Economic Weekly 28/2025, July 18, 2025

Published: 18/07/2025

Table of contents

Uncertain Future for U.S. Tariffs

30% announced new U.S. tariff rate on the EU

USD 57 billion value of U.S. imports from the EU in May 2025, up USD 7 billion year-on-year

USD 15 billion / 8% year-on-year decline in U.S. vehicle imports (including parts) between January and May 2025

The outlook for U.S. tariffs from 1 August 2025 remains uncertain. Donald Trump has begun notifying countries of new tariff rates set to take effect on that date, even as trade negotiations are still ongoing. The 90-day moratorium on new tariffs officially expired between 7 and 9 July, but just before that, the administration announced that tariffs would come into force on 1 August – during which Trump would continue talks and issue formal notices. South Korea and Japan have already been informed of a new 25% tariff. The EU was initially expected to be among the negotiating partners that would not receive a tariff notice, but Trump has since announced a 30% rate for the EU, on par with Mexico, and 35% for Canada.

Of the announced agreements, only one has been formally concluded – with the United Kingdom. The agreement with China remains a unique case, while Vietnam presents an interesting example: the announced deal has not been accepted by the Vietnamese government after Trump unilaterally raised the agreed tariff from 11% to 20%. Additionally, the U.S. administration has announced a 50% tariff on copper and a 200% tariff on pharmaceuticals, both scheduled to take effect in 1.5 years. Financial markets have not yet responded to these announcements, probably reflecting investor expectations that the proposed rates will ultimately not be enforced.

Current U.S. tariff levels are already high, and further increases are anticipated. As of now, the following duties apply to imports into the United States:― 10% general tariffs, excluding select products such as consumer electronics and pharmaceuticals;

- 50% on steel and aluminum imports;

- 25% on cars and car parts (with some exemptions for parts);

- 30% on imports from China;

- 25% on imports from Mexico and Canada, excluding goods covered by USMCA.

These tariffs are expected to be supplemented by domestic tariffs scheduled to take effect on 1 August 2025. Regardless of how the domestic tariffs are finalized, import duties to the U.S. have already risen significantly. The anticipated increase in U.S. annual inflation for June – to 2.7%, up from 2.4% in May – is largely attributed to rising import costs.

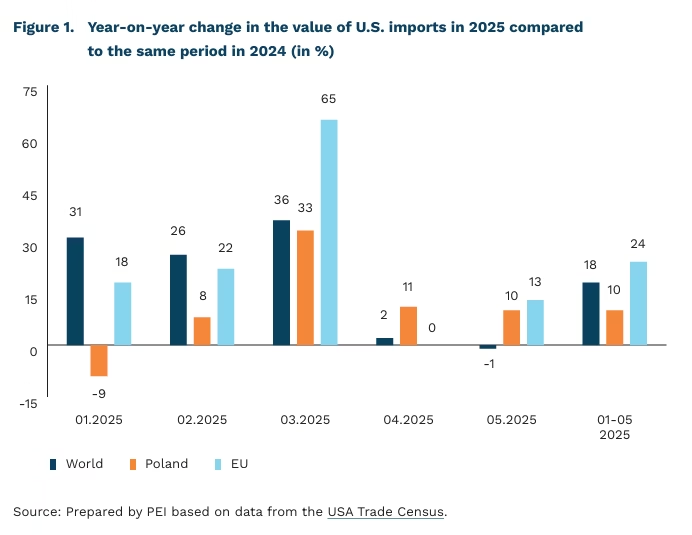

While overall U.S. imports have not yet experienced a sharp decline, a clear stockpiling effect was evident from January to March 2025, ahead of the anticipated tariff increases. During this period, total imports rose by nearly one-third year-on-year, including a 36% increase from the EU. In May, U.S. imports from the world declined by 1% compared to the previous year, but imports from the EU rose by 13%, and from Poland by 10%. In contrast, tariffs had an immediate and significant impact on the automotive sector. Between January and May 2025, U.S. imports of vehicles and parts dropped by USD 15 billion (8%) compared to the same period in 2024. Mexico accounted for nearly one-third of the decline, followed by South Korea (20%), Canada (14%), and Germany (8%). Interestingly, Germany’s largest decline occurred in the export of automotive parts.

