Economic Weekly 29/2025, July 25, 2025

Published: 25/07/2025

Table of contents

AI and Big Data Drive Demand for Highly Skilled Specialists

47% share of industrial enterprises using digital technologies in 2023

8% share of Big Data-using enterprises that employed highly qualified specialists in 2023

6% share of AI-using enterprises that employed highly qualified specialists in 2023

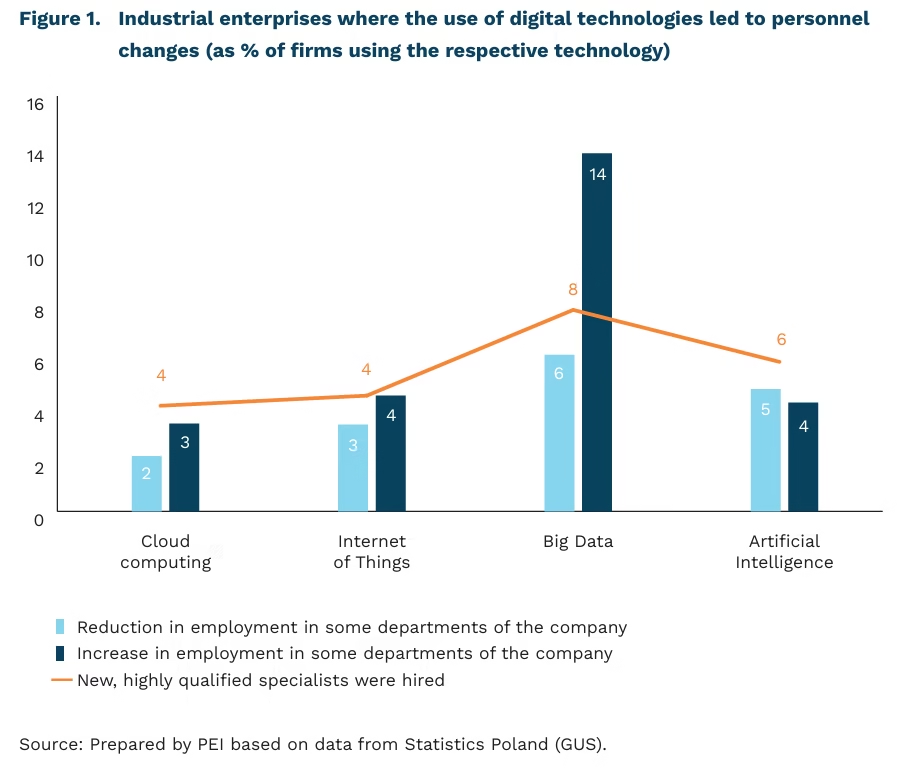

In 2023, 47% of industrial enterprises used advanced digital technologies1. Among them, 38% utilized cloud computing, 25% adopted the Internet of Things (commonly known as smart devices or systems), 2% used Big Data, and 3% implemented Artificial Intelligence (AI). According to data from Statistics Poland (GUS), the adoption of these technologies has so far led to limited changes in employment structures. Although the share of firms using digital technologies increased in 2024, employment change data was not collected for that year.

Staffing changes were reported by 8% of firms using cloud computing, 11% using the Internet of Things (IoT), 20% using Big Data, and 13% using artificial intelligence (AI). The highest share of job reductions occurred among companies using Big Data and AI (6% each). The largest increases in employment were also seen in firms adopting Big Data (14%), followed by AI and IoT (4% each). The smallest increase was reported by cloud computing users (3%).

Big Data (8%) and AI (6%) adoption most frequently led to the hiring of highly qualified specialists, reflecting the growing strategic importance of these technologies. Firms using Big Data primarily hired data scientists, programmers, and heads of maintenance or production, while those adopting AI most often recruited programmers and data scientists.

Among the 24 enterprises that reported both job reductions and increases due to the adoption of cloud computing, 12 experienced a net increase in employment, 3 saw a decrease, and 9 reported no change in overall staffing levels. Among 6 companies implementing IoT, 2 reported increased employment, 3 reported decreases, and 1 reported no change. Of the 3 companies using Big Data, 1 experienced a net increase, 1 a decrease, and 1 no change. Overall, the industrial sector still makes limited use of advanced digital technologies, although the pace of adoption is accelerating – a trend that may increasingly affect employment structures. So far, staffing changes have largely benefited highly skilled professionals, particularly data scientists and programmers.

