Economic Weekly 12/2026, March 27, 2026

Published: 27/03/2026

Table of contents

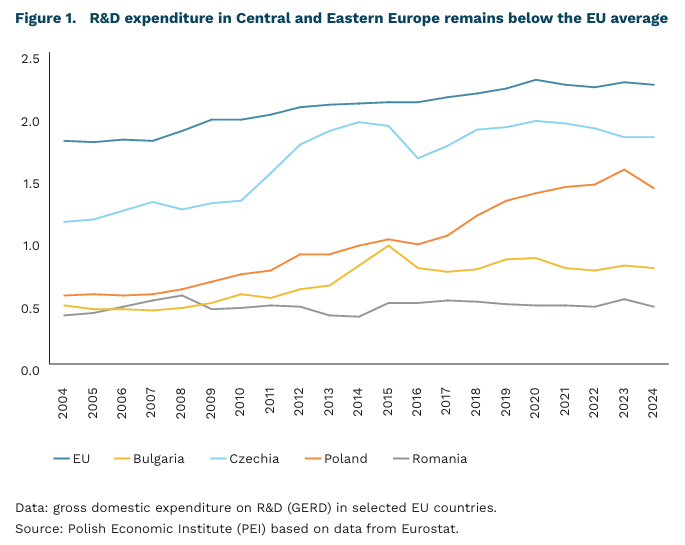

Poland has the strongest fundaments in the region for innovation-driven growth

1.4% of GDP was Poland’s R&D expenditure in 2024

Over the past two decades, the countries of Central and Eastern Europe have been among the fastest in the world to increase their level of wealthiness. After joining the EU, some of them more than doubled their per capita income by benefiting from capital inflows, improved infrastructure, rising worker qualifications, and deep integration into European value chains. Poland stands out within this group as a special case: as the region’s largest economy, it became one of the main beneficiaries of integration with the EU market and one of the most successful examples of development based on exports, investment, and technology adoption. However, the potential of this growth model is gradually being exhausted, among other things because of rising labor and energy costs. As a result, the future direction of Poland’s economic development has become the subject of increasingly intense economic debate.

A World Bank report shows that, compared with other CEE countries, Poland has the strongest fundaments for innovation-driven growth. The country has a relatively strong educational base, a significant industrial base, and a growing ICT sector. It also stands out for having the most developed startup ecosystem in the region. According to the report, around 3,000 startups operate in Poland, and the country can boast 14 unicorns[1], placing it above the EU median. Spending on research and development (R&D) is also gradually increasing, reaching 1.4% of GDP in 2024, although it still remains below the EU average of 2.2%. It is worth remembering, however, that R&D spending typically rises with the level of prosperity, and Poland’s result falls within the typical range for countries with a similar GDP per capita. In the case of converging economies such as Poland, it is often more efficient to use foreign solutions and adapt them, which naturally limits the scale of domestic R&D spending compared with more technologically advanced economies. This does not change the fact that civilian R&D expenditure can generate high long-term returns and support productivity growth (Fieldhouse and Mertens, 2023).

For Poland and the entire CEE region, the most realistic path is neither to remain permanently an imitative economy nor to attempt an immediate leap into the ranks of global technological leaders. A more rational strategy appears to be selective leadership: continued efficient absorption of technology where domestic development lacks economic justification, combined with building a domestic advantage in those niches where it is possible to create and capture intellectual value. Innovation in Poland will not be the result of a single program or one fashionable sector. Rather, it will stem from a long-term improvement in the quality of institutions, management, cooperation, and capital allocation. Only on such a foundation can higher R&D spending, startup development, and support for new technologies deliver lasting results.

- A startup valued at least USD 1 billion.