One of the key objectives of the tariff offensive was to stimulate domestic industry, in part by attracting foreign direct investment. According to the Trump administration, high tariffs would pressure foreign firms to move production to the U.S. in order to maintain their competitiveness. Data from fDi Markets on announced greenfield manufacturing projects appear to support this rationale. In the first half of 2025, the United States attracted USD 142 billion in announced greenfield manufacturing investments representing 91% of all such announcements for the year. However, this is only a small fraction of the USD 2.6 trillion in investments cited by the administration and is difficult to reconcile with the USD 14 trillion figure mentioned by the President.

It is important to note that USD 97 billion, nearly 70% of the announced investments in the first half of 2025, relates to the third and final phase of investment plans by Taiwanese semiconductor giant TSMC. These projects are being implemented under the CHIPS and Science Act, passed during the Biden administration. Given the typical investment cycle, a significant share of these projects were either inherited from the Biden era or approved prior to the 2024 election. Additionally, a ‘Trump effect’ may be influencing corporate messaging – many foreign firms publicly link their investments to the current administration’s policies, possibly to avoid becoming targets of future trade actions.

Dominik Kopiński, Marek Wąsiński

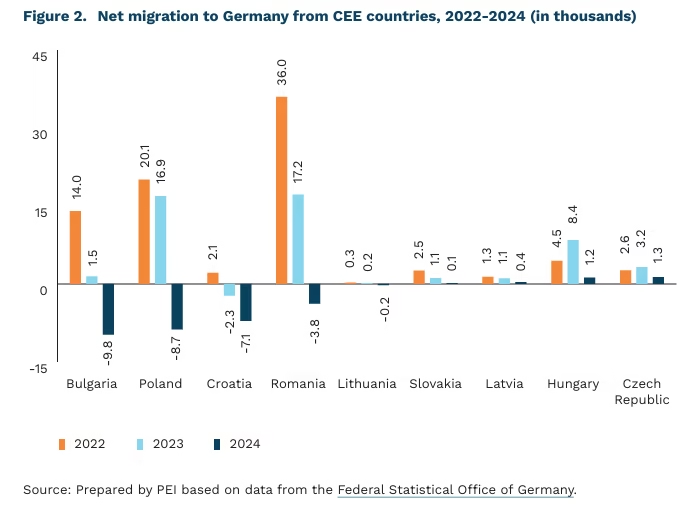

Germany Records First-Ever Negative Migration Balance with Central and Eastern Europe in 2024

-26,600 net migration balance between Germany and CEE countries in 2024

8,700 net outflow of Polish citizens from Germany in 2024

24% share of Ukrainian migrants in Germany’s net migration balance in 2024

In 2024, Germany recorded a negative net migration balance with Central and Eastern European (CEE) countries for the first time. Across nine countries (Poland, Bulgaria, Croatia, Latvia, Lithuania, Romania, Slovakia, Czechia, and Hungary) 26,600 more people left Germany than arrived(1). This marks a historic reversal. In 2023, net migration from these countries was still positive at 47,000. Between 2013 and 2023, the average annual net inflow from the CEE region stood at 139,000.

The downward trend in Germany’s net migration with CEE countries has been visible for nearly a decade but accelerated sharply after 2022. The peak was recorded in 2015, when Germany received 257,000 more migrants from the region than it lost – the highest level since the 2004 EU enlargement. Since then, only in 2017 and 2022 has the year-onyear change in the migration balance been positive. In 2023 and 2024, the annual dynamics dropped by -43% and -156%, respectively.