- Based on questionnaire survey data from Statistics Poland (GUS) covering a sample of 5,642 industrial enterprises in 2023.

Magdalena Lesiak

Too Few Orders, Too Much Production Capacity – Challenges for Businesses in Q2 2025

-29 p.p. demand gap in the sales market in Q2 2025

81.9% capacity utilisation rate in Q2 2025

44% share of companies citing insufficient or uncertain demand as the main barrier to growth in Q2 2025

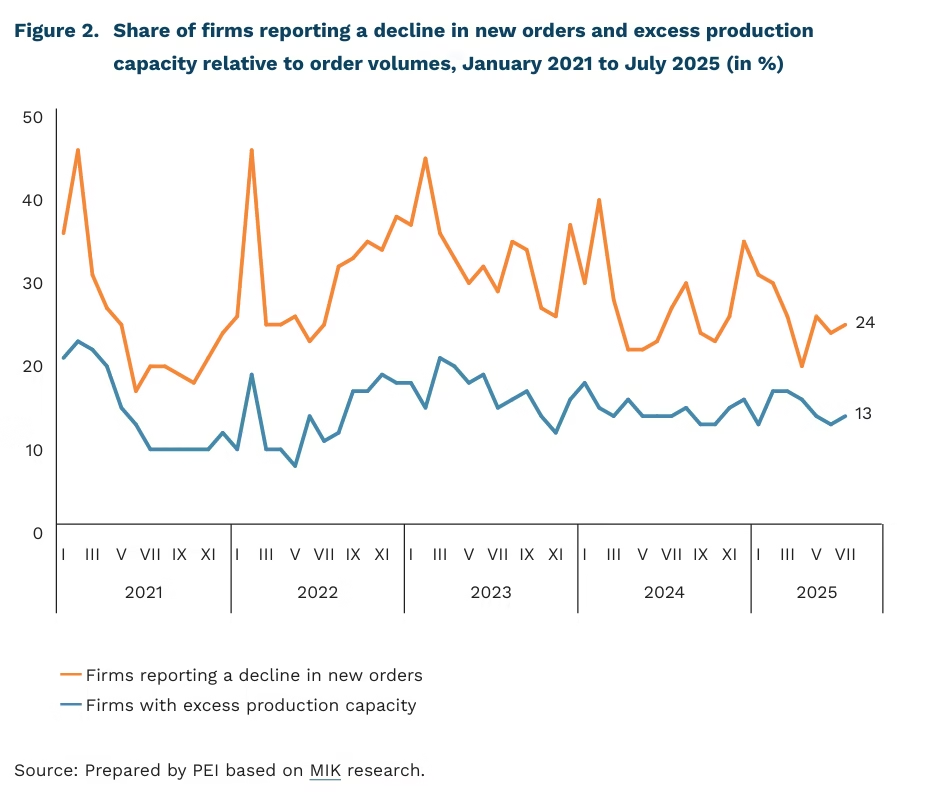

In Q2 2025, non-financial enterprises employing at least 10 people recorded a negative demand gap of 29 percentage points in the sales market, according to data from the NBP’s Quick Monitoring Survey. This means demand for their products was lower than their production capacity. In the supply market, the issue was less pronounced, though still evident, with a gap of -16 percentage points. Compared to Q1 2025, the supply surplus widened in both the sales and supply markets (by 2 p.p. and 3 p.p., respectively).

The supply-demand imbalance was particularly pronounced in the sales of durable consumer goods (-48 p.p.) and intermediate goods (-43 p.p.). The supply-demand imbalance was particularly pronounced in the sales of durable consumer goods (-48 p.p.) and intermediate goods (-43 p.p.). In these sectors, companies have a significant share of unused production capacity, while the market is unable to absorb the volume of goods offered. Although the situation was somewhat better in construction, business services, and consumer services (-28 p.p., -28 p.p., and -27 p.p. respectively), these sectors also remained in negative territory. Only non-market services (i.e. public administration, education, and healthcare) saw demand outstrip supply (+11 p.p.), a quarter-on-quarter increase of 8 percentage points.

