Economic Weekly 24/2025, June 20, 2025

Published: 20/06/2025

Table of contents

China holds strong cards in negotiations with the US

92% China’s share of global permanent magnet production

72% share of US rare earth elements (REE) imports originating from China

USD 30 billion additional US tariff revenues collected between October 2024 and May 2025

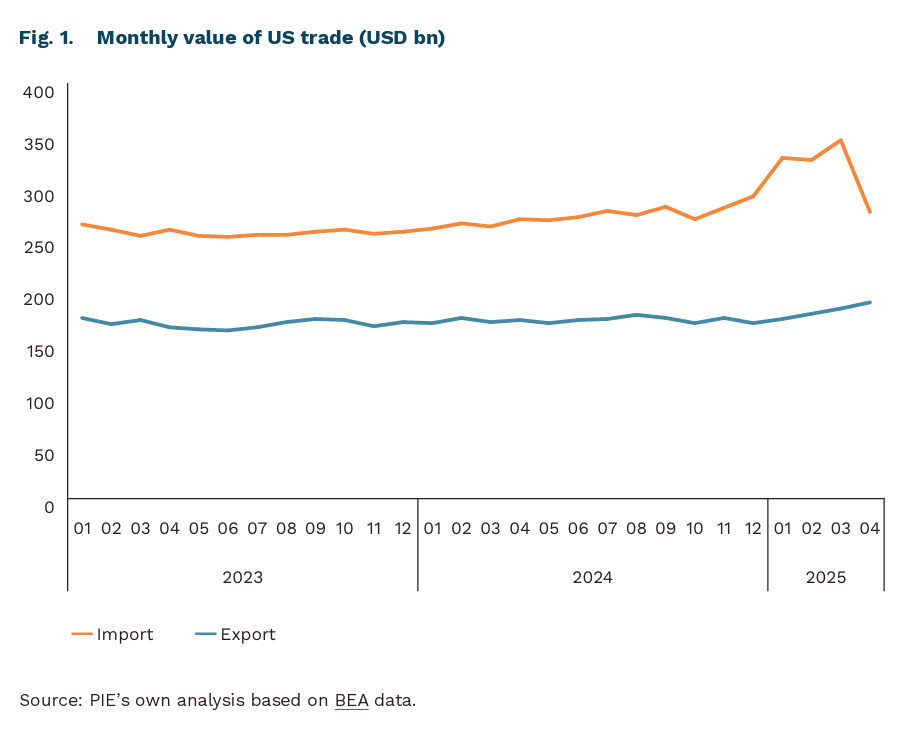

45% increase in the US trade deficit in January-April 2025 compared to the same period in 2024

The deadline for negotiating trade agreements between the US and its partners which allow the avoidance of so-called mutual tariffs announced on 2 April and suspended on April 9 for 90 days expires in early July. While it is still premature to fully evaluate the trade policies of the US administration during Donald Trump’s second term, current data offers important insights. US import data for April 2025 shows a 20% year-on-year decline in imports from China, a 12% drop from Canada, no change from the EU, and a 12% increase in imports from Poland. Although the US trade deficit fell by 14% year-on-year in April alone, it rose by 45% over the January-April period due to increased imports through March. Average tariff rates as of 14 May 2025 stood at 51% for China and 11% for the rest of the world, although tariffs on steel and aluminium were further raised to 50% in the meantime. Meanwhile, tariff revenues increased significantly by USD 30 billion (61%) between October 2024 and May 2025 compared to the same period of the previous fiscal year. OECD forecasts indicate US GDP growth slowing from 2.8% in 2024 to 1.6% in 2025. Inflation may reach nearly 4% by the end of 2025, partly due to raised tariff rates. So far, however, tariffs have had a limited effect on prices – inflation was only 2.4% year-on-year in May.

Of the widely publicised trade negotiations, two have been concluded: one with the United Kingdom, which resulted in no reciprocal tariffs, and another with China, viewed by the US administration as its main competitor. Negotiations with other partners, including the European Union, are still ongoing. However, these partners are hesitant to make concessions under pressure from unilateral US tariff barriers. Meanwhile, the White House shows little interest in a comprehensive trade deal and has rejected proposals such as the EU’s offer to eliminate bilateral tariffs on industrial goods. Overall, the announced agreements appear to yield limited gains for the US, with the White House also having to make concessions. The case of China is particularly noteworthy.