The negative migration balance between Germany and Central and Eastern European (CEE) countries in 2024 was primarily driven by four countries: Poland (-8.7 thousand), Bulgaria (-9.8 thousand), Croatia (-7.1 thousand), and Romania (-3.8 thousand). While Germany did not record a negative balance with every country in the group of nine, the migration surplus in 2024 was lower than in both 2022 and 2019 for all of them (with the exception of Hungary in 2019).

In 2024, Germany recorded the highest net migration figures with Ukraine, Syria, India, Turkey, Afghanistan, Iran, and Kosovo – each accounting for a net inflow of more than 15,000 people. The largest groups were Ukrainians (121,000), Syrians (75,000), and both Indians and Turks (41,000 each). Among the top 20 countries contributing to Germany’s highest net migration figures in 2024, only Italy was an EU member state. Germany’s net migration balance with Italy (excluding German citizens) was 5,200 in 2024, down from 10,400 in 2023. The year before, Poland and Romania were also among this group.

Excluding migration from Ukraine and Syria, Germany’s 2024 net migration would have been the lowest since 2020, though still considerable. Ukrainian migration accounted for 62% of the total net inflow in 2022, 16% in 2023, and 24% in 2024. A similar trend is visible for Syrians: net migration jumped from 41,000 in 2021 to 68,000 in 2022. Without Ukraine and Syria, Germany’s net migration in 2024 would have totaled 315,000 – the lowest since the pandemic year 2020, when the figure (also excluding these two countries) was 226,000.

According to Statistics Poland (GUS), Germany has traditionally been the primary destination for Polish emigrants. At the same time, the German labour market remains heavily reliant on migrant workers. Eurostat data show that in 2024, 21% of all employed persons in Germany aged 15-64 were foreign-born, compared to an EU average of 15%.

- This statistic excludes German citizens – the figure of 26.6 thousand refers solely to nationals of the analysed CEE countries.

Jędrzej Lubasiński

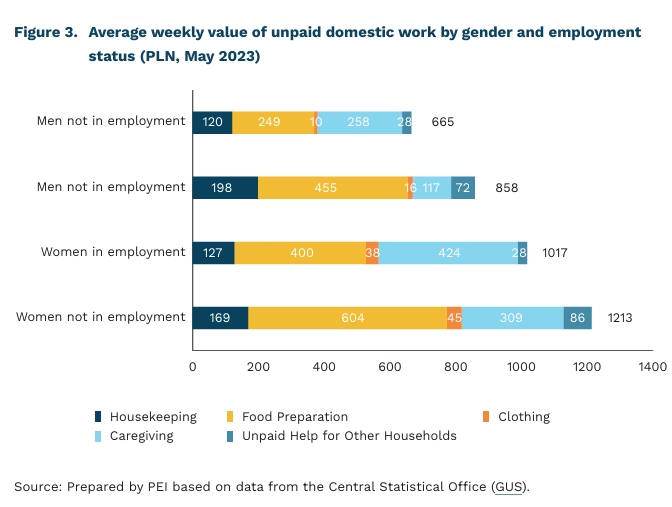

Invisible Household Production Generates Value Equivalent to 40% of GDP

40% share of Poland’s GDP in 2023 attributable to the gross value added from non-market household production

PLN 4,727 average monthly value of unpaid domestic work performed by women in 2023

PLN 3,035 average monthly value of unpaid domestic work performed by men in 2023

A substantial share of the labour necessary for the functioning of the economy and society takes place within households yet remains unrecorded in official economic statistics. This so-called invisible work includes caregiving, housework, and meal preparation. Although unpaid, it holds significant economic value. Economists are increasingly highlighting this overlooked area of activity. According to estimates published by Statistics Poland (GUS), the gross value added from non-market household production in 2023 amounted to 40% of the country’s GDP, underscoring its critical but often underestimated role in the national economy.