Piotr Kamiński

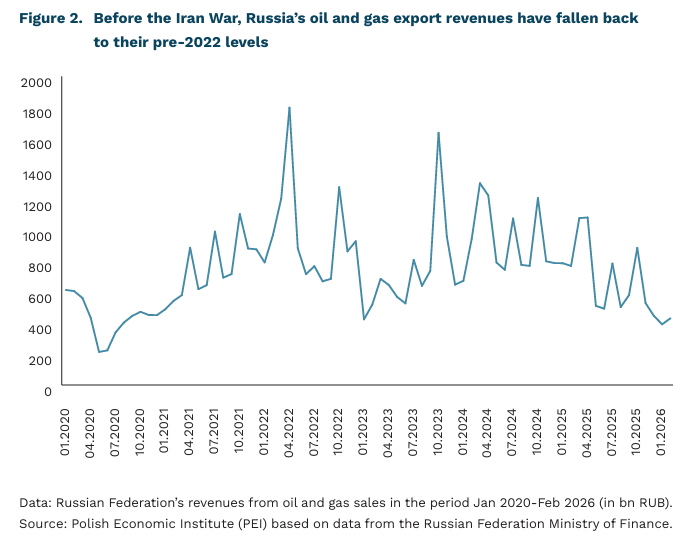

Russia Benefits Economically from the Iran War

approx. USD 25 the discount on Russia’s Urals crude stood at in 2025

75% the price of Russian oil has risen over the past month

The American-Israeli attack of Iran has caused a dramatic increase in oil prices on global markets. Rising oil prices give Russia hope of reversing the adverse trends of recent months. In 2025, Russia’s revenues from oil and gas exports fell significantly, as a result of both ample supply on global commodity markets and sanctions. Sanctions pressure caused lower prices for Russian crude. In 2025, the discount on Russia’s Urals crude relative to Brent rose from a few US dollars per barrel to more than USD 25. In addition, in February 2026 Russian oil supplies to global markets fell short of forecasts due to successful Ukrainian attacks on refineries and export infrastructure. According to the International Energy Agency (IEA), Russia’s oil exports fell to 6.6 million barrels per day in February, the lowest level since the start of the full-scale invasion of Ukraine. As a result, Russia’s export revenues declined once again. This was largely linked to tightening sanctions pressure from the EU and the US in 2025 and 2026. For example, the EU ban on importing products derived from the processing of Russian oil caused Russian exports to India to fall in February to around two-thirds of their level at the beginning of 2025. Declining budget revenues from exports make it harder to sustain the same scale of public spending that has flowed into the economy over the past four years of war.

Tehran’s threats to completely close the Strait of Hormuz and to attack energy infrastructure in the region are increasing the risk of further rises in oil prices. The war in Iran is already boosting revenues for the Russian budget: the price of Russia’s Urals crude has risen by around 75% over the past month, surpassing the threshold of USD 100 per barrel. According to FT estimates, Moscow may receive an additional USD 3.3-4.9 billion in budget revenues by the end of March. The key question, however, will be how long the war in the Middle East lasts and whether calls to ease sanctions on Russia intensify. A worrying signal is that the US administration has already softened some sanctions, for example by allowing purchases of Russian oil already at sea. Growing tensions among EU states may in turn be reflected in the fact that the European Commission has postponed the presentation date of the REPowerEU plan concerning the phase-out of imports of Russian raw materials.

The war and a blockade of the Strait of Hormuz could also cause fertiliser shortages and its higher prices, which would in turn increase food prices, something that would also benefit Moscow. The Gulf states are important exporters of certain fertilisers, and a large share of global fertiliser trade passes through the Strait of Hormuz. According to Argus estimates, closing the Strait of Hormuz threatens to disrupt 20-50% of international trade in urea, sulphur, phosphates and ammonia. Russia, meanwhile, is one of the world’s largest fertiliser exporters (around a 15% share of the global market), as well as the largest exporter of wheat (18% of global exports). It cannot be ruled out that Moscow will try to exploit the situation on agricultural and food markets in a manner similar to 2022-2023, when it blocked Ukrainian exports and increased its own role in supplies to the Middle East.