Weak demand in Q2 2025 brought capacity utilisation down to 81.9%, with the steepest declines recorded in services, transport, and construction. Modest increases were observed in trade and industry sectors dependent on the German economic cycle. Monthly results of Monthly Business Climate Index (MIK) similarly indicate that firms with excess capacity continue to outnumber those reporting capacity shortages. This reflects mounting pressure to cut costs and postpone investment decisions. As more companies report declining orders, the share of firms declaring excessive production capacity continues to grow.

According to NBP surveys, the main medium-term barrier to growth for businesses remains weak or uncertain demand. Among firms expecting no growth, 44% cited this as the primary constraint. The issue is particularly acute for companies reliant on foreign demand, including those in global supply chains (48%), producers of durable consumer goods (70%) and capital goods (51%), and trading companies (54%).

Demand forecasts for the third quarter of 2025 remain stable. This reflects improved sentiment among producers of capital goods and providers of business services, which has offset weaker expectations among manufacturers of other goods and services. Shortterm export prospects have also strengthened – for both specialized and non-specialized exporters – potentially softening the impact of subdued domestic demand. However, this does not yet point to a lasting recovery.

Aleksandra Wejt-Knyżewska

Retirement Savings of Poles Continue to Grow

PLN 24.7 billion increase in retirement savings held by Poles in 2024

656,000 new retirement accounts opened in 2024; over half were Employee Capital Plans (PPK)

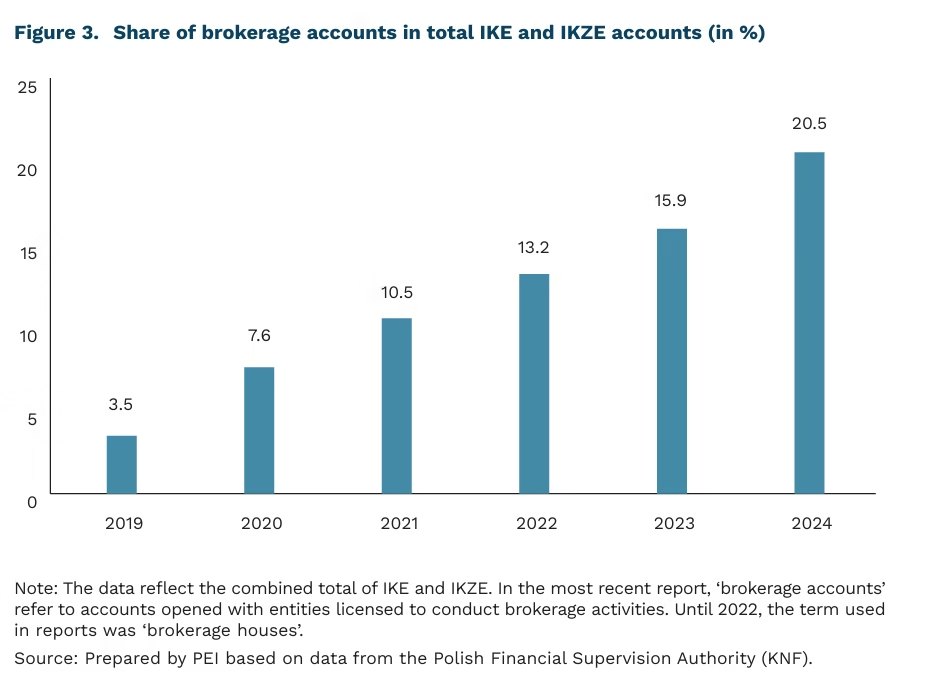

From 3.5% to 20.5% increase in the share of brokerage accounts among all Individual Retirement Accounts (IKE) and Individual Retirement Protection Accounts (IKZE)

The Draghi Report identifies the underdevelopment of Europe’s retirement savings market as one of the structural causes behind the EU’s declining global competitiveness. Pension assets held in capital markets represent just 32% of GDP in the EU, compared to 142% in the United States. This constrains Europe’s ability to finance long-term and higher-risk investments. In Poland, the gap is even more pronounced. According to data from the Polish Financial Supervision Authority (KNF), retirement assets amounted to 8.7% of GDP in 2015, dropped to 7.9% in 2019, and rose modestly to 8.4% in 2024. However, the increasing number of investment accounts and the growing popularity of Employee Capital Plans (PPK) indicate a positive trend toward deeper participation in capital markets. The most significant growth in 2024 occurred in the PPK system, alongside Individual Retirement Accounts (IKE) and Individual Retirement Protection Accounts (IKZE). There was also a marked increase in brokerage accounts held under IKE and IKZE accounts – from 3.5% in 2023 to 20.5% in 2024 – suggesting a growing appetite among Poles for active investment of long-term savings.

