Economic Weekly 17/2026 May 4, 2026

Published: 04/05/2026

Table of contents

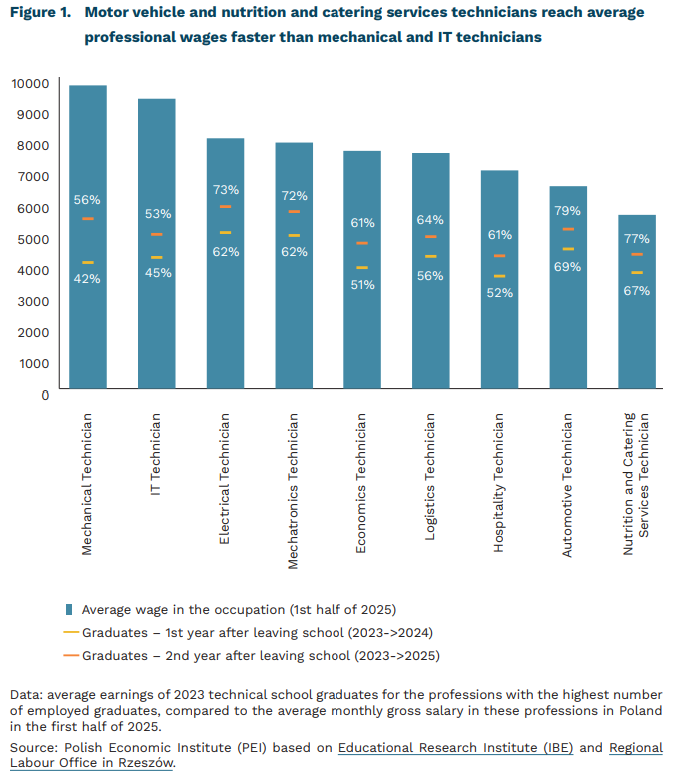

Mechanical technicians among the highest-earning technical school graduates

24.5% technical school graduates’ share of all upper-secondary school graduates in Poland in 2025

63% technical school graduates trained in the ten most popular professions

46% technical school graduates enrolled in higher education in the second year after graduation

In 2025, technical schools had 111,100 graduates, accounting for nearly 25% of all upper-secondary school graduates in Poland. Compared to 2020, the share of technical school graduates has decreased slightly (from 29%), which is linked to an increase in the share of graduates from Stage I sectoral vocational schools (we discussed this in “Economic Weekly” no. 12/2026). Technical schools hold a special place in the Polish education system: on the one hand, they provide vocational training, and on the other, they enable students to pass the matura exam and pursue further education. They combine two educational options for young people: the security of having a trade and an open path to university. The number of schools remains virtually constant. In 2017, there were 1,856 technical schools for youth (excluding special education) in Poland, compared to 1,812 in 2024.

The structure of education in technical schools is concentrated and has remained stable for several years. The most popular profession among 2023 graduates was IT technician (16.1% of technical school graduates), followed by logistics technician (9.3%) and nutrition and catering services technician (7.7%). In total, 63% of all graduates were trained in the ten most popular professions. The list of the most popular fields has remained virtually unchanged since 2019, but a shift in emphasis is visible. The share of logistics technicians is growing significantly, from 7.4% in 2019 to 9.3% in 2023 (an increase of approx. 3,000 people). At the same time, the share of nutrition and catering services technicians (from 10.6% to 7.7%) and economists (from 8.5% to 7.1%) is declining. The graduate structure reflects trends resulting from changing labor market needs.

Graduate activity in the second year after graduation indicates the parallel functioning of two paths: educational and professional. In March 2025, 38% of 2023 graduates were studying, 16% combined work and study, 30% were working, and 11% were absent from administrative records. The most common form of continuing education was pursuing a university degree (46% of all technical school graduates). Mechatronics, economics, and IT technicians pursued university studies more frequently (over 60%) than nutrition and catering services technicians (26%) and motor vehicle technicians (21%). The percentage of technical school graduates registered as unemployed was significantly lower than in other types of schools and showed a downward trend, standing at only 5% in the second year after graduation, varying by educational profile (10% for nutrition and catering services technicians vs. 3% for mechatronics technicians).

The earnings of technical school graduates differ significantly between professions. Mechanical technicians (PLN 9.7k gross) and IT technicians (PLN 9.3k gross) can potentially expect the highest earnings. Conversely, motor vehicle and nutrition and catering services technicians reach the average wage in their profession the fastest. Two years after graduation, they approach 80% of the average wage in their profession. Meanwhile, for mechanical and IT technicians, earnings after two years exceed only half of the average wage in their profession.

