Economic Weekly 23/2025, June 13, 2025

Published: 13/06/2025

Table of contents

Sanctions may hit Russia’s declining revenues even harder

20% Russia’s interest rate after the latest cut

+20% y/y increase in total federal budget expenditure in the first four months of 2025

-35% y/y drop in oil and gas export revenues in the Russian federal budget in May 2025

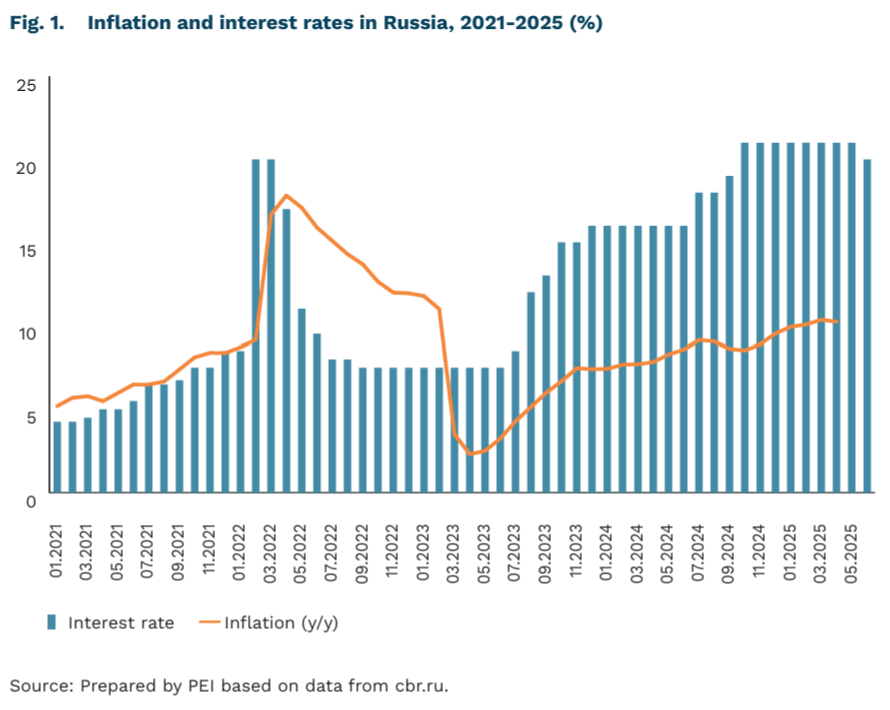

The Central Bank of Russia has cut interest rates for the first time in two years. On 6 June 2025, the benchmark rate was lowered by 1 percentage point to 20%. Despite this move, interest rates are expected to remain elevated in the near term, as inflation continues to hover around 10%. Persistently rising budget expenditure continues to hamper efforts to bring inflation under control. Between January and April 2025, total federal spending rose by 20% compared to the same period in 2024, significantly exceeding the growth rate planned for the year. A substantial share of these funds was allocated to sectors related to defence and military operations. Preliminary estimates from Rosstat show that Russia’s GDP grew by 1.4% year-on-year in Q1 2025, marking a slowdown from the official growth rate of 4.3% recorded in 2024.

The rise in budget expenditure has coincided with a decline in energy export revenues, driven primarily by falling oil prices and ongoing Western sanctions. In May, Russia’s oil and gas export revenues were 35% lower than in the same month of 2024. In previous years, part of these revenues had been accumulated in the National Wealth Fund. However, since the launch of Russia’s full-scale invasion of Ukraine, these reserves have increasingly been used to finance the budget deficit and infrastructure projects. As a result, the fund’s liquid assets have declined by roughly two-thirds. Approximately USD 40 billion remains, which may still be used to offset revenue shortfalls. Meanwhile, industrial output and the war-driven economy continue to rely on rising corporate debt, which increased by around 50%, from the start of the full-scale invasion through 2024, much of it supporting companies involved in military production.