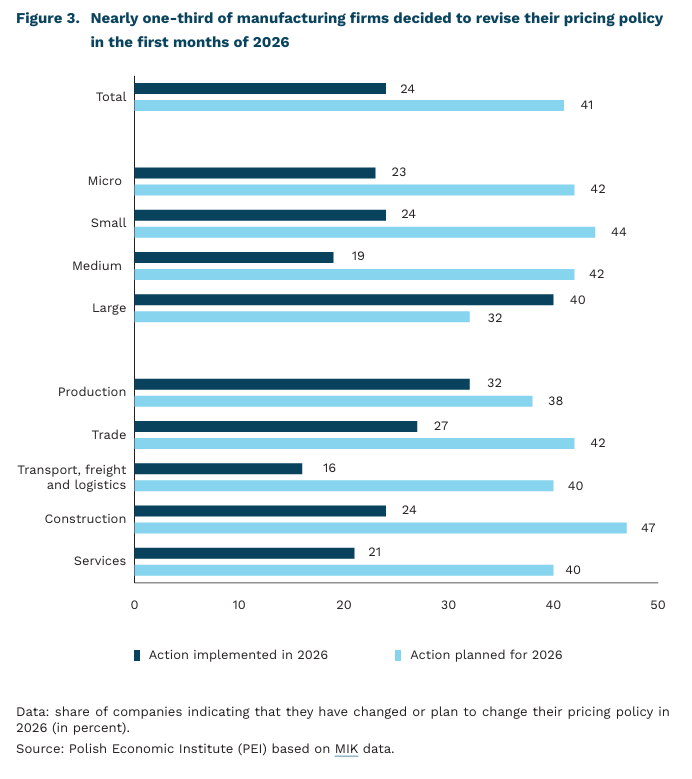

Nearly one in four companies has revised its pricing policy this year

41% of firms plan to adjust their pricing policies in 2026

47% of entrepreneurs in the construction sector declare they will modify their pricing policy before the end of 2026

40% of large companies updated their pricing policies at the beginning of 2026

Nearly one quarter of firms revised their pricing policy in the first two months of 2026, according to the March MIK (Monthly Business Climate Index). However, as many as 41% of companies declare that they intend to undertake such action later this year. Adjusting the pricing policy ranks as the third most common business measure in 2026, following wage increases and cost-cutting initiatives.

Companies in the manufacturing sector were particularly likely to alter their pricing policies at the beginning of the year: 32% have already done so, and 38% plan to do so in the coming months. In the trade sector, these shares amount to 27% and 42%, respectively, and in construction – 24% and as much as 47%. The propensity to adjust prices is similar across almost all firm-size categories. The exception is large enterprises, which show the strongest inclination toward price changes. According to the February 2026 survey by the Polish Economic Institute (PIE), conducted as part of MIK, in the last quarter of 2025 more than one-fifth of firms increased the price of their main product or service compared with the previous quarter, and all sectors were more likely to raise prices than to reduce them. At the same time, 34% of companies declared price increases in the first quarter of 2026.

Artificial intelligence (AI) is increasingly assisting firms in setting prices more quickly and accurately, by continuously analysing changes in demand, competitive behaviour, and cost levels. Available analyses show that AI-based solutions enable companies to adjust prices automatically in real time and to better forecast customer behaviour. In practice, this means moving away from simple, one-off markups toward more flexible and strategically designed pricing models.

The tendency among firms to adjust their pricing policies is part of a broader pattern of persistent cost pressures. Despite declining inflation and the protection of households from energy-price hikes through Energy Regulatory Office (URE) interventions, companies continue to operate under conditions of elevated energy and labor costs. According to the latest Grant Thornton report, 60% of medium-sized and large firms plan to raise prices in 2026, most often in the range of 5-7%, clearly above the inflation experienced by consumers. In its latest inflation projection, the National Bank of Poland (NBP) forecasts that in 2026 the CPI will reach 2.3%. This demonstrates that price-policy adjustments are becoming a necessary tool for many industries to balance rising cost burdens and maintain competitiveness at a time when both global and domestic factors continue to strongly shape operating costs.