Cezary Przybył

Financial assistance to Ukraine and crackdown on sanctions circumvention: Europe fills the gap left by the US

EUR 90 billion the loan for Ukraine

EUR 60 billion the share of the loan earmarked for military support

8-fold the increase in EU exports of dual-use goods to Kyrgyzstan in 2022-2025

On April 23, the European Union adopted its 20th package of sanctions targeting the Russian economy and granted Ukraine a EUR 90 billion interest-free loan for 2026-2027, to be financed through EU borrowing on capital markets. The decision became possible after Hungary and Slovakia lifted their objections – in Slovakia’s case, only to the sanctions package – following the resumption of Russian oil supplies via the Druzhba pipeline and the elections in Hungary. Ukraine will be required to repay the loan only once Russia pays war reparations after the war ends. The EUR 90 billion loan is expected to cover around two-thirds of Ukraine’s external financial support needs over the next two years. Twothirds of the loan is to be allocated to military needs and one-third to macroeconomic assistance. At the same time, a significant share of military deliveries will come from European partners, which means that the funds will also support arms production in EU member states. The loan is a compromise solution reached after some member states, including Belgium, refused in December to agree to the confiscation of Russian reserves frozen under sanctions. Belgium is where most of the frozen Russian funds are deposited.

The main aim of the 20th sanctions package was to target oil and fuel exports, which are crucial to the Kremlin’s revenues. However, the package’s original provisions, initially planned for February and including a complete ban on maritime services for Russian tankers, were significantly watered down due to opposition from countries including Greece and Malta. Despite this weakening, the package adopted last week contains painful sanctions, including restrictions on another 36 entities in Russia’s energy sector, 46 shadow fleet vessels, 20 banks and two Russian ports, as well as a ban on providing Russian entities with services linked to LNG exports and restrictions on cryptocurrencies used to transfer funds out of Russia.

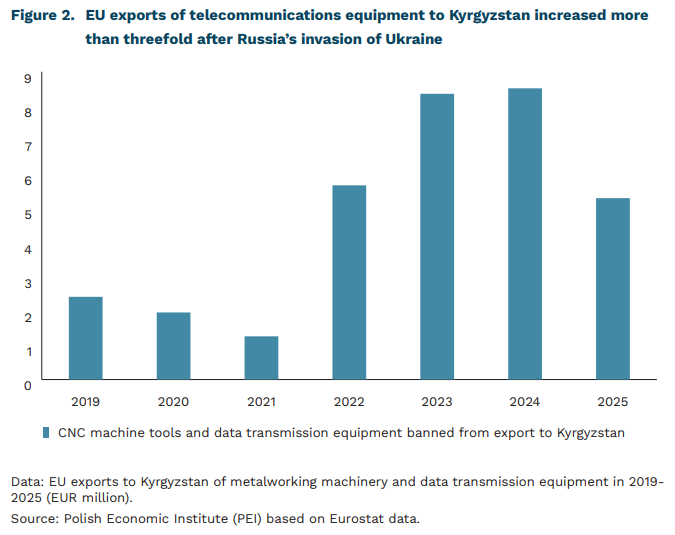

The 20th sanctions package also reflects the EU’s bolder approach towards countries that have helped circumvent sanctions or supply Russia’s arms industry. Many entities from third countries were included among those subject to restrictions, including entities from China, the United Arab Emirates, Uzbekistan, Kazakhstan, Belarus, Thailand and Turkey. In response to the sanctions on Chinese entities, Beijing added seven EU companies to its own restrictions list over their cooperation with Taiwan. For the first time, as part of its efforts to counter sanctions circumvention, the EU introduced a complete ban on exports of selected goods to a third country, prohibiting the sale of CNC machine tools and telecommunications equipment to Kyrgyzstan due to the large-scale re-export of these goods to Russia. According to the European Commission, EU exports to Kyrgyzstan of dual-use goods that could be used in Russian military production were almost eight times higher last year than before the invasion began, while Kyrgyzstan’s exports of these goods to Russia were 12 times higher. The goods covered by the latest sales ban account for only a portion of the goods already banned from export to Russia, but the data suggest that the mere announcement of their inclusion under sanctions may have already contributed to a decline in EU exports of these goods to Kyrgyzstan.

