Economic Weekly 22/2026, June 5, 2026

Published: 05/06/2026

Table of contents

Armenia, heading into elections, is now closer to the EU but still dependent on Russia

7.2% Armenia’s economic growth in 2025

48% share of EU exports to Armenia in 2025 made up of goods covered by the export ban to Russia

49% share of EAEU exports to Armenia in 2025 made up of gold and precious stones

Armenia’s parliamentary elections, scheduled for 7 June, will take place amid rapprochement with the EU and persistent polarisation following the loss of Nagorno-Karabakh. The government of Nikol Pashinyan offers peace with Azerbaijan, the opening of borders and trade diversification as a long-term development opportunity, while the opposition warns of losing access to the Russian market, cheaper energy and membership in the Eurasian Economic Union (EAEU). Moscow, too, has issued warnings ahead of the elections about the consequences of a pro-European course. At the recent EAEU summit, Vladimir Putin compared Armenia’s situation to Ukraine’s and threatened, among other things, with the loss of access to the free-trade area, preferential gas prices, investment and labour market. At the same time, the country has enjoyed uninterrupted GDP growth above 5% since 2021 and seeks to leverage the economic consequences of Russia’s invasion of Ukraine. Growth in recent years has been driven, among other things, by re-export earnings to Russia and the inflow of migrants.

Armenia remains tied to Russia institutionally, economically and militarily, but following the Karabakh war with Azerbaijan and Russia’s invasion of Ukraine it has begun a process of rapprochement with the EU. The EU-Armenia summit in Yerevan in May 2026, preceded by a meeting of the European Political Community, was intended to demonstrate that Brussels treats Armenia as an important element of its policy in the South Caucasus: deeper cooperation was announced in transport, energy, digitalisation, security and resilience to hybrid threats. Economic integration with the EU appears feasible primarily through the development of infrastructure connections, for which the EU intends to commit substantial financial support. The ongoing normalisation of relations between Yerevan and Baku could give greater importance to the trade corridor running through Armenia and bypassing Russia between China and the EU.