Katarzyna Zybertowicz

Growing popularity of vocational schools, especially those training electricians

15.1% of all upper-secondary school graduates in Poland in 2024 were graduates of first-stage sectoral vocational schools

78% of graduates of first-stage sectoral vocational schools were trained in the ten most popular occupations

53% of graduates of first-stage sectoral vocational schools were employed in the second year after completing school

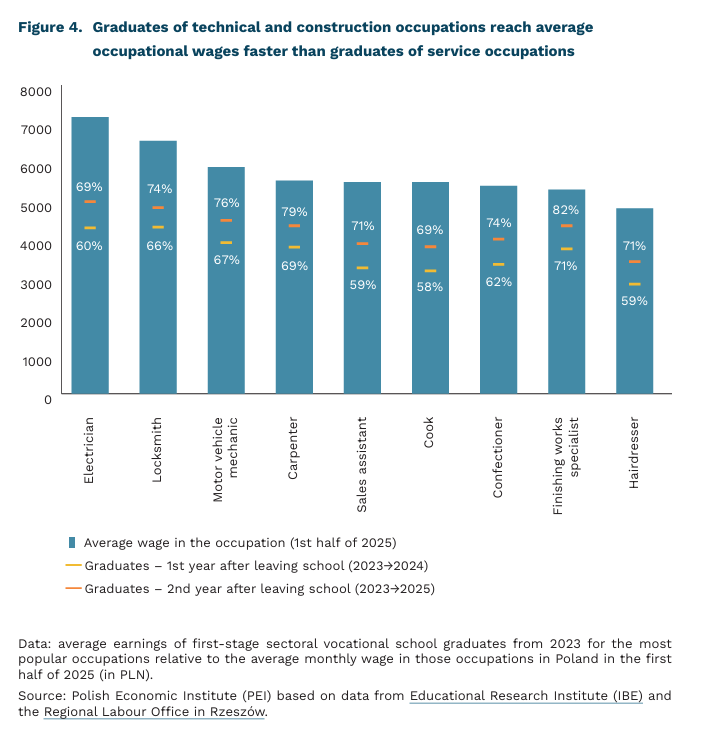

The share of graduates of first-stage sectoral vocational schools among all upper-secondary school graduates has been clearly increasing. In 2020[2], they accounted for 10% (38.9 thousand) of graduates, while in 2024 their share had risen to 15.1% (68.6 thousand). This represents an increase of more than 76% over four years. At the same time, the share of general secondary school graduates declined, from 47% in 2020 to 41% in 2024, and the share of technical secondary school graduates fell from 29% to 25%. In practice, this means a gradual departure from a model in which general secondary education clearly dominates, toward a more balanced structure with a strong vocational pathway preparing young people for specific professions. The growing popularity of this type of education has been accompanied by the expansion of first-stage sectoral vocational schools. According to Statistics Poland (GUS), their number rose by 11% between 2017 and 2024, from 1,167 to 1,299. 53% of graduates of first-stage sectoral vocational schools were employed in the second year after completing school PEI Economic Weekly March 27, 2026

The structure of education in first-stage sectoral vocational schools has been concentrated and stable for several years. Among graduates from 2023[3], the most popular occupation was motor vehicle mechanic, followed by hairdresser and cook. Altogether, as many as 78% of all graduates were trained in the ten most frequently chosen occupations[4]. The list of the most popular occupations has changed very little since 2020, which shows a high degree of repetition in educational choices and in the profile of vocational school offerings. Against this background, the occupation of electrician stands out in particular. Between 2020 and 2023, the number of graduates of schools or classes with this profile increased by more than half, from 1.6 thousand to 2.5 thousand, which may reflect rising market demand. Since 2018, electrician has consistently been identified as a shortage occupation[5]. In 2026, a shortage was forecast in 2/3 of counties in Poland.

In the second year after completing first-stage sectoral vocational school, graduates were clearly present on the labour market. More than half of them were working. In March 2025, 43% of graduates from the 2023 cohort were employed, more than twice as many as in September 2023, when 19% were working immediately after completing their education. The share combining further education and work was 10%. Employment was highest among graduates in the occupations of locksmith, carpenter and electrician. The remaining graduates either continued their education only (17%), were registered as unemployed (10%), or were absent from administrative registers (20%)[6]. The highest share of registered unemployed persons was among sales assistants and cooks.