The value of domestic work performed by women is significantly higher than that performed by men. In 2023, the average monthly value of unpaid domestic work in Poland was estimated at PLN 3,993, equivalent to 56% of the national average gross salary. For women, the value reached PLN 4,727 (66% of the average salary), compared to PLN 3,035 for men (42%). Across all categories – home maintenance, food preparation, clothing care, and caregiving – the value of women’s unpaid (or invisible/hidden) work was consistently higher. These estimates were obtained by multiplying the time spent on each activity by the market hourly wage for equivalent paid work.

Women carry out higher-value domestic work regardless of employment status. In 2023, the weekly value of unpaid domestic labour performed by women outside the labour market was 14% higher than that of employed women (PLN 1,213 vs. PLN 1,017). Among men, the difference was even greater, with non-working men contributing 25% more than their employed counterparts (PLN 858 vs. PLN 665).

Mothers, particularly those not in paid employment and caring for young children, perform the highest-value domestic work. As the number of children increases, so does the time spent on caregiving and household duties, while time for paid work, rest, and basic needs decreases. In 2023, the weekly value of unpaid domestic labour for a married mother with one child was estimated at PLN 1,414, rising to PLN 2,404 for mothers of four or more. However, the age of the child has an even greater impact than the number of children. The highest values were recorded for non-working parents of children under three: PLN 2,806 per week for mothers and PLN 1,810 for fathers. Among working parents with children of this age, the weekly value was PLN 2,336 for mothers and PLN 1,267 for fathers.

Valuing domestic work in monetary terms highlights its scale but does not capture its full meaning. Unpaid household labour challenges the assumptions of classical economic models based on utility-maximising individuals. Its economic value is only a proxy for the time and effort involved, and it does not capture the care, altruism, or sense of responsibility that distinguish domestic duties from market labour.

Iga Rozbicka

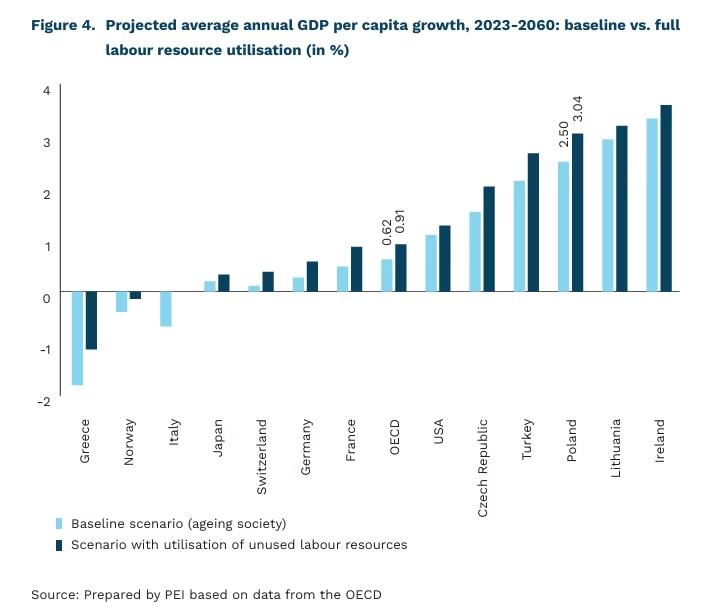

The Demographic Crisis Looms Over OECD Countries

52% projected share of the population aged 65+ relative to the working-age population (20-64) in OECD countries by 2060

2.5% forecasted average annual growth rate of Poland’s GDP per capita from 2023 to 2060, assuming an ageing population (OECD)

Demographic shifts are emerging as a critical challenge for OECD member states. The proportion of people aged 65 and over relative to those of working age (20-64) is expected to rise sharply – from 31% in 2023 to 52% by 2060. In Poland, this figure is projected to exceed 75%, making it one of the countries most severely affected by the demographic crisis. Poland is also experiencing a clear decline in population – from 38.5 million in 2010 to 37.5 million by the end of 2024.