Russian energy revenues may come under further pressure from additional Western sanctions. The European Commission’s proposed 18th sanctions package includes extending restrictions to the Nord Stream gas pipeline, transaction ban for 22 Russian banks, targeting the so-called shadow fleet that facilitates sanctions evasion, and lowering the price cap on Russian crude oil. Under the current EU and G7 policy, companies from member states are barred from providing services for oil shipments priced above USD 60. The new proposal would reduce the cap to USD 45. The package also seeks to expand restrictions on dual-use goods that may support military production. If adopted, this new round of sanctions could significantly increase pressure on the Russian economy. However, its implementation depends on unanimous support from EU member states.

Jan Strzelecki

Flexible forms of work support longer professional activity

7 years by this margin, the expected average length of working life in Denmark exceeded that in Poland in 2024

0.5 years difference in expected healthy life expectancy at age 50 between Danes and Poles in 2022

13.9 p.p. the share of part-time employment among workers aged 50-74 was higher in Denmark than in Poland in 2023

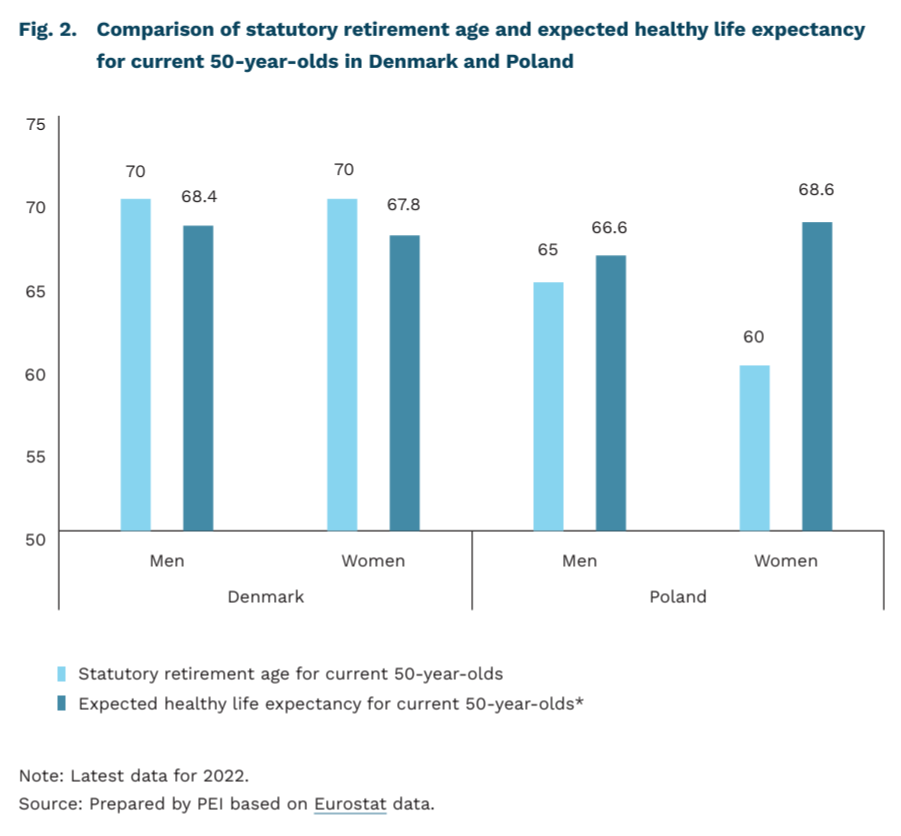

Denmark is advancing further in pension reform – by 2040, the statutory retirement age will reach 70, the highest in the European Union. This is due to an automatic adjustment mechanism, introduced in 2006, that links retirement age to increases in life expectancy. Compared to Poland, Danish men will retire 5 years later, and Danish women 10 years later. In 2024, the expected length of working life in Denmark was 42.5 years, compared to 35.5 years in Poland, meaning that Danes work, on average, 7 years longer. Meanwhile, the old-age dependency ratio (the ratio of people aged 65+ to those aged 15-64) was similar in both countries in 2024 – 32.5 in Denmark and 31.8 in Poland.