The pace at which vocational school graduates reach average wages differs clearly across occupations. The highest earnings can be expected by graduates in the occupations of electrician and locksmith. After two years, the closest to average occupational pay are specialists in finishing works in construction, carpenters and motor vehicle mechanics, while a larger gap persists in service occupations such as cook, hairdresser and sales assistant. First-stage sectoral vocational school offers a relatively fast entry into working life, but the scale of wage gains depends on the chosen occupation and demand for specific skills.

2. It was the first cohort of graduates from the first-stage sectoral vocational school launched after the reform initiated in 2017. It was the first cohort to be taught according to the new core curriculum.

3. For graduates from 2023, the latest data are available from the monitoring of career paths of graduates from public and non-public upper-secondary schools (2025 edition). It is based on administrative data, including social insurance data from the Social Insurance Institution (ZUS) on graduates’ labour market activity.

4. The group also included: sales assistant, construction finishing works installer, electrician, confectioner, carpenter, motor vehicle electromechanic, and locksmith.

Cezary Przybył

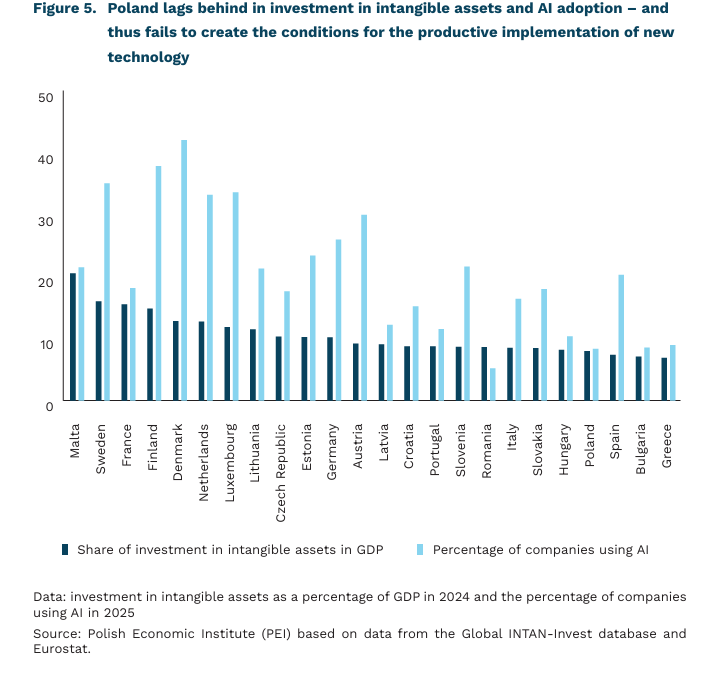

Intangible assets enable companies to fully benefit from the implementation of AI

4% is the average increase in firms’ productivity after adopting AI

16% is the level of investment in intangible assets relative to GDP in Sweden, compared with 8% in Poland

Harnessing the full potential of artificial intelligence (AI) to improve productivity requires significant complementary investments – in data, training, and management processes. These types of resources, known as intangible assets, are still poorly captured in public statistics, even though they can determine the success or failure of a company in the current phase of digital transformation. Research by the European Investment Bank (EIB), based on company data from 2019-2024, shows that the implementation of AI in organizations resulted in an average productivity increase of 4%. However, investments in intangible assets were key. A 1 percentage point increase in training expenditures boosted productivity resulting from AI implementation by 5.9%, while a 1 percentage point increase in expenditures on software and data translated into a 2.4% increase in productivity linked to AI use. By comparison, investments in fixed assets yielded small or statistically insignificant results.

