation reported exposure to content encouraging the purchase of lootboxes (77%). The main source of these messages was influencers and well-known gamers, together accounting for 56% of responses.

Interest in the issue in Poland is not waning – among politicians, the media, and institutions, including the Children’s Rights Ombudsman and the National Revenue Administration. Under Polish law, not every game with a random element is automatically classified as gambling. The key issue is how a given mechanism works and whether it meets the criteria set out in the Polish Gambling Act. National Revenue Administration assesses whether a specific platform or mechanism should be treated as a form of gambling and then blocks domains that meet these conditions.

An effective strategy to protect users requires combining education with regulation of monetisation systems in digital games. On the one hand, strengthening financial and digital competences is crucial. On the other hand, competences alone may not be sufficient in the longer term. Research findings from Australia suggest that higher financial literacy is associated with a lower risk of problem gambling, but not necessarily with lower gambling activity or lower spending. Regulations are therefore equally important – those related to gambling, but also, more broadly, those concerning monetisation systems in digital games. In both areas, solutions drawing on behavioural science can be used, such as monthly spending summaries, default payment limits, or reminders about time spent in the game, which can genuinely reduce the costs unintentionally incurred by users, including non-financial costs.

3. Risky use of lootboxes refers to compulsive patterns of use, associated, among other things, with difficulty stopping play and postponing other activities in favour of continued purchases.

Iga Rozbicka

Pope Leo XIV supports the ‘disarmament of AI’ and the application of ethical criteria in the development of new technologies

Leo XIV’s new encyclical, *Magnifica humanitas*, revisits and updates Catholic social teaching in light of the rapid development of artificial intelligence. Developed over more than 100 years (since the time of the current Pope’s namesake, Leo XIII), Catholic social teaching focuses, amongst other things, on issues of work, social justice, the dignity of workers and equality of access to material goods. The 1891 encyclical Rerum novarum was a powerful voice in defence of workers during the Industrial Revolution, supporting, amongst other things, the formation of trade unions and the idea of a living wage, and this theme has since been regularly addressed and developed by successive popes.

The themes concerning work relate primarily to combating unemployment and warning against the negative impact of AI on working conditions. The Pope is not opposed to technological development, but emphasises that responsibility for the ethical development and implementation of innovations (including, of course, AI) should be shared by companies, governments, the scientific community and trade unions alike. He also strongly emphasises the need to move away from a paradigm focused on increasing efficiency (and using it as the main criterion for assessing an employee’s suitability) and to develop ‘social criteria for innovation’. Appropriate policies should, above all, counteract exclusion (including from the labour market), and the cost of adaptation (including, among other things, participation in lifelong learning) should be at least partially borne by the state rather than by individuals. To ensure that “new ways of working” do not lead to a decline in workers’ skills, subject them to automated surveillance, or reduce them to performing rigid and repetitive tasks, it is necessary not only to design entire systems appropriately but also to emphasise the responsibility of employers to include “the quality and dignity of work among the indicators of success”.

The encyclical does not address topics absent from discussions on the development of AI, but it clearly frames the discussion within the perspective of moral principles and Christian anthropology – highlighting the central role of the human person and the need to assess actions through the lens of their impact on the vulnerable and marginalised. An example is the issue of assessing technology based on its entire development cycle – in a very vivid passage, the text highlights the suffering of people (often children) employed in the extraction of rare earth elements, whose wounds have become necessary so that “computational flow may continue uninterruptedly”. The critique of the ‘attention economy’ and the way platforms and services are designed – with mechanisms that are addictive and ‘exploit vulnerability’ – is also very powerful. In some areas, the document suggests specific solutions – such as recommending restrictions on children’s access to mobile phones, support for processes facilitating lifelong learning, or a progressive tax system. Less attention, however, seems to be devoted to the collection of data for training models and the discussion of copyright infringements – although the theme of “invisible labour” is present in the document.

The question remains open as to whether such a document can influence a change in the current trajectory of AI development, or whether it will merely be an expression of idealistic opposition. However, at least three factors speak in its favour. First and fore most, the mainstream discussion and narrative surrounding AI has shifted away from ethical issues towards the pursuit of economic and technological dominance. This is evident both in the actions of individual states (particularly the Donald Trump administration) and in the change of tone at global AI summits. Recently, there has been a lack of such a clear voice placing ethical issues higher in the hierarchy of motivations than development itself. The papal document also aligns with themes raised by certain movements associated with the left or the labour movement, which broadens the base for positive reception and action. Secondly, the past year has heightened the significance of the Pope’s voice in political discourse – a few statements opposing Donald Trump were enough for Leo XIV to establish a clear presence in the media as a defender of established principles and the international order. Now this capital can be channelled into raising awareness of key issues in the debate on technological development. Finally, the timing of the encyclical is good. The changes brought about by AI are already visible, but the question of the target economic model or the shape of regulation remains open. A clear voice reiterating fundamental principles, delivered by a respected leader (who, moreover, is not directly involved in the ongoing rivalry), stands a chance of contributing to a more acceptable shape for the emerging socio-economic model.

Ignacy Święcicki