The loan to Ukraine and the adoption of the 20th sanctions package point to an evolution in Europe’s approach. To fill the gap left by the US withdrawal, the EU is taking a more active role in financing Ukraine’s military spending and is also adopting a more decisive approach to penalising entities from third countries that support the Russian economy. However, a more painful blow to the Russian economy would require a complete halt to purchases of Russian oil, as well as stronger restrictions on services linked to its export – steps that some member states are still not ready to take.

Jan Strzelecki

Most Polish companies are still not ready to make productive use of AI

only 23% of companies in the sectors with the greatest potential for AI implementation are using this technology

as many as 46% of companies have a very cautious approach to AI

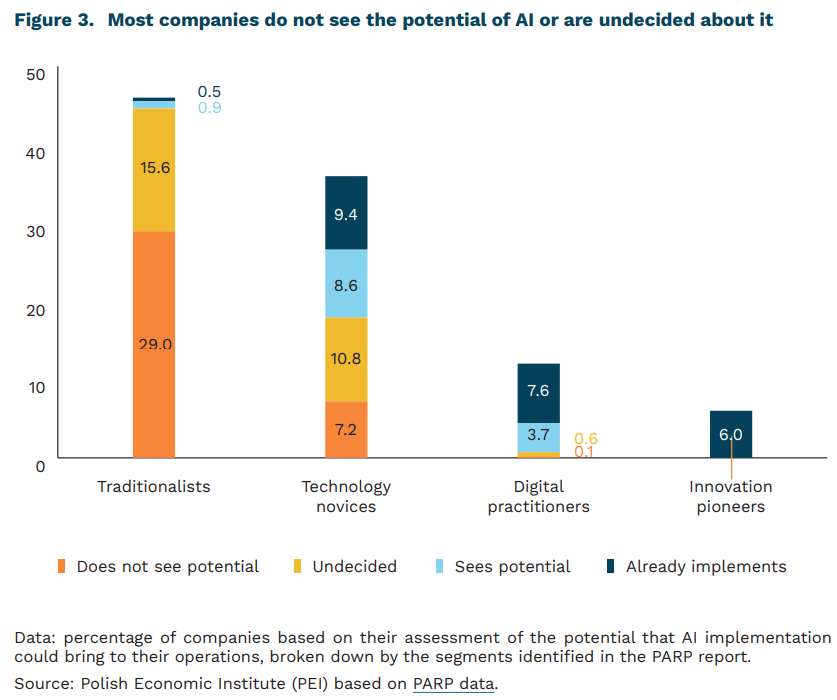

The majority of companies operating in Poland are still not ready to implement artificial intelligence (AI) solutions – recently published research findings from the Polish Agency for Enterprise Development (PARP) and the Jagiellonian University confirm existing data on the digitalisation of the Polish economy. Only 23% of the surveyed companies, representing 12 sectors with the theoretically greatest potential for AI implementation, use these technologies, whilst as many as 37% see no potential whatsoever for utilising this technology.

In the aforementioned research, conducted in the second half of last year, as many as 46% of companies are classified as ‘traditionalists’ – those who recognise the potential of AI in the context of their own operations to a limited extent, with a conservative approach to technology. In contrast, in a research conducted by the Ministry of Economic Development and Technology conducted a year and a half earlier, the group uninterested in digitalisation and failing to see its benefits stood at 38%.4 It can therefore be assumed that, despite market changes and the constant presence of the topic of AI in the media, the proportion of companies structurally uninterested in digitalisation remains relatively high and is not decreasing. The remaining groups are “technology novices” (36% of companies), “digital practitioners” (12%) and “innovation pioneers” (6%). The latter group consists primarily of companies from the energy, IT, finance and insurance sectors.

The report and the discussion accompanying its presentation clearly highlighted the theme of comprehensive business transformation that a company must undergo to fully exploit the potential of AI. Artificial intelligence, like other general-purpose technologies, requires a change in the way work is organised, in management methods and in the skills required. Meanwhile, among ‘traditionalists’, the majority of management staff do not keep up with technological trends (71%) and lack change management skills (74%). To a large extent, the transformation enabling the use of AI also involves investment in intangible assets, such as management skills, software and data (not only tools for collecting it, but above all skilful data management) and employee skills. Such investments, often treated in official statistics as mere costs, have a direct impact on the productivity of companies using AI, as confirmed by the EIB studies we have described.