The volume of retirement savings in Poland is steadily increasing. The total value of assets held in pension schemes rose from PLN 282.9 billion at the end of 2023 to PLN 307.6 billion by the end of 2024, marking an 8.7% increase. The sharpest growth was recorded in Employee Capital Plans (PPK), whose assets surged by 39.0%, from PLN 21.8 billion to PLN 30.3 billion. Double-digit growth was also observed in Individual Retirement Protection Accounts (IKZE), which grew by 31.8% (PLN 2.9 billion), Individual Retirement Accounts (IKE), up 25.1% (PLN 4.6 billion), and Employee Pension Schemes (PPE), up 14.7% (PLN 3.8 billion). In contrast, assets held in Open Pension Funds (OFE) increased by just 2.4%, or PLN 4.9 billion.

The significance of OFE in Poland’s retirement savings landscape is steadily declining. While OFE remains the largest pension product in Poland – managing assets worth PLN 213 billion – its share of the retirement market has decreased consistently, from 80.4% in 2020 to 69.3% in 2024. This trend stems from the lack of new participants and the ageing profile of existing members, whose funds are gradually being withdrawn from the capital market and transferred to the Social Insurance Institution (ZUS) as part of the so-called ‘OFE slider’ mechanism. Consequently, OFE is the only pension vehicle with a negative net inflow, which means that withdrawals exceed new contributions, and any growth in assets is attributable solely to investment returns. Encouragingly, this shortfall is being offset by rising contributions to PPK. In 2024, OFE recorded a net outflow of PLN 5.7 billion, whereas net inflows to PPK reached PLN 6.6 billion, helping to maintain capital market liquidity.

More Poles are saving for retirement through capital market instruments. In 2024, the total number of retirement accounts increased by 656,000. The largest growth was observed in PPK, with 372,000 new participants, primarily through automatic enrolment. IKE and IKZE followed, with 169,500 and 109,100 new accounts, respectively. New enrolments in OFE and PPE remained minimal, totalling fewer than 5,500. Notably, brokerage accounts within IKE and IKZE are gaining popularity, with their share rising from just 3.5% in 2019 to 20.5% in 2024. In 2024 alone, over 100,000 new brokerage accounts were opened, which account for roughly 55% of all new IKE and IKZE accounts that year.

Withdrawals from PPK remain moderate. The total volume of withdrawals rose from PLN 7.2 billion in 2023 to PLN 8.7 billion in 2024, a change driven almost entirely by the program’s expansion and rising wages. In relative terms, the scale of withdrawals has remained stable: payouts as a share of new contributions rose slightly from 21.6% to 22.4%, while their share relative to net assets in PPK fell from 7.1% to 6.4%. While early withdrawals are not in the long-term interest of savers, they remain a legal option – one that can help build trust in the system.

Marcin Klucznik

Elderly Care in Poland Relies Heavily on Family Support

5.5% share of Poles aged 50-70 providing regular in-home personal care in 2022

35% share of people aged 80+ regularly receiving personal care from a household member in 2022

2.4-2.7% of GDP estimated value of informal caregiving work in the EU

In Poland, long-term care (LTC) for older adults depends largely on informal support – primarily from family members – while public spending on formal care remains limited. Public expenditure on LTC accounts for just 0.5% of Poland’s GDP, with approximately 70% of all care provided at home by informal caregivers. By contrast, other OECD countries offer significantly broader access to formal LTC services, both in institutional settings and through at-home care allowances.

According to the 2022 SHARE survey, around 5.5% of Poles aged 50-70 reported providing regular, long-term personal care to a household member. Respondents were asked whether, over the past year, they had helped someone in their household daily or nearly daily for at least three months with activities such as bathing, getting out of bed, or dressing. The question excluded short-term or occasional support, focusing instead on sustained, long-term care that often limits or prevents engagement in paid work. This age group (50-70) is particularly important, as it is during this stage of life that many individuals, especially women, choose to retire early or opt not to continue working after reaching retirement age due to increasing caregiving responsibilities for elderly family members.