Although the statutory retirement age in Denmark is currently 67 for both women and men, Danes tend to retire earlier in practice. Between 2017 and 2022, the effective retirement age was 63.8 for women and 64.2 for men. Compared to Poland, these differences are moderate – Danish women retired 2.6 years later than their Polish counterparts, while the retirement age for men in both countries was nearly identical, differing by just 0.1 years.

Differences in healthy life expectancy between Poland and Denmark are relatively minor, suggesting similar health potential for older workers in both countries. In 2022, a 50-year-old Danish man could expect to live another 18.4 years in good health, and a Danish woman another – 17.8 years. In Poland, the comparable figures were slightly lower for men (by 1.2 years) and slightly higher for women (by 0.8 years). On average, the difference in healthy life expectancy at age 50 was just 0.5 years in favour of Denmark. It is also worth noting that Denmark operates a Senior Fleksjob programme [1], which allows people with reduced work capacity to remain in employment under flexible arrangements, potentially supporting longer working lives.

In Denmark, older workers are significantly more likely to work part-time than in Poland. In 2023, only 8.1% of Poles aged 50-74 were employed part-time, one of the lowest rates in the EU. By contrast, the share in Denmark was 22%, slightly above the EU average of 19.8%. The difference is also evident among working pensioners: in Denmark, they work an average of 21.4 hours per week, compared to 31.7 hours in Poland.

- This programme targets individuals below retirement age whose work capacity has been assessed as limited by the municipality. Trade unions can assist employees in applying for this flexible work arrangement. Employers pay only for the actual hours worked, while the municipality covers the remainder, i.e. up to the full salary the employee would receive for working full-time in the same position.

Dominika Prudło

Digitisation is Reshaping Poland’s Postal Market

1.2 billion number of courier shipments sent in Poland in 2024

101.3% increase in the value of the courier services market between 2020 and 2024

21.2% decrease in the number of letters sent in Poland between 2020 and 2024

In 2024, the postal market in Poland was valued at PLN 18.7 billion, with courier services accounting for PLN 13.7 billion, representing 73.3% of the market’s total value, according to a report by UKE. The value of the courier services segment has grown by 101.3% since 2020. This expansion has been accompanied by a steady decline in the volume and value of traditional postal services.

Courier shipments made up 56.6% of all postal shipments [2] in Poland in 2024, highlighting the dominant role of courier services in the sector. Between 2020 and 2024, the number of courier shipments rose by 91%, while their share in total postal volume increased by 22.7 p.p. This surge in demand has paralleled growth in the e-commerce and re-commerce markets. Notably, despite rising volumes, strong market competition has helped stabilise the average revenue per courier shipment in recent years at around PLN 11.

At the same time, demand for universal postal services3 provided by Poczta Polska has been steadily declining. Between 2020 and 2024, the volume of these services dropped by 22.1%, including a 21.2% decrease in letter-post items. According to UKE, the number of complaints related to universal postal services has also increased, which may suggest either a decline in service quality or rising customer expectations.

Similar trends can be observed across Europe, with Denmark standing out as a notable example. In 2026, PostNord, the Danish public postal operator, will cease letter delivery entirely. This decision reflects long-term market shifts and the accelerating digitalisation of communication. Letter volumes in Denmark have declined by 90% since 2000, and by 2024, over 94% of citizens were using digital mail services. Denmark is also a leader in digital public service use, with 98.5% of residents actively engaging with such platforms. PostNord will be the first universal service provider in the EU to discontinue letter delivery and has announced plans to expand its presence in the courier services market. entitlements. As the quality and scope of electronic public services continue to improve, demand for traditional letter services is expected to decline further. This trend will pose new challenges for Poczta Polska and the evolution of its operating model.