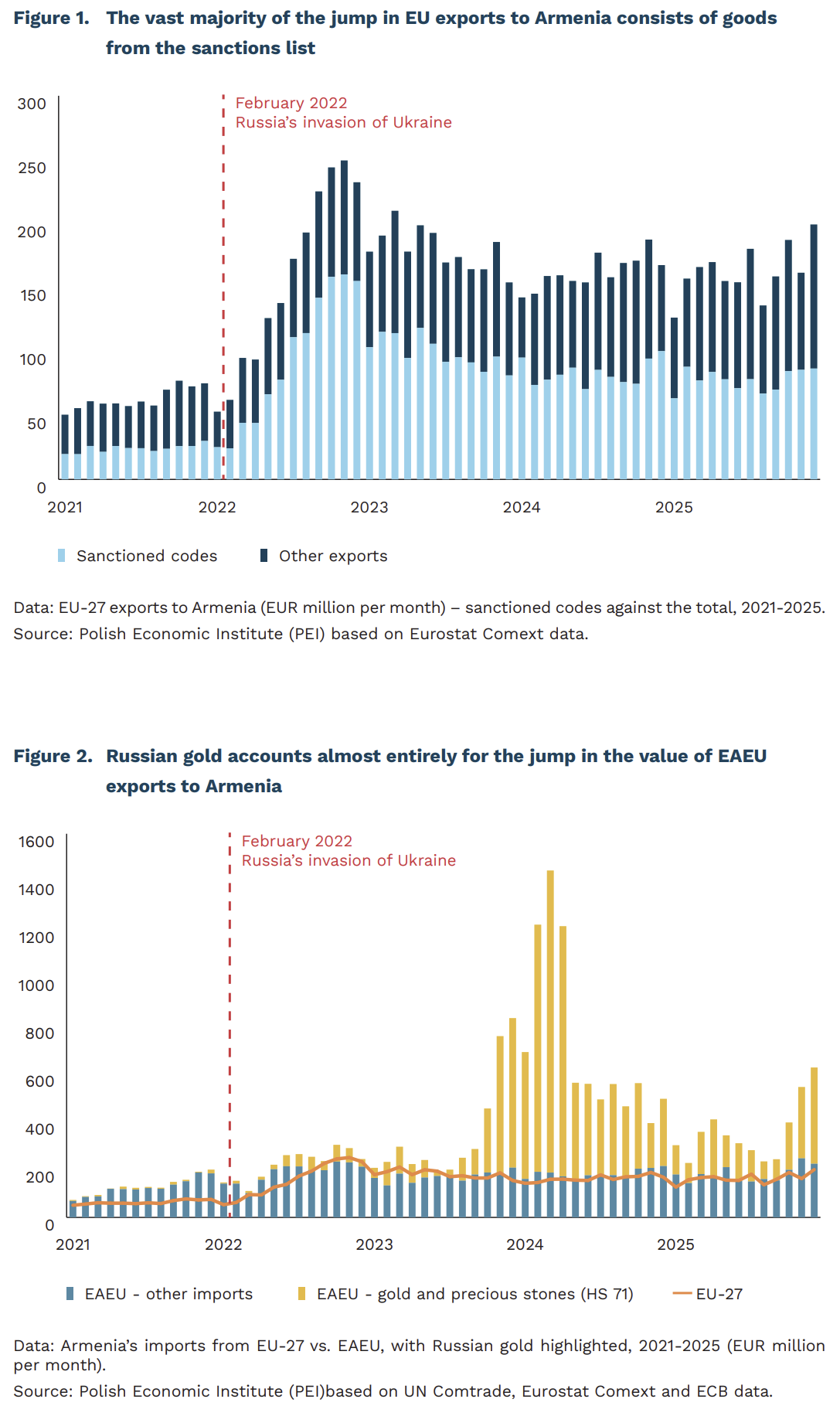

In recent years Armenia has benefited from the sanctions imposed on Russia. After February 2022, EU exports to Armenia shifted scale abruptly: the average monthly value increased nearly threefold – from approximately EUR 62 million before Russia’s invasion of Ukraine (January 2021 – January 2022) to approximately EUR 170 million after it (March 2022 – December 2025). In annual terms, this translates into growth from EUR 0.76 billion in 2021 to EUR 1.9-2.2 billion per year in 2022-2025. The vast majority of this jump consists of goods on the EU sanctions list, including semiconductors, CNC machine tools, bearings, drones and aircraft parts, optics and telecommunications electronics. Their average monthly export rose 3.8-fold (from approximately EUR 24 million to approximately EUR 91 million) and accounts for 62% of the total increase. The share of these categories in the trade structure rose from 38% in 2021 to 60% in 2022, but in 2023-2025 it gradually declined to 48%. The remaining portion of exports also rose – on average twofold, from approximately EUR 38 million to approximately EUR 79 million per month – but more moderately and with a clearly consumer-oriented profile. The largest contributions came from pharmaceuticals and medical equipment, food, confectionery and beverages, as well as clothing, footwear and cosmetics, consistent with a classic consumer boom driven by Armenia’s rapidly growing economy after 2022.

Another signal of sanctions circumvention – this time of export sanctions imposed on Russia – is the transit of Russian gold through Armenia. The spike in the value of Armenia’s imports from the EAEU visible in the data is almost entirely accounted for by this category: in March 2024, gold accounted for 87% of monthly imports from Russia (it should be emphasised that it is re-exported almost immediately, mainly to the United Arab Emirates and Hong Kong).