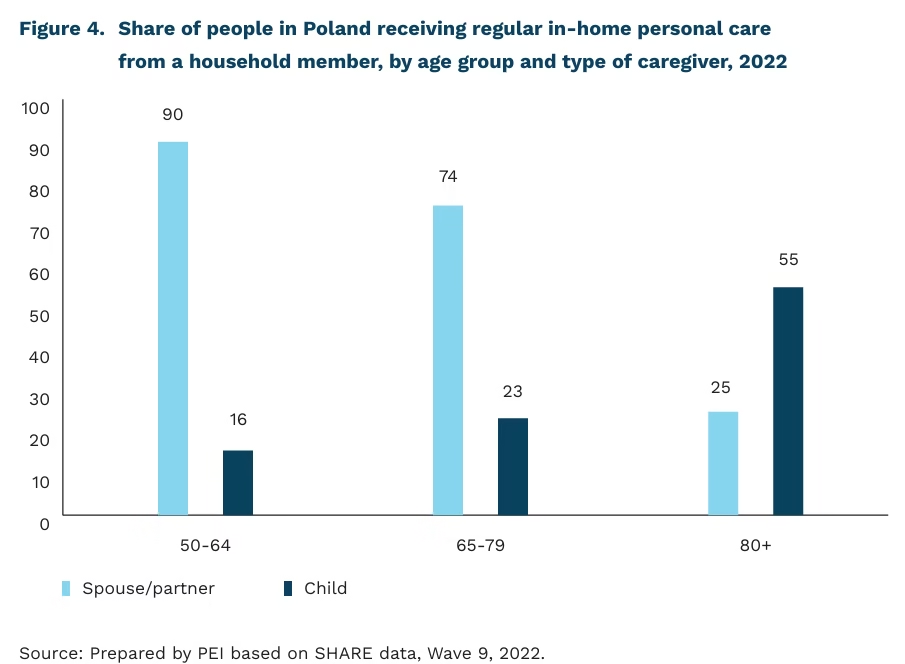

The share of people receiving regular in-home personal care rises sharply among those aged 80 and over. In this oldest age group, 35% report receiving consistent assistance with daily activities such as bathing and dressing, compared with 26% among those aged 50-64 and 20% among those aged 65-79. As the number of people aged 80 and over is projected to nearly triple by 2060, the demand for long-term care will continue to rise. The current model – relying heavily on informal, family-based support – may prove insufficient in the face of these demographic changes.

The source of care for older adults shifts significantly with age. Among younger seniors (aged 50-64), support is provided primarily by partners, while adult children are rarely involved. However, as care recipients age, the role of the partner diminishes, often because they too require assistance or are no longer living. Among those aged 80 and over, this dynamic reverses: children – predominantly daughters, who account for 62% of all informal caregivers – become the main providers of care.

Although informal caregivers are often viewed as a cost-saving alternative to public long-term care, their contribution carries considerable economic implications (WHO, 2024). In both Poland and the EU, the value of unpaid caregiving is estimated at between 2.4% and 2.7% of GDP. This includes not only the time spent providing care but also the economic costs resulting from reduced labour market participation. These often invisible burdens translate into lower tax revenues, diminished productivity, and increased pressure on social protection systems. As such, greater recognition and support for informal caregivers are essential to address the growing needs of ageing societies in Poland and across Europe.

Dominika Prudło

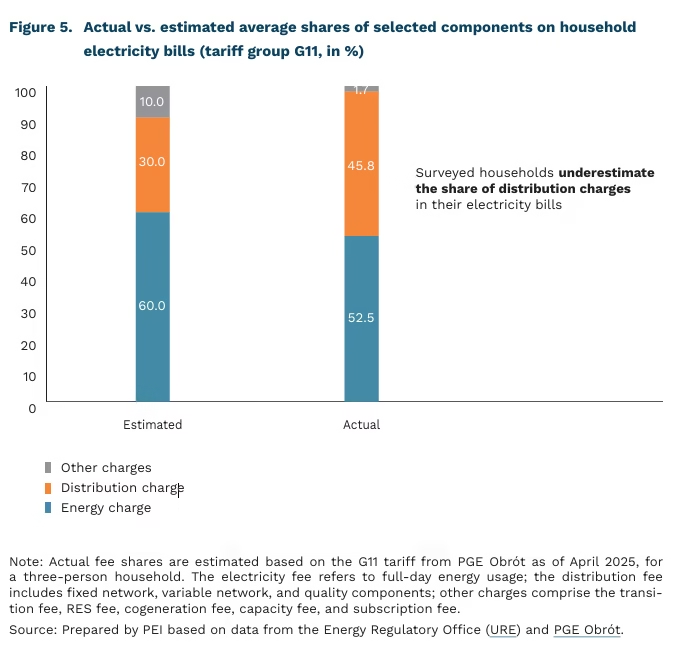

Lack of Awareness Fuels Poles’ Concerns Over Rising Electricity Bills

66% share of Polish households concerned about an uncontrolled rise in electricity prices