According to a WIPO analysis covering 27 economies[7], including Poland, investment in intangible assets grew 3.7 times faster than investment in tangible assets between 2008 and 2024. In the countries surveyed, the average share of investment in intangible assets in 2024 was 13.6% of GDP. The leaders were Sweden with 16% of GDP, followed by the U.S., France, and Finland, where this ratio was approximately 15%. Poland was among the countries with relatively low investment – spending on intangible assets accounted for about 8% of GDP. This result was lower than in Brazil (8.5% of GDP) but higher than in Spain, Bulgaria, or Greece. Furthermore, it is worth noting that some countries ranking below the EU average in AI adoption are investing significantly in intangible assets. This applies, for example, to France, Lithuania, and the Czech Republic. This may indicate that these countries are laying the groundwork for faster AI adoption, which in turn could lead to increased productivity.

With low levels of investment in intangible assets, Polish companies may struggle to fully realize the potential of AI. Eurostat data already shows that, among EU countries, only Romania has fewer companies using AI than Poland. Meanwhile, as the cited studies show, without investment in skills, data, and organizational processes, the benefits of AI

7. The WIPO analysis covered 22 EU countries (Bulgaria, Croatia, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Italy, Lithuania, Latvia, Luxembourg, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, and Sweden) as well as Brazil, India, Japan, the United Kingdom, and the United States.

Jakub Witczak, Ignacy Święcicki

Polish youth are significantly less happy than the general population

Poland ranked 24th in the subjective happiness ranking (2 places higher than in the previous edition)

Poland ranked 56th in the subjective happiness ranking for people under 25

The authors of the World Happiness Report 2026 place Poland in 24th position, which is 2 places higher than the previous year. For the ninth time, Finland turns out to be the happiest country in the ranking, ahead of other Nordic countries and Costa Rica, which ranks 4th.

Subjective well-being is measured using the Cantril Ladder method: respondents evaluate their lives on a ladder scale with ten steps, where 0 represents the worst possible life situation and 10 the best.

The WHR also examined subjective happiness among people under 25. Serbia leads this ranking, followed by Costa Rica, Israel, and Iceland. Poland ranks 56th in this list. Such a large discrepancy between Poland’s positions in the two rankings may be due to factors such as increasing uncertainty about the future, higher levels of loneliness, and a high prevalence of anxiety and mental health issues, as reported, among others, in the “Youth Diagnosis 2026” study.

In addition to the subjective happiness rankings, this year’s report placed strong emphasis on the use and impact of social media on young people. A study conducted in 43 countries on problematic social media use (PSMU) among adolescents shows that higher levels of this measure are associated with a greater number of symptoms related to low mood, as well as lower overall happiness and life satisfaction (measured on a 10-point scale). The study also examined relationships between socioeconomic status, PSMU, life satisfaction, and psychological symptoms.

Most of the regions studied (including Central and Eastern Europe) did not show a significant relationship between socioeconomic status and the impact of PSMU on subjective life evaluation or negative psychological symptoms resulting from excessive social media exposure. This means that regardless of family status, children and adolescents experience the negative effects of PSMU to a similar extent.

The issue of social media arises at a time when more countries are introducing regulations to limit access for the youngest users. The United Kingdom, Denmark, and France are announcing or developing legislation to ban access to social media for individuals under the age of 16.

The most notable case, however, is Australia, which introduced such restrictions at the end of 2025. Public optimism in Australia regarding the expected impact of the ban was rather moderate. However, in a YouGov survey, parents reported noticing positive effects, such as improved relationships with their children and greater engagement in interactions with them and their peers.

The Polish version of such regulations focuses on banning smartphone use in schools and is set to come into force on September 1, 2026. The justification for this decision is the negative impact of smartphones on children’s academic performance. However, there is still a lack of adequate control over access to social media, whose prolonged daily use also negatively affects academic performance, both among children and young adults.

Maksymilian Pyrkowski

The EU introduces new budgetary rules and preferences in the clean tech sector

In March, the European Commission published the Industrial Accelerator Act (IAA) – a draft regulation aimed at supporting European industry, particularly low-emission sectors and those linked to clean technologies. The IAA is intended to stimulate demand for production within the EU and partner countries, for example by introducing procurement preferences in public tenders and low-emission criteria for products. The Commission notes that one of the key challenges in industrial decarbonization is the difficulty of scaling up new technologies. This is closely linked to high investment risks and barriers to accessing finance. EU leaders declared at the European Council their intention to adopt the IAA by the end of 2026.