The EAEU’s trade dominance over the EU in trade with Armenia is shrinking, but dependencies remain significant. The EAEU and the Russian market remain more important for Armenian exporters of food, alcohol and industrial goods, as well as for labour migration channels. In turn, Armenia depends on Russia for imports of key commodities: gas, fuels and grain. Dependence on Russia creates room for Russian pressure. Moscow can obstruct re-exports, restrict imports of Armenian agricultural produce, manipulate gas prices and use the EAEU as an instrument of leverage. After the elections, Armenia’s challenge will be to implement EU requirements on curbing sanctions-circumventing trade – both the re-export of goods to Russia and the transit of Russian gold and diamonds to third countries. This may make it harder to sustain rapid growth and increase pressure from Russia.

Aleksandra Sojka, Jan Strzelecki

Global investment in natural gas is at its highest level in a decade

5% YoY growth in global energy-sector investment in 2026

the EU saved USD 63 billion in 2025 on fossil fuel imports thanks to investments in clean technologies made between 2015 and 2024

PLN 30 billion the total value of gas-fired power plant projects currently under construction in Poland

Despite the destabilizing impact of the conflict in the Middle East, the International Energy Agency (IEA) estimates that global investment in the energy sector will reach USD 3.4 trillion in 2026, representing a 5% year-on-year increase. Investment in clean technologies is expected to be almost twice as high (USD 2.2 trillion) as investment in the fossil fuel sector (coal, oil, and gas). Capital expenditure in the oil production and supply sector is projected to decline for the third consecutive year, falling below USD 500 billion in 2026, despite higher oil prices caused by disruptions in the Strait of Hormuz, which have boosted revenues for most producers.

A significant global trend is the rise in investment in natural gas production and supply, which is expected to reach USD 330 billion in 2026, the highest level in a decade. Current investments in gas extraction and gas infrastructure are primarily aimed at meeting domestic demand in countries with substantial gas reserves. However, a significant share also consists of export-oriented projects, particularly a new wave of investments in liquefied natural gas (LNG) exports, mainly in the United States and Qatar. This trend accelerated in 2025, when projects increasing LNG export capacity by more than 100 billion cubic meters per year were approved.

Global orders for new gas-fired power plants reached 130 GW in 2025, the highest level in 25 years. One of the main drivers of this growth was electricity demand from data centers in the United States. The same factor also accounted for nearly all orders for gas turbines intended for on-site power generation, whose total value reached USD 28 billion in 2025. Such strong demand from a single country is limiting turbine availability for projects planned in other parts of the world over the coming years. According to Bloomberg, gas-fired power plant projects with a combined value exceeding USD 400 billion, planned by 2030, are at risk of delays or cancellation due to insufficient production capacity among gas turbine manufacturers.

According to IEA estimates, investments in electrification and other clean technologies made in the European Union between 2015 and 2024 enabled EU countries to avoid importing fossil fuels worth a total of USD 63 billion in 2025. As a net energy importer, the EU saved USD 12 billion on coal, USD 34 billion on crude oil, and USD 17 billion on natural gas. The vast majority (90%) of avoided fossil fuel imports into the EU in 2025 can be attributed to investments in renewable energy (USD 29 billion in savings) and energy efficiency (USD 28 billion in savings).