A key consequence of demographic ageing is the slowdown in GDP per capita growth. A declining population reduces labour input in the production of goods and services. At the same time, a smaller population mechanically inflates per capita GDP figures, as output is distributed across fewer individuals. In the baseline scenario (assuming continued demographic ageing), the average annual GDP per capita growth in OECD countries is projected at just 0.6% between 2023 and 2060. With better utilisation of untapped resources(2), this rate could rise by 0.3 percentage points. Poland stands out in the OECD in this regard. Its projected per capita GDP growth is 2.5% in the baseline scenario and 3% assuming resource mobilisation – the third-highest among OECD countries, after Ireland and Lithuania. This suggests that Poland could benefit significantly from structural reforms aimed at improving labour market participation and productivity.

Declining fertility and an ageing population will also have wider implications for the economy. An older society may be less inclined to take entrepreneurial risks or start new businesses, potentially dampening innovation and slowing the adoption of new technologies. Demographic shifts are also expected to alter consumption patterns. Older households tend to allocate a greater share of their spending to healthcare, pharmaceuticals, and care services, while spending less on durable goods. According to OECD estimates, peak healthcare consumption occurs in the oldest age groups, suggesting that the healthcare sector will account for a growing share of GDP.

Addressing the negative effects of the demographic crisis will require strategic and forward-looking action. Supporting older workers in upskilling and adapting to changing labour market needs will demand a shift toward a lifelong learning model. To counter declining labour mobility, flexible employment solutions and targeted support for mid-career workers should also be prioritised. Boosting productivity growth will depend on the effective deployment of AI and automation. However, this must be accompanied by appropriate guidance, supportive policy frameworks, and robust regulation to ensure a smooth and equitable transition.

2. With better utilisation of untapped labour resources, two-thirds of the potential gains could be achieved through greater employment of older workers, gender equality, and sustained migration.

Piotr Kamiński

Summer Holidays Boost Sentiment in Vacation-Related Service Firms

73% share of Poles planning a summer holiday trip in 2025

25% vacation-related businesses reporting increased sales in June 2025

39% vacation-related businesses that made investments in Q2 2025

According to research by the Polish Tourism Organisation, 73% of Poles plan a summer holiday trip with at least one overnight stay between late June and the end of September 2025 – slightly more than last year, when 7 in 10 declared similar plans. 18% do not intend to travel for more than one day, while 9% remain undecided. Meanwhile, 18% do not intend to travel for more than a day, and 9% remain undecided. The majority (61%) will spend their main holiday in Poland, while 31% plan to travel abroad. Poles do not expect a significant increase in holiday spending – according to a study by the Polish Bank Association, planned expenditures may rise by less than 2% compared to last year.

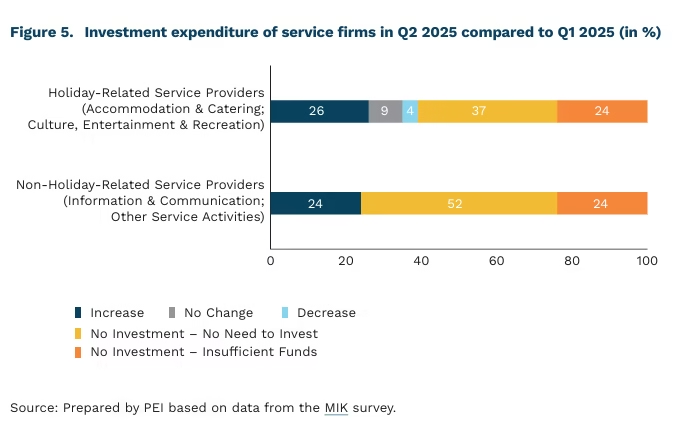

The summer tourist season is clearly reflected in the performance of the service sector. According to the July MIK (Monthly Business Climate Index) survey, positive sentiment among service providers now outweighs negative outlooks. The sector’s MIK score rose by 3.1 points month-on-month and by 11 points compared to July of the previous year. Among businesses offering holiday-related services (Accomodation and Food Service Activities; Arts, Entertainment and Recreation), 25% reported an increase in sales value in June versus May, and 22% saw a rise in new orders. In contrast, for firms providing non-holiday- related services (Information and Communication; Other Services Activities), those figures were 18% and 14%, respectively.