The planned Industrial Accelerator Act should be viewed alongside the new vision for the Multiannual Financial Framework (MFF) for 2028-2034, currently under negotiation. This framework is expected to include a European Competitiveness Fund and allocate more resources to innovation and the clean technology sector. In future calls – for example under Horizon Europe – industrial criteria may gain importance, and projects that reduce critical dependencies within European supply chains may be favored. Budget negotiations have so far progressed slowly and reveal a clear divide between the “excellence” approach and the “geographical balance” approach. The former supports allocating funds primarily to the best projects and most innovative actors, while the latter emphasizes maintaining a balanced geographical distribution of funding. At the same time, traditional lines of conflict remain: the European Parliament calls for an overall budget increase (including through instruments such as a digital tax), some Member States advocate fiscal restraint (e.g. Austria opposes a 39% increase in the European Commission’s spending), and current beneficiaries seek to preserve existing allocation rules. The coming months will be crucial for negotiations on the new long-term EU budget, with a likely shift towards promoting innovation, advanced technologies, and the clean tech sector, alongside a greater role for centrally managed EU funds.

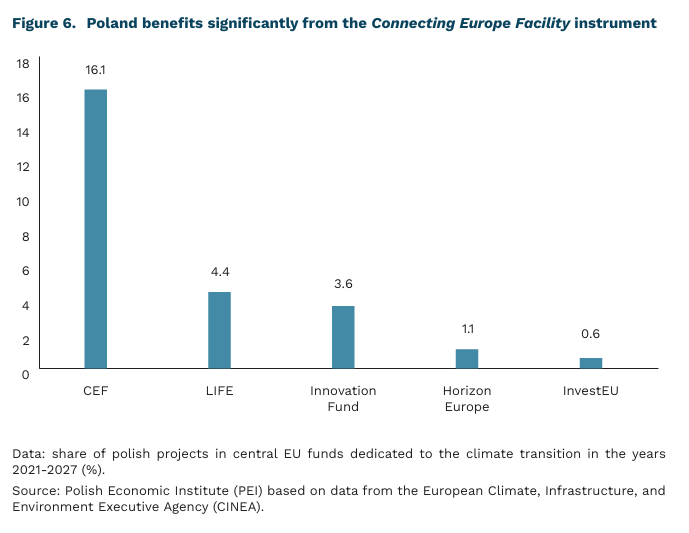

The budget for projects supporting the climate transition under centrally managed EU funds amounted to a total of EUR 50.3 billion for the 2021-2027 period. These instruments include the Innovation Fund – fully dedicated to industrial decarbonization – as well as programs with dedicated climate pillars such as Horizon Europe, the Connecting Europe Facility (CEF), LIFE, and InvestEU. Within the 2021-2027 budget, 728 projects involving Polish entities received a total of EUR 4.4 billion (8.7% of the total budget). Polish projects recorded the highest share under the Connecting Europe Facility (CEF), which supports infrastructure projects in energy and transport. Poland’s share of the CEF budget for 20212027 amounted to 14.9% in transport and 3.6% in energy, with total funding for projects involving Polish entities reaching EUR 3.7 billion.

The share of Polish projects is significantly lower under Horizon Europe, which funds research and development. In the 2021-2027 budget, projects involving Polish entities accounted for only 1.1% of total funding. However, this is an improvement compared to the previous Multiannual Financial Framework (0.8% in 2014-2020). The highest level of funding for Polish projects was recorded in the Energy pillar, where 38 projects involving Polish entities received a total of EUR 79 million. Poland’s relatively low participation in Horizon Europe grants reflects its comparatively low R&D expenditure: in 2024, it amounted to 1.4% of GDP, compared to the EU average of 2.2%.

Marianna Sobkiewicz, Marek Wąsiński, Wojciech Żelisko