Data presented by PARP point to a persistent technological divide among companies in Poland. Significant differences both between and within sectors, coupled with a substantial proportion of companies wary of technological change, may result in the emergence of strong leaders and a significant group of marginalised firms – losing market share, with increasingly less attractive products. This phenomenon is, in a sense, natural; however, what is cause for concern is the scale of the disparity (only 6% ‘pioneers’, 46% ‘traditionalists’) and the growing significance of competition from companies in other countries (digitalisation facilitates entry into foreign markets). In this context, the report’s recommendations regarding the need for comprehensive support from public authorities appear valid, although at the same time, changing the mindset of management will be a major challenge, as it goes beyond the traditional understanding of skills development or knowledge dissemination.

Ignacy Święcicki

The outlook for the German economy has deteriorated

0.5% GDP growth in 2026, according to the German ministry

2.7% inflation in 2026, according to the German ministry

0.3% m/m decline in German industrial production in February 2026

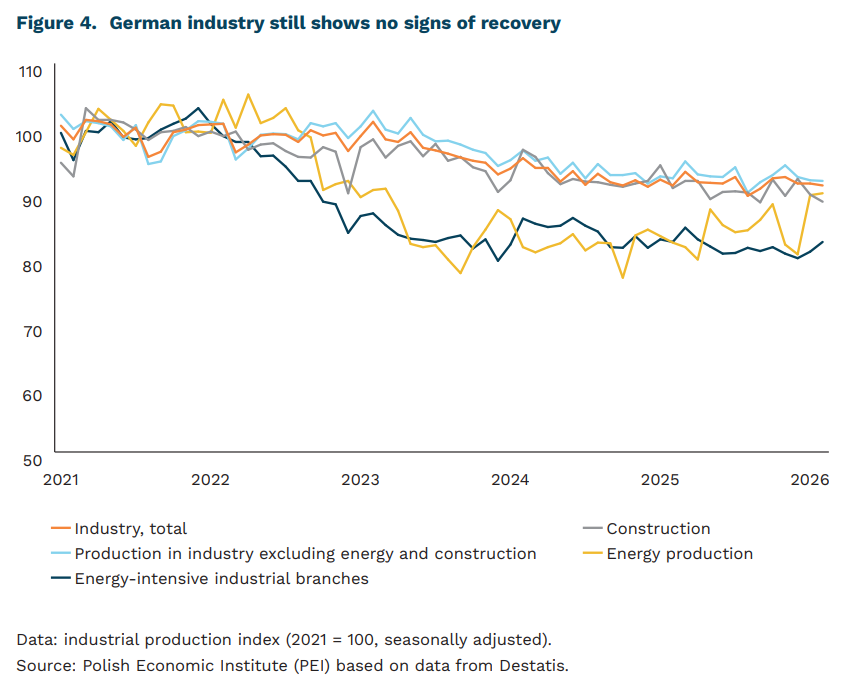

As a result of the escalation of the conflict in the Middle East, the economic outlook for Germany has deteriorated. The government has lowered its expected GDP growth to 0.5% in 2026 and 0.9% in 2027, down from 1.0% and 1.3%, respectively. The revision is driven primarily by a new energy shock. The war in Iran has pushed up oil and gas prices, and Germany, despite its energy transition, remains particularly vulnerable to energy costs. At the same time, the traditional engine of the German economy – industry – remains weak: industrial production in February 2026 fell by 0.3% month on month and by 0.4% in three-month terms. Although the value of industrial orders rose by 0.9% in February, this was a rebound after a very sharp 11.1% decline in January, and does not yet indicate a lasting improvement. The deterioration in business sentiment is also confirmed by the Ifo Business Climate Index, which fell to 84.4 points in April, reaching its lowest level since May 2020.

At the same time, the German economy remains under inflationary pressure, with forecasts pointing to a sustained elevated pace of price growth. Inflation is expected to reach 2.7% in 2026 and 2.8% in 2027, compared with 2.2% in 2025. In response to the price shock, governments around the world, including the German government, have begun using various forms of intervention. As shown by a World Bank analysis, as many as 202 social policy measures in 79 countries have been implemented or planned in response to rising energy prices, about half of which are subsidies, mainly energy-related. These include, among other things, fuel subsidies, limits on price increases, and price-stabilisation mechanisms. Germany is also using such tools, introducing two-month fuel tax relief and limiting price increases at petrol stations to once per day.