Most holiday-focused service firms do not plan to change staffing levels over the next three months: 11% intend to hire, while 9% expect to reduce staff. A strong majority (95%) have no plans to adjust wages during the summer, while 5% anticipate introducing pay raises.

Investment activity has also been notably higher among holiday-related service providers, i.e. 39% reported capital expenditures in the last three months, compared to 24% among other service firms. Their financial condition is also better: nearly 60% report having sufficient liquidity to operate for more than three months, compared to 53% of non-holiday-related service firms. This increase in investment could help improve the offer and attract more customers, providing optimism that the upward momentum in the MIK index for services will continue throughout the holiday season.

Anna Szymańska

European Union Imposes New Sanctions on Russian Oil

9× decline in Russia’s share of EU oil imports between early 2022 and 2024 (from 27% to 3%)

EUR 41 billion value of Russian oil purchased by India and China in H1 2025

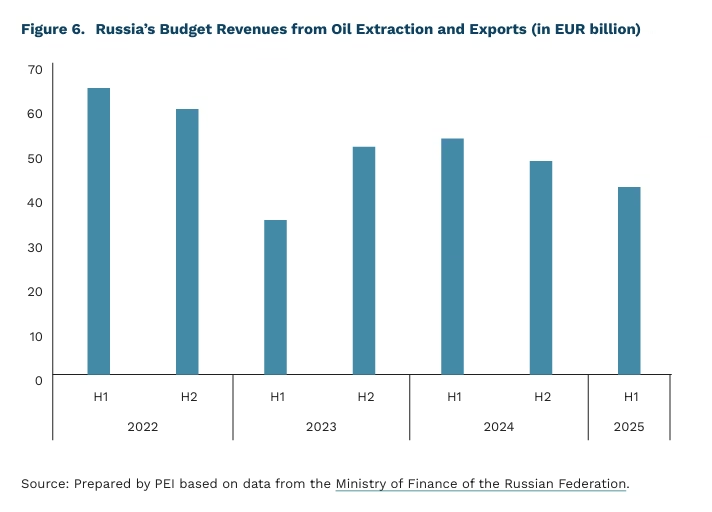

EUR 42 billion Russia’s budget revenue from oil extraction taxes in H1 2025

The European Union is moving forward with its 18th sanctions package against Russia, which includes new price caps on Russian crude oil. According to the European Commission’s proposal, the maximum price for Russian oil would be set at 15% below the average market price(3). This update builds on an earlier measure that capped the price at USD 60 per barrel. Between April and June 2025, the market price of Urals crude fell and fluctuated between USD 55 and 60 per barrel. At present, it stands at approximately USD 65. The proposed cap would further restrict Russia’s oil revenues, adding pressure to its state finances.

In the first half of 2025, Russia’s budget revenues from oil extraction taxes and export duties amounted to EUR42 billion, i.e. EUR 11 billion less than in the previous year, but EUR 7 billion more than in H1 2023 and slightly above the 2018-2025 average (by approximately EUR 70 million). Although EU sanctions have significantly reduced trade with Russia, the total value of oil imported from Russia to the EU since the start of the war has reached EUR 104 billion. However, Russia’s share of EU oil imports has declined sharply over the past three years – from 27% at the start of 2022 to just 3% in 2024.

Russia continues to generate most of its oil export revenue from China (EUR 22 billion in H1 2025) and India (EUR 19 billion), with Turkey also remaining a key importer (EUR 3 billion). There are growing suspicions, however, that some crude oil and petroleum products, especially those routed through Turkish ports such as Ceyhan, Marmara Ereğlisi, and Mersin (which lack domestic refineries), are being re-exported to EU countries. Within the EU, Hungary (EUR 1.1 billion) and Slovakia (over EUR 900 million) are currently the leading importers of Russian oil(4).