In April 2025, in response to escalating tariffs, China introduced export restrictions on rare earth elements (REE). These seventeen elements are essential components in advanced technologies, including electric vehicles, defence systems, and renewable energy technologies. Approximately 80-90% of the market value and 25% of global REE production relate to permanent magnets used in EV motors and wind turbines. Key elements such as neodymium, praseodymium, dysprosium, and terbium are critical in their manufacture. China effectively holds a near-monopoly on permanent magnet production, accounting for 92% of global output.

New restrictions introduced a requirement to obtain export licences for rare earth elements (REE), ostensibly to prevent dual-use risks. While in theory this significantly extended the export procedure, in practice it nearly froze the trade in REE. Combined with rapidly depleting stockpiles, the impact was swiftly felt by US industries, particularly automotive, defence, and robotics sectors. Some car manufacturers even considered relocating part of their component production to China, others contemplated exporting motors to China for magnet installation, while companies such as Ford and several European firms suspended production altogether.

These growing difficulties in accessing REE prompted the US to initiate talks in Geneva on 12 May, resulting in an agreed 90-day ‘truce.’ However, both sides soon began accusing each other of bad faith. The US accused China of deliberately delaying licence approvals, while China alleged that the US was imposing additional export restrictions, including on AI chips, and seeking to cancel visas for Chinese students. Nevertheless, much indicates that it was the US side, alarmed by REE shortages, that pushed for renewed negotiations and the reopening of REE exports to the US.

Although President Trump announced a successful outcome in the latest round of talks held in London from June 10 to 12, it appears that the meeting merely confirmed the Geneva agreements. The phrase ‘appears’ is used because no detailed information about the agreements has been publicly released. The Chinese side agreed to a six-month liberalisation window for the export of rare earth elements (REE), effective upon approval by both presidents, but with the right to immediately reinstate restrictions if the US does not withdraw a number of export controls. Among these are restrictions that the Biden administration, implementing the ‘small yard, high fence’ doctrine, has considered non-negotiable. Although the full list has not been disclosed, it reportedly includes jet engines and parts, as well as ethane, a by-product of hydrocarbon extraction. Both parties have set a deadline in August to develop a more comprehensive trade agreement.

Given China’s indispensability to the US industrial sector, Donald Trump may be seeking to strengthen his position as a strong leader amid escalating tensions with other trade partners. It cannot be ruled out that the administration will decide to raise tariff barriers on trade with the EU, as Trump briefly suggested in May, hinting at a 50% tariff rate. Meanwhile, Treasury Secretary Scott Bessent suggested in Congress extending the negotiation window with some countries by another 90 days. The direction of the administration’s trade policy appears to be strongly influenced by American business interests, which exert pressure leading to rationalisation of the measures taken. Nonetheless, the current situation remains unchanged, with a universal 10% tariff applied to all countries and most trade, a 25% tariff for the automotive sector, and a 50% tariff for steel and aluminium.

Dominik Kopiński, Marek Wąsiński

Entrepreneurship of Foreigners in Poland

13,700 number of sole proprietorships established by foreign nationals in Poland from January to April 2025

-8% year-on-year decrease in new sole proprietorships founded by foreigners in January-April 2025