Germany’s greatest opportunity at present lies in increasing public and private investment, especially in infrastructure, energy, digitalisation, defence, and advanced technologies. The government is trying to stimulate the economy through higher spending and reforms, including changes to parts of the tax system, as well as reducing bureaucracy and simplifying investment procedures. However, the effects of these measures will only become visible in the coming years. Despite the current difficulties, Germany still has strong fundamentals: a developed industrial sector, a high level of technology, and a key role in the European Union economy. However, the current state of the economy shows that the country still faces the need for deeper modernisation.

Piotr Kamiński

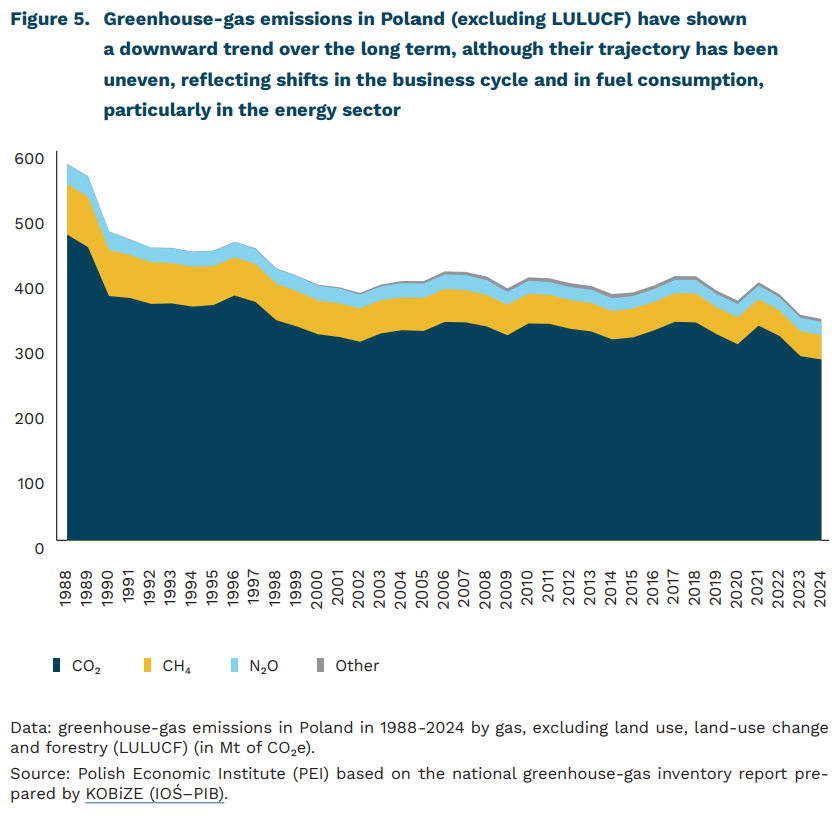

Lower carbon sequestration led to an increase in net greenhouse gas emissions in 2024

316.4 Mt of CO₂eq were Poland’s net greenhousegas emissions in 2024, marking a year-on-year increase of 2.8%

341.0 Mt of CO₂eq were Poland’s greenhouse-gas emissions excluding LULUCF in 2024, representing a year-on-year decline of 1.8%

According to the latest national inventory report prepared by KOBiZE (IOŚ-PIB), greenhouse-gas emissions in carbon dioxide equivalent (CO₂eq) in Poland in 2024 r. amounted to 316.4 Mt of CO₂e on a net basis in 2024, marking a year-on-year increase of 2.8%. This measure incorporates the balance of emissions and removals of CO₂ by forests and land use (LULUCF). At the same time, emissions excluding LULUCF declined slightly – to 341.0 Mt of CO₂eq (from 347.3 Mt in 2023) – pointing to a divergence in the direction of change between the two indicators. The structure of emissions excluding removals by forests and land has remained broadly unchanged over time: in 2024 carbon dioxide accounted for 81.8%, followed by methane (11.1%) and nitrous oxide (6.0%), with other gases playing a marginal role.

Compared with 1988, the first year such measurements were conducted in Poland, emissions in 2024 were 40.6% lower. The decline in greenhouse-gas emissions is consistent with a long-term trend of reducing fossil-fuel use in the energy and industrial sectors. This trend was initiated by the economic transition and has in recent years been reinforced by EU climate policy and the resulting energy transition, including the modernisation of generation capacity.