A significant share of letters sent in Poland consists of official correspondence between citizens, businesses, and public administration. The rollout of e-delivery systems for businesses and public institutions marks a key step toward reducing letter volume. The use of digital public services by citizens 29.1% report using them to receive official correspondence and documents, while 15.8% have submitted applications for benefits or entitlements. As the quality and scope of electronic public services continue to improve, demand for traditional letter services is expected to decline further. This trend will pose new challenges for Poczta Polska and the evolution of its operating model.

2. Total postal items include letter-post items, postal parcels, courier and express items, postal money orders, and advertising materials.

3. Universal postal services are defined by the Postal Law Act and primarily include letter-post items and parcels within specified size limits.

Improved sentiment among construction companies

+19% m/m share of construction companies reporting an increase in new orders in May 2025

+25% m/m share of companies reporting an increase in sales in May 2025

36% share of companies that incurred investment expenditure between March and May 2025

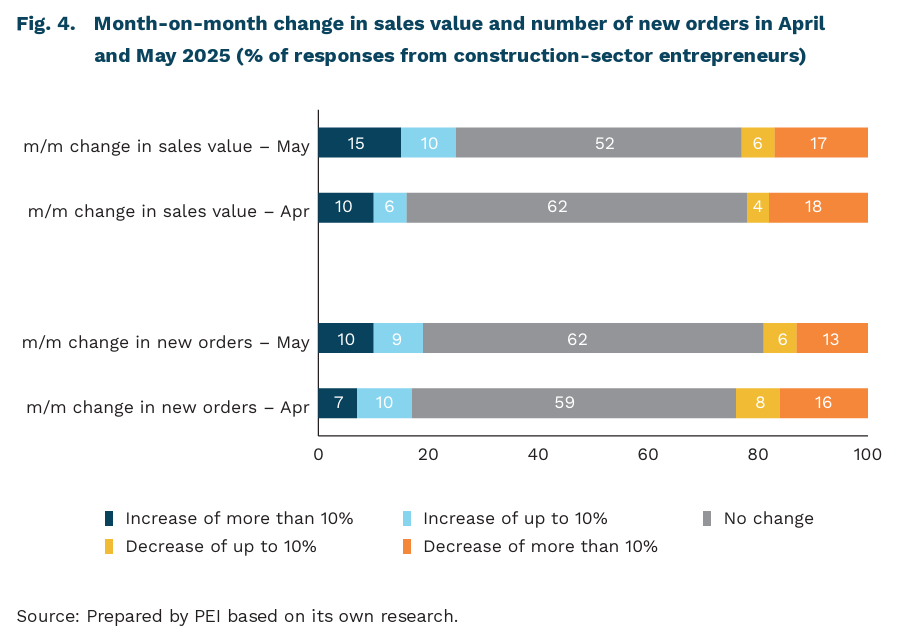

In June, sentiment among construction companies improved, according to the results of the Monthly Economic Climate Index (MIK). The business sentiment index rose by 3.2 points to 99.3. Although still slightly below the neutral level of 100, this indicates that negative sentiment only marginally outweighs positive sentiment. Similarly, the Central Statistical Office’s (GUS) May survey recorded a modest improvement in construction sector sentiment, with the index rising from -4.0 in April to -3.6 in May. Nonetheless, more firms continue to expect a deterioration in the economic situation than an improvement.

The June increase in MIK for construction was driven by a growing proportion of companies reporting month-on-month increases in sales (from 16% in April to 25% in May) and new orders (from 17% to 19%). The share of companies planning to hire in the next three months also rose, from 11% in May to 16% in June. Additionally, construction companies appear to be entering the high season with relatively strong financial liquidity: 76% reported having sufficient liquidity to operate for over two months, while only 5% said their financial reserves would not last even one month.