22% share of new foreign-founded sole proprietorships related to construction

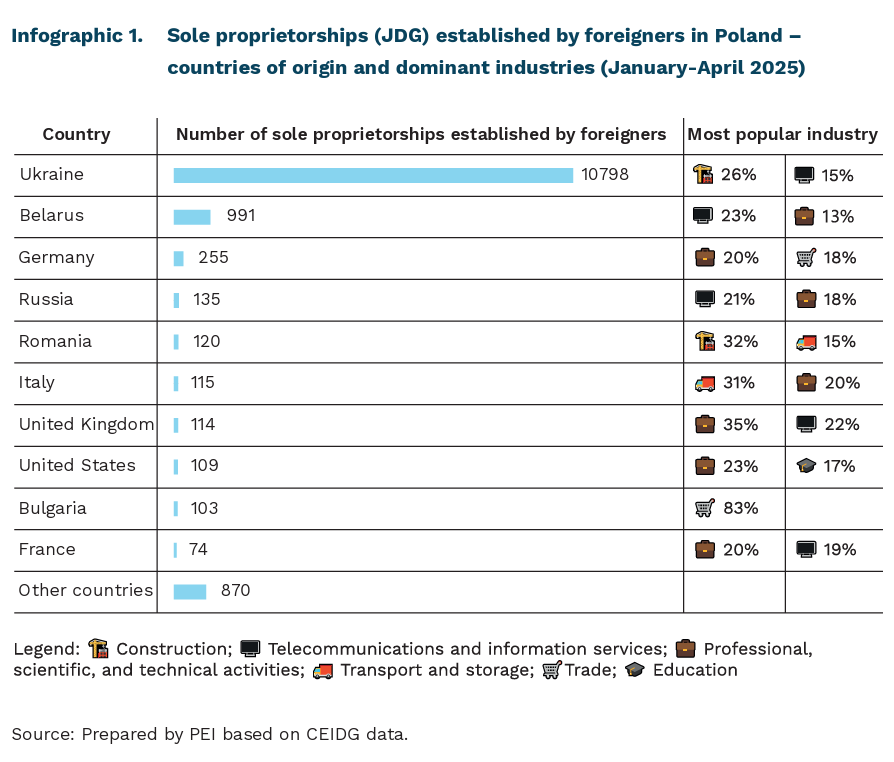

Between January and April 2025, foreigners registered 13,700 sole proprietorships (JDG) in Poland, according to data from the Central Register and Information on Economic Activity (CEIDG). Sole proprietorships established by foreigners accounted for 14% of all new entities registered in Poland during this period, with those founded by Ukrainians making up 11% of the total. Compared to the same period in 2024, the number of new firms registered by foreigners declined by 8% year-on-year, while the total number of new sole proprietorships decreased by 3%.

Nearly 80% of active businesses registered by foreigners in Poland between January and April 2025 are run by Ukrainian citizens, while 7% are run by Belarusian citizens. Businesses established by Germans accounted for 2% of all foreign sole proprietorships, a share similar to that in 2024. Among companies registered by foreigners in Poland in 2025, 22% operate in construction, 15% provide telecommunications and information services (classified under the Information and Communication section according to PKD2007), and 11% are involved in other service activities. In 2024, the dominant sectors were information and communication (23%), construction (19%), and other service activities (10%). The industry structure varies depending on the founder’s country of origin.

Construction is the leading sector among companies established by Ukrainians (26%) and Romanians (32%). Professional, scientific, and technical activities dominate among Belarusian, German, Russian, Italian, British, American, and French companies. Telecommunications and information services hold a significant share among Ukrainian, Belarusian, British, and French companies. Education is frequently chosen by US citizens, while trade is one of the top industries for German and Bulgarian entrepreneurs.

Foreign-founded businesses often respond to specific needs within Poland’s labour market and economic structure. Their role is especially prominent in sectors experiencing labour shortages, such as construction, trade, transport, and storage. For many migrants, running their own business helps overcome barriers to full-time employment, including non-recognition of qualifications, language difficulties, or legal restrictions. In this context, sole proprietorship serves as a tool for social and professional integration and a means of adapting to systemic conditions. Foreign entrepreneurs contribute to economic development by creating jobs, investing, paying taxes, and stimulating demand. Their presence enhances structural diversity and can strengthen the competitiveness of key industries.