41% share of Polish households that f ind electricity bills easy to read, and 40 find electricity bills easy to understand

23% share of Polish households that know their annual electricity consumption

Awareness of electricity use among Polish households remains low and calls for educational action. This is the key conclusion of a survey commissioned by the Energy Regulatory Office (URE) and conducted in April-May 2025. The aim of the study was to gauge consumers’ opinions and attitudes toward the electricity market in Poland.

A major issue for households is understanding the components of their electricity bills and how those components are calculated. Only 29% of respondents said they understood how the energy market works and how prices are set. Just 47% correctly identified energy companies as the entities responsible for calculating household electricity tariffs. Meanwhile, 41% and 40%, respectively, said their electricity bills were readable and understandable. However, half of the surveyed households admitted that they either did not know, or knew but did not understand, why usage and distribution charges appear as separate items on their bills. The URE study also shows that households incorrectly estimated the share of these charges in the total cost of electricity.

Two out of three Polish households report concerns about an uncontrolled rise in electricity prices in the future. Nearly 75% say their electricity bills have become more burdensome compared to 2-3 years ago. At the same time, only 23% state they can estimate their annual electricity consumption. According to URE, surveyed households also show limited awareness of actions that could help reduce their electricity bills. While 73% are aware that it is possible to switch electricity providers, only 13% have ever done so. Moreover, 44% have never heard of dynamic electricity tariffs. A greater share of respondents believe that EU policy (61%) and national policy (60%) have a stronger impact on electricity bills than their own efforts to reduce energy use (40%).

Half of respondents expect the government to take more responsibility for controlling and mitigating price increases. In addition, 39% believe electricity bills should be more transparent. Over 54% agree that so-called energy price freezes are beneficial for the Polish economy, despite their estimated cost reaching nearly PLN 5.5 billion in 2025 alone. The relatively low public awareness of how the energy market works, and the tools available to manage household consumption, may increase expectations toward government intervention and reduce incentives to take individual action to lower bills.

Wojciech Żelisko

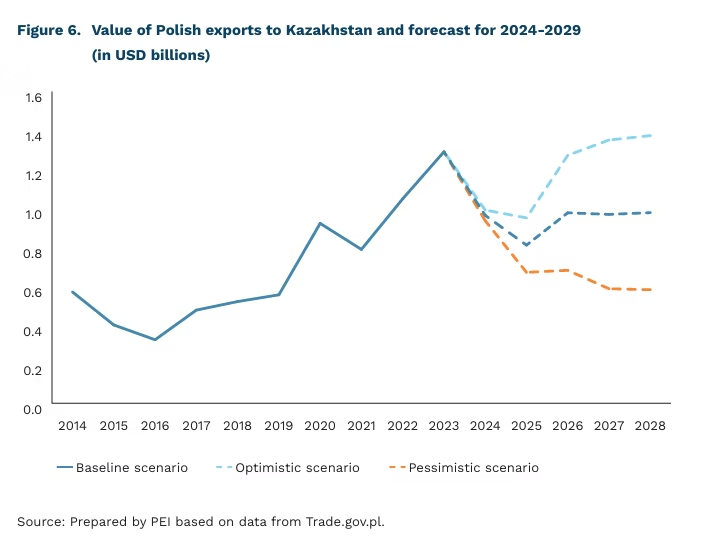

Kazakhstan: Poland’s Strategic Partner in Central Asia

3.5% projected average annual GDP growth of Kazakhstan (in constant prices) from 2025 to 2030

USD 142.3 million value of Polish agri-food exports to Kazakhstan in 2024

Kazakhstan remains Poland’s key trading partner in Central Asia. The two countries have launched talks aimed at removing barriers in agri-food trade, which reached USD 142.3 million in Polish exports to Kazakhstan in 2024. A central point of the negotiations is the lifting of the transit ban, which currently prevents Polish exporters from accessing other Central Asian markets via Kazakhstan. Preliminary estimates suggest total Polish exports to Kazakhstan reached around USD 964.2 million in 2024, marking a 25.3% year-on-year decline. However, final figures may approach the more optimistic scenario of USD 1 billion. Between 2024 and 2029, the fastest nominal export growth is expected in Polish bakery products, confectionery, and sweets. A successful conclusion of trade talks would further boost sales in the agri-food sector.