Poland is among the countries that have completely halted imports of Russian oil. On 30 June 2025, Orlen’s contract with Russia’s Rosneft expired. Prior to that, other agreements for deliveries via the Druzhba pipeline had been terminated, and maritime imports were also discontinued. Currently, the crude oil processed at Orlen’s refineries in Poland and Lithuania is sourced from multiple regions, including the Middle East, the North Sea, Africa, and both Americas.

3. Some reports also mention a proposed fixed price cap of USD 45 per barrel.

4. Prepared by PEI based on raports by the Centre for Research on Energy and Clean Air.

Adam Juszczak

European Commission Imposes New Fines for Digital Regulation Violations

EUR 2 billion total fines imposed on Meta by the EU since 2023

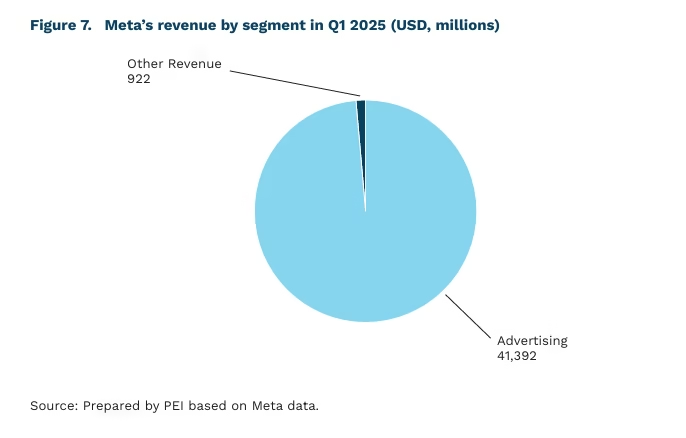

99.8% share of Meta’s revenue generated from advertising

Meta, the parent company of Facebook and Instagram, is under mounting pressure from the European Commission over breaches of digital regulations, particularly concerning its pay-or-consent advertising model. In April 2025, the Commission imposed a EUR 200 million fine on Meta for violating the Digital Markets Act by implementing a system that compelled users to choose between paying for an ad-free service or consenting to the use of their personal data for targeted advertising. The Commission concluded that this model did not offer users a meaningful choice.

The European Commission’s actions have prompted further developments. Although Meta attempted to adjust its advertising model, the Commission deemed the changes inadequate. In response to regulatory pressure, Meta introduced an option for less personalized advertising for users in Europe and, in 2024, reduced the cost of its ad-free service by 40%. However, the European Consumer Organisation (BEUC) raised concerns that these adjustments still fail to provide users with a genuine choice. As a result, the Commission has warned that additional sanctions may follow, including daily fines of up to 5% of Meta’s average global daily turnover.

EU regulations pose a substantial challenge for Meta, whose business model relies heavily on user-data-driven advertising. In Q1 2025, the company reported USD 42.3 billion in revenue, of which USD 41.4 billion (97.8%) came from advertising. Restrictions on ad personalization could therefore directly impact Meta’s primary revenue stream. The Commission’s actions are part of a broader regulatory crackdown on Big Tech. Since 2023, Meta has been fined more than EUR 2 billion for various violations of EU rules. Other tech giants have faced similar penalties; for instance, Apple was fined EUR 500 million in 2025 over breaches related to its App Store.

The European Commission’s recent actions against Meta underscore the EU’s increasing determination to enforce digital regulations and uphold consumer rights. However, the long-term impact of these measures will depend on consistent and rigorous enforcement. As tech giants continue to consolidate their dominance, the EU faces the challenge of balancing consumer protection with the need to foster competition in the digital marketplace.

Krystian Łukasik