A modest increase in investment activity is visible among construction companies. According to the June MIK survey, the share of construction firms that incurred investment expenditure on tangible or intangible assets between March and May 2025 rose from 34% to 36%. At the same time, the proportion of companies declaring that their production capacity is insufficient to meet current orders and anticipated demand over the next month increased from 16% in May to 25% in June. This suggests a growing need for investment in the sector and bodes well for a potential increase in construction activity in the coming months.

According to a report by Spectis, demand for construction services is expected to rise in 2025, driven by EU funding (including from the National Recovery Plan), infrastructure investment (road and rail), and the energy transition. Additionally, the adoption of modern technologies, such as prefabrication and modular construction, could accelerate project timelines and improve company profitability.

However, several factors may continue to constrain the sector’s development. High interest rates, labour shortages, and geopolitical uncertainty remain key challenges. According to the June MIK survey, 64% of construction companies reported labour shortages, while 60% cited the uncertain economic environment as a major concern. Heavy reliance on large-scale investments, while a source of opportunity, also poses risks. Delays, as well as changes in project scope and design, could present significant obstacles.

Urszula Kłosiewicz-Górecka

Anticipatory investments canfacilitate electricity grid development

EUR 1.2 trillion projected investment in EU transmission and distribution networks by 2040

212 GW new renewable energy capacity installed in the EU between 2022 and 2024

The share of renewable energy in electricity generation continues to grow in the European Union, reaching 47% in 2024. Between 2022 and 2024 alone, 168 GW of solar and 44 GW of wind power capacity were added. The structure of electricity demand is also evolving due to the ongoing electrification of various sectors of the economy, including energy, industry, and transport. Given the increasing decentralisation of generation units and rising demand for electricity, power grids require modernisation and expansion.

The development of electricity grids is typically a more complex and time-consuming process than the construction of generation units, particularly photovoltaic installations or wind farms, and often spans multiple regions. Grid infrastructure projects can take 8-10 years for distribution networks and more than a decade for transmission networks. As a result, the rapid increase in new generation capacity is outpacing the development of grid infrastructure. According to the Agency for the Cooperation of Energy Regulators (ACER), as many as 63% of grid development projects experienced delays in 2024.

According to the European Commission, one recommended approach to addressing emerging grid bottlenecks is the implementation of anticipatory investments, i.e. investments made in advance of projected network needs. These can be guided by medium- and long-term projections in transmission system development plans. Examples of anticipatory investments include constructing substations with capacity exceeding current requirements or constructing poles for double-circuit lines while initially equipping with only one circuit.

By 2040, investment in electricity infrastructure across the European Union is projected to total EUR 730 billion for distribution networks and EUR 472 billion for transmission networks. Delays or underinvestment in these areas could impose significant costs on energy consumers. For example, the Scottish transmission system operator has estimated that an investment of GBP 25 million in additional network capacity could generate consumer savings of up to GBP 750 million.

Polskie Sieci Elektroenergetyczne (PSE), the Polish transmission system operator, plans to build 6,448 km of new transmission lines between 2025 and 2034, while 802 km of existing lines are scheduled for decommissioning during the same period. In addition to network expansion, substantial modernisation of existing infrastructure is essential: from 2025 to 2034, a total of 3,204 km of 220 kV and 400 kV lines are set to be upgraded. The development of electricity grids will be a critical factor in the success of Poland’s energy transition, especially in the context of planned investments in offshore wind and nuclear energy.

Marianna Sobkiewicz

Interest in housing loans is growing again

38,600 number of housing loan applications submitted in May 2025

+46.4% y/y increase in housing loan enquiries in May 2025

May saw an increase in interest in housing loans. The increased demand is visible in the number of housing loan enquiries, which rose by 46.4% y/y. A total of 38,600 people applied for housing loans This represents a year-on-year increase of 43.1% and a monthon-month increase of 8.4%. The increased interest in the form of a higher number of applications is beginning to resemble the period of the 2% Safe Loan programme in 2023. At that time, the number of applicants (from July to December 2023) amounted to 246,500 (the highest interest was in December – 46,300 people in a month). May also turned out to be a record month in terms of the average value of financing, which amounted to PLN 467,600.