In 2024 around 77% of emissions (excluding LULUCF) originated from fuel combustion, primarily in solid-fuel-based power generation (1.A.1), road transport (1.A.3.b) and other sectors (1.A.4). In 2022-2024, reductions were driven mainly by lower fuel consumption in the energy sector and in households. In electricity and heat generation, hard-coal consumption fell by more than 30% over this period, lignite use by nearly 23%, while hard-coal consumption in households declined by around 26%.

The increase in net emissions alongside a decline in emissions excluding LULUCF points to a deterioration in the CO₂ removal balance of forests and land. This implies that their capacity to offset emissions was lower than a year earlier. This may reflect a weakening of the carbon sequestration capacity of forest ecosystems as well as changes in land use. It should be noted that part of the observed changes may reflect updates to estimation methods and data, rather than purely real-world developments.

Against the EU backdrop, Poland remains a relatively emissions-intensive economy. According to data from the European Environment Agencyper capita emissions in 2024 stood at 8.65 tonnes of CO₂eq, compared with 6.19 tonnes in the EU-27. An even wider gap is visible relative to GDP, with emissions in Poland reaching 511.7 tonnes of CO₂eq per million EUR (at 2015 prices), the highest level in the EU-27, against an EU average of 183.5. This suggests that despite the observed decline in emissions, their intensity in the Polish economy remains markedly above the EU average, reflecting the still high share of fossil fuels in the energy mix.

Krzysztof Krawiec

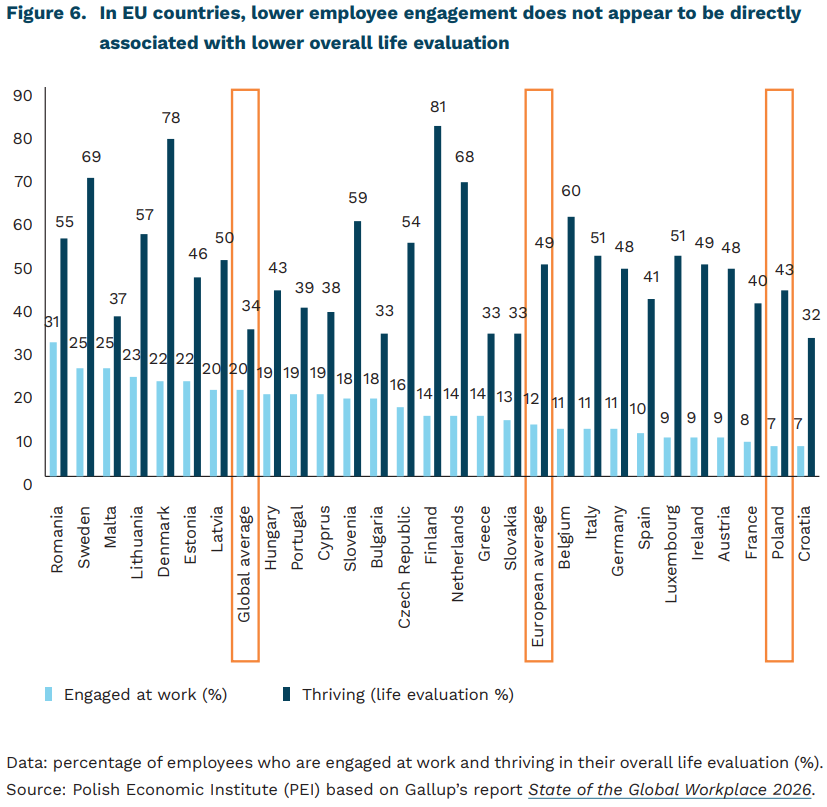

Employee engagement remains low due to poor management quality

7% of employees in Poland are engaged at work

59% of employees in Poland report that they are looking for, or monitoring opportunities for, a new job

43% of employees in Poland are classified as thriving based on their overall life evaluation

Employee engagement in Poland remains low relative to Europe and the global average. According to Gallup’s latest report, State of the Global Workplace 2026 only 7% of employees in Poland are classified as engaged at work. This places Poland among the lowest‑engagement countries in Europe, compared with a European average of 12% and a global average of 20%. At the same time, 43% of people in Poland are classified as thriving based on their overall life evaluation, compared with 49% in Europe and 34% globally. In addition, 57% of respondents in Poland believe it is a good time to find a job, while only 6% report feeling lonely. By comparison, 13% of people in Europe and 22% globally report experiences of loneliness.