Aleksandra Wejt-Knyżewska

Transport Emissions Account for One-Quarter of Poland’s Total Emissions

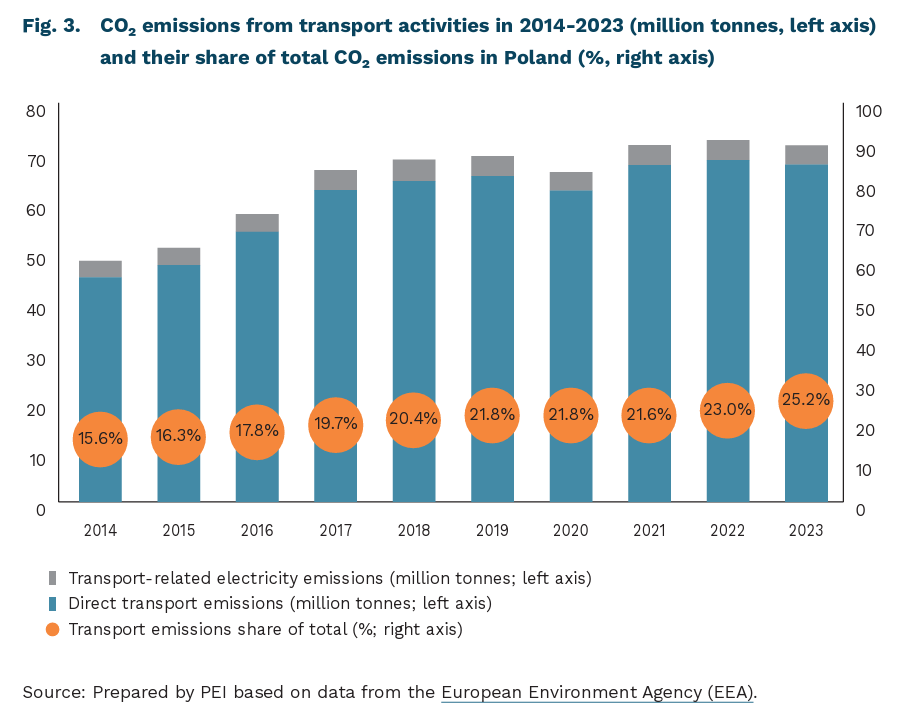

68 million tonnes direct CO₂ emissions from the transport sector in Poland in 2023

3.8 million tonnes CO₂ emissions related to electricity used in transport activities in Poland in 2023

99% share of road transport in direct transport sector CO₂ emissions in 2023

CO₂ emissions from the Polish transport sector have more than tripled over the past 35 years, rising from 20 million tonnes in 1990 to nearly 68 million tonnes in 2023. The transport sector’s share of total national CO₂ emissions has increased almost fivefold since 1990, reaching 24% in 2023. According to estimates by the National Centre for Emissions Management (KOBiZE), road transport accounted for over 99% of these emissions in 2023. The rise in emissions from road transport is linked to significant growth in Poland’s road infrastructure and vehicle fleet: motorway length expanded from 212 km in 1990 to over 5,000 km of expressways and motorways by 2023, while the number of registered motor vehicles increased from 9 million to nearly 36 million in the same period.

Actual emissions related to transport activities are higher than those directly accounted for in the transport sector’s emissions inventory. Current methodologies exclude greenhouse gas emissions from electricity generation (which are counted under the energy sector) as well as emissions from the production of materials such as cement and steel used in constructing transport infrastructure (classified under energy-intensive industries).

In 2023, electricity consumption across the entire transport sector amounted to 6.4 TWh, representing 4% of Poland’s total electricity consumption. Using an emission factor of 597 kg CO₂ per MWh for end users during this period, the transport sector indirectly accounted for 3.8 million tonnes of CO₂ emissions, which are recorded under the energy sector in national inventories. This means that in 2023, the transport sector was indirectly responsible for 25% of Poland’s total CO₂ emissions.

The exclusion of emissions related to electricity generation in transport sector analyses is particularly evident in rail transport. Railways generate minimal direct emissions from diesel traction – only 0.26 million tonnes of CO₂ in 2023, representing 0.4% of transport sector emissions. This low share is due to the high electrification level of Poland’s railway network (62.5 of total track length), which carries the majority of rail traffic. Considering that 4.3 TWh of electricity was consumed by the railways in 2023, the actual emissions related to railway operations amounted to 2.8 million tonnes of CO₂, accounting for 4% of transport-related emissions (including those attributed to the energy sector). Despite this, rail remains an energy-efficient and low-carbon mode of transport.

According to forecasts from the National Centre for Emissions Management (KOBiZE), electricity consumption for passenger transport in Poland is expected to rise to 8 TWh by 2030 and as much as 34 TWh by 2050. This increase will result from ongoing electrification efforts and the growing adoption of electric vehicles.

Krzysztof Krawiec