The growing interest in housing loans is also reflected in the rising number and value of agreements signed. In April, 18,600 loan agreements were concluded – an increase of 3.9% month-on-month and 11.4% year-on-year. This figure is approaching the 2019 monthly average of 19,900, when the NBP reference rate was significantly lower at 1.5%. The total value of housing loans also continues to rise, reaching PLN 8.1 billion in April – up 17.4% year-on-year and well above the 2019 average of PLN 5.4 billion. This increase is driven not only by the higher number of agreements, but more importantly by record-high loan amounts. These larger loan values are made possible by improved creditworthiness and the growing popularity of fixed-rate mortgages.

Demand for mortgages is expected to continue rising in the coming months. The weakest demand in the past six years was recorded between June 2022 and June 2023, primarily due to elevated interest rates. Current levels of interest are approaching those seen in 2019 and are gradually increasing, supported by the first interest rate cut in nineteen months and expectations of further reductions later this year. These developments are anticipated to reduce loan instalments and enhance borrowers’ creditworthiness, further bolstered by rising real wages. A stable housing market is also reinforcing demand. Since the first quarter of 2024, housing prices have remained largely unchanged, particularly in the secondary market in major cities. This price stability is encouraging prospective buyers and contributing to the continued growth in mortgage applications.

Piotr Kamiński

Psychological well-being remains below pre-pandemic levels

+3.5 p.p. increase in reported symptoms of depression among people aged 50+ in the UK in 2023 compared to pre-pandemic levels

-0.1 points decline in Poland’s mental comfort index in 2024 compared to 2019 (on a 4-point scale, CBOS)

While key economic indicators such as GDP no longer reflect the effects of the COVID-19 pandemic, its impact remains visible in non-economic areas, particularly mental well-being. Although there has been a general rebound in subjective well-being post-pandemic, disparities persist among specific demographic groups. At the same time, a paradoxical improvement in mental health has been observed among some individuals who had previously struggled in this area. Successfully coping with a major challenge like the COVID-19 pandemic may have helped stabilise pre-existing mental health issues, as the return to normal life can serve as a significant positive stimulus.

Longitudinal studies – those that track the same individuals before, during, and after the pandemic – provide the most reliable insights. One such study, conducted among British citizens aged 50 and over, found that after an initial decline in life satisfaction and happiness in 2020, both indicators rebounded in the following years and even surpassed pre-pandemic levels. However, the incidence of depressive symptoms more than doubled during the pandemic and, as of 2023, remains 3.5 p.p. higher than before the pandemic. These findings account for other contributing factors such as financial situation, employment status, and social life.

A second group for whom well-being has not fully returned to pre-pandemic levels are young people. As with older adults, the pandemic led to a significant rise in depressive symptoms and a decline in life satisfaction. Longitudinal studies based on British data also observed a rebound in well-being indicators toward the end of the pandemic, particularly after restrictions were lifted. However, this improvement has not been universal – some subgroups continue to report lower well-being. In 2023, around one-third of teenagers in the UK reported persistent symptoms of diminished mental health since the pandemic.

Available data indicate that the mental well-being of Poles has not fully returned to pre-pandemic levels. According to the annual Poles’ Well-Being survey conducted by CBOS, the mental comfort index, which measures the average frequency of experiencing various negative emotions, reached a record high in 2019. In 2020, the index dropped to levels observed at the beginning of the previous decade. Although there has been a gradual improvement in recent years, the 2024 measurement shows that it remains slightly below the pre-pandemic benchmark. Specifically, the 2024 score was approximately 0.1 points lower than in 2019 on a 4-point scale. In addition to the lingering effects of the pandemic, the ongoing war in Ukraine continues to impact perceptions of psychological comfort in Poland.

Łukasz Baszczak