The main factors differentiating employee engagement levels in Polish companies include internal communication and leadership quality. According to the Enpuls report Zaangażowanie 2025, based on continuous monitoring of employee experience across organizations employing a total of more than 100,000 employees, following a brief post‑pandemic improvement, Poland’s overall engagement index declined from 66% in 2024 to 63% in 2025. This decline affected all three core dimensions of engagement: sense of purpose at work, perceived impact on the organization, and opportunities for personal development. Enpuls reports that 38% of employees do not have access to all the information necessary to perform their work effectively, while 40% assess vertical communication within their organizations as insufficient. At the same time, 65% of employees declare awareness of their organization’s mission, representing a year‑on‑year decline of five percentage points. Notably, the share of employees who would not recommend their organization as a place to work exceeds the share of those who would.

Low levels of employee engagement are also associated with increased readiness to change jobs. According to the latest Randstad report nearly 60% of employees declare that they are looking for or considering new employment opportunities. The most frequently cited reasons include limited opportunities for professional development and dissatisfaction with management quality, both mentioned more often than dissatisfaction with pay levels.

The combination of a relatively high share of employees classified as thriving and one of the lowest levels of employee engagement in Europe suggests that Polish employees are adapting to organizational realities rather than forming strong emotional bonds with their employers. Critical assessments of management quality and internal communication appear to function primarily as mechanisms of distance rather than disengagement from work itself. This pattern points to a crisis in the quality of employee–organization relationships, rather than a broader crisis of employee well‑being as such.

Katarzyna Zybertowicz

AI can boost workforce participation among people with disabilities

One of the key issues analyzed by researchers studying the impact of AI on socio-economic reality is the effect of the widespread adoption of this technology on the labor market. Expectations of increased employee productivity and the gradual elimination of routine tasks – thus enhancing job satisfaction – are confronted with concerns about job losses in areas where work can be automated using AI. A relatively underexplored aspect of this discussion is the impact of AI on the situation of workers with disabilities; however, the latest research findings point to the potential of artificial intelligence to strengthen the competencies of this group of workers, help them remain in the labor market, and even increase their employment.

A recent study based on panel data from 25 developed countries, including Poland, covering the years 2010-2022 (i.e., the period before the deployment of generative artificial intelligence), examined both the linear (direct) and nonlinear effects of the diffusion of AI-based tools (measured somewhat imprecisely by the number of patent applications related to AI and industrial robots) on employment rates of people with disabilities. The direct effect of AI diffusion on the employment of people with disabilities proved to be negative and significantly more pronounced for men. However, the nonlinear relationships were more optimistic, indicating that at higher and more advanced levels of AI adoption, employment among people with disabilities increases.

The model used in the study showed that factors strengthening the positive impact of AI diffusion on the employment of people with disabilities include increased public spending on employment support programs, the education level of workers, as well as the quality of institutions and regulations, which were incorporated into the model at several detailed levels. In this context, regulations concerning fair employment practices are of particular importance.

The findings of another interesting study by researchers from Toronto illustrate a concrete example of AI use that enhances the competencies of workers with disabilities while also contributing to improved market performance for a company pursuing an inclusive hiring policy. The study was conducted among employees of a specialized online platform focused on meal deliveries, employing individuals with hearing impairments.

Before the implementation of an AI-based communication system, workers with disabilities performed significantly worse in processing orders and meeting delivery deadlines (they received negative customer ratings more often and took longer to complete tasks) than other employees. Supporting communication for hearing-impaired workers with AI tools that generate natural-sounding speech improved both the speed and quality of their work. Wage disparities between non-disabled and disabled employees also decreased, and the company’s revenues increased by 11%.

The authors of the study point out that, in this case, the widespread employment of people with disabilities contributed to a significant increase in productivity, making the investment in AI technology profitable without the need for external funding. In companies where people with disabilities make up only a small share of the workforce, such innovations may yield lower returns, meaning their implementation may require government subsidies. In the context of employing people with disabilities, such support may be particularly justified not only for social reasons, but also as a way to harness the potential of people with disabilities in the labor market amid shrinking human resources.

These and other studies point to a growing need for active involvement of public institutions in shaping the potential impact of AI on the labor market, particularly – though not exclusively – with regard to people with disabilities. Not only appropriate regulations are needed, but also support programs, especially those aimed at improving AI-related skills among individuals at risk of exclusion and at financing socially important and economically viable AI implementations.

Agnieszka Wincewicz-Price