Kazakhstan is leveraging its geographic location and vast natural resources to attract trade and investment. The country’s economy is driven by abundant reserves of oil, natural gas, and uranium – of which Kazakhstan is the world’s leading producer, accounting for 39% of global output in 2023. These resources underpin the expansion of the extractive and metallurgical industries and fuel export growth. Strategically located along key trade routes connecting Europe and Asia, Kazakhstan is investing heavily in transport infrastructure upgrades. In addition, to improve the investment climate, the country has introduced numerous economic and administrative reforms (e.g., the new Tax Code of 2017), and established special economic zones and institutions to support foreign capital, such as the Astana International Financial Centre.

Kazakhstan’s economic outlook for the coming years remains optimistic, though it depends heavily on commodity market trends and the progress of domestic reforms. According to the International Monetary Fund, Kazakhstan’s nominal GDP is expected to reach USD 425.9 billion by 2030, which would imply an average annual growth rate of 6.9% between 2025 and 2030. In real terms, growth is projected to average 3.5% annually. This robust performance is expected to be supported by strong domestic demand, driven by rising household incomes and consumer credit, as well as ongoing raw material exports. However, Kazakhstan’s economy remains highly sensitive to global oil and gas prices, posing a risk to long-term stability. External threats include a potential slowdown in major economies, rising regional tensions, and the possibility of secondary sanctions. Successful implementation of planned reforms, combined with favourable external conditions, would support further strengthening of the Kazakh economy.

Piotr Kamiński

Voucher Could Boost Engagement in Cultural Activities

50.9% share of Poles who participated in cultural activities in the past year; EU average: 51.7% (2022)

77% vs 33% participation rate among people with higher education vs those without a secondary qualification

EUR 500 value of the cultural voucher available to 18-year-olds in Italy

According to Eurostat data from 2022, approximately 50.9% of Poles reported participating in cultural activities in the previous 12 months such as going to the cinema, concerts, museums or other cultural institutions. This figure places Poland close to the concerts, museums or other cultural institutions. This figure places Poland close to the EU average. However, such averages mask substantial inequalities in cultural participation between groups of differing socioeconomic status. Poland, alongside France, Romania and Portugal, is among the EU countries where institutional cultural engagement is most strongly correlated with education level: only 33% of those without a secondary qualification engaged in cultural activities last year, compared to 77% of university-educated individuals.

Similar findings emerge from research by the National Centre for Culture. Just 12% of people with basic or vocational education visited an art gallery in the past year, compared to 49% of those with higher education. This socioeconomic “participation gradient” is evident across nearly every form of cultural engagement.

In this context, it is worth examining instruments used in other countries to boost cultural participation, particularly among young people from lower socioeconomic backgrounds, thus supporting the “democratisation of culture.” A notable example is Italy’s “18app” programme, under which every citizen receives a EUR 500 cultural voucher upon turning 18. The voucher can be used for cinema, theatre, museum and concert tickets, or to purchase books. Introduced in 2016, the scheme has inspired similar initiatives in France (2021), Spain (2022), and Germany (2023).

Research published this month on the impact of Italy’s programme found that it significantly increased cultural participation, particularly among those whose parents had lower levels of education. While the effects were small or statistically insignificant for young people from more educated households, beneficiaries from less-educated backgrounds were markedly more likely to attend cultural events. Among this group, cinema attendance rose by 20%, classical music concerts by 45%, popular music concerts by 23%, and museum visits by 16%. The programme also generated a spillover effect, increasing cultural consumption among other household members.

The researchers suggest that the voucher helped overcome financial barriers and provided motivation for those from less privileged backgrounds to engage in cultural life. The Italian experience indicates that a similar initiative in Poland could help reduce participation gaps and encourage new social groups to interact with cultural institutions.

Marcin Lewandowski