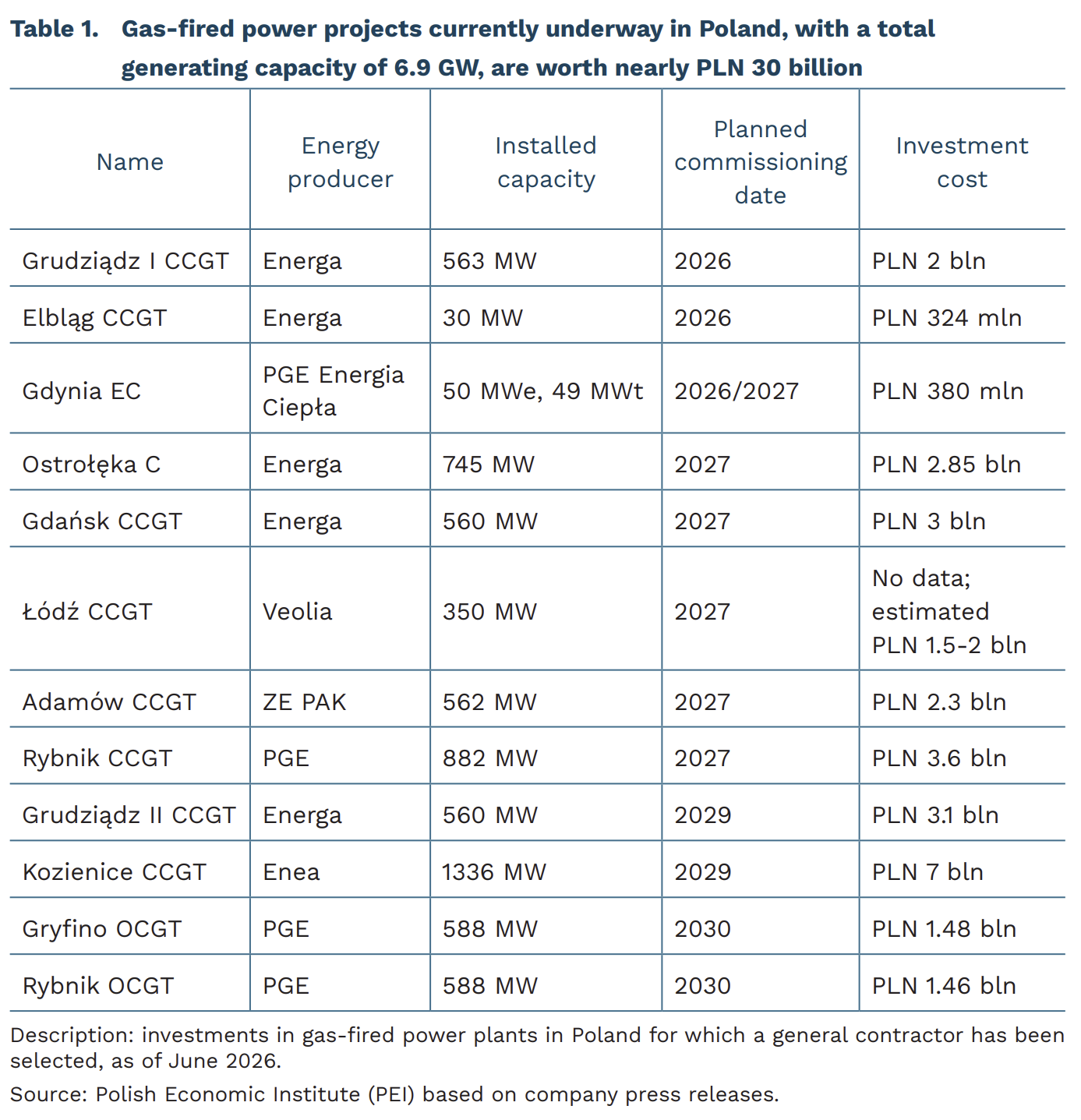

Poland is following the trend of growing demand for gas infrastructure. In the transformation of Poland’s energy system, natural gas is regarded as a transitional fuel that, over the next 10-15 years, is expected to replace coal-fired units, which are characterized by significantly higher emissions than gas-fired ones. The installed capacity of gas-fired power plants in the National Power System currently amounts to nearly 6 GW, with another 6.9 GW under construction and scheduled to come online. Although the expansion of gas-fired generation is necessary to fill the capacity gap left by the phase-out of coalfired plants, there is a risk of overinvestment in this type of infrastructure considering climate neutrality goals. It also increases dependence on fuel imports, predominantly from countries outside the EU.

Marianna Sobkiewicz

European Commission’s forecasts for Poland have withstood the test of the Middle East crisis

3.5% forecast GDP growth for Poland in 2026 (EC forecasts, autumn 2025 and spring 2026)

3.4% real year-on-year GDP growth in Q1 2026 (Statistics Poland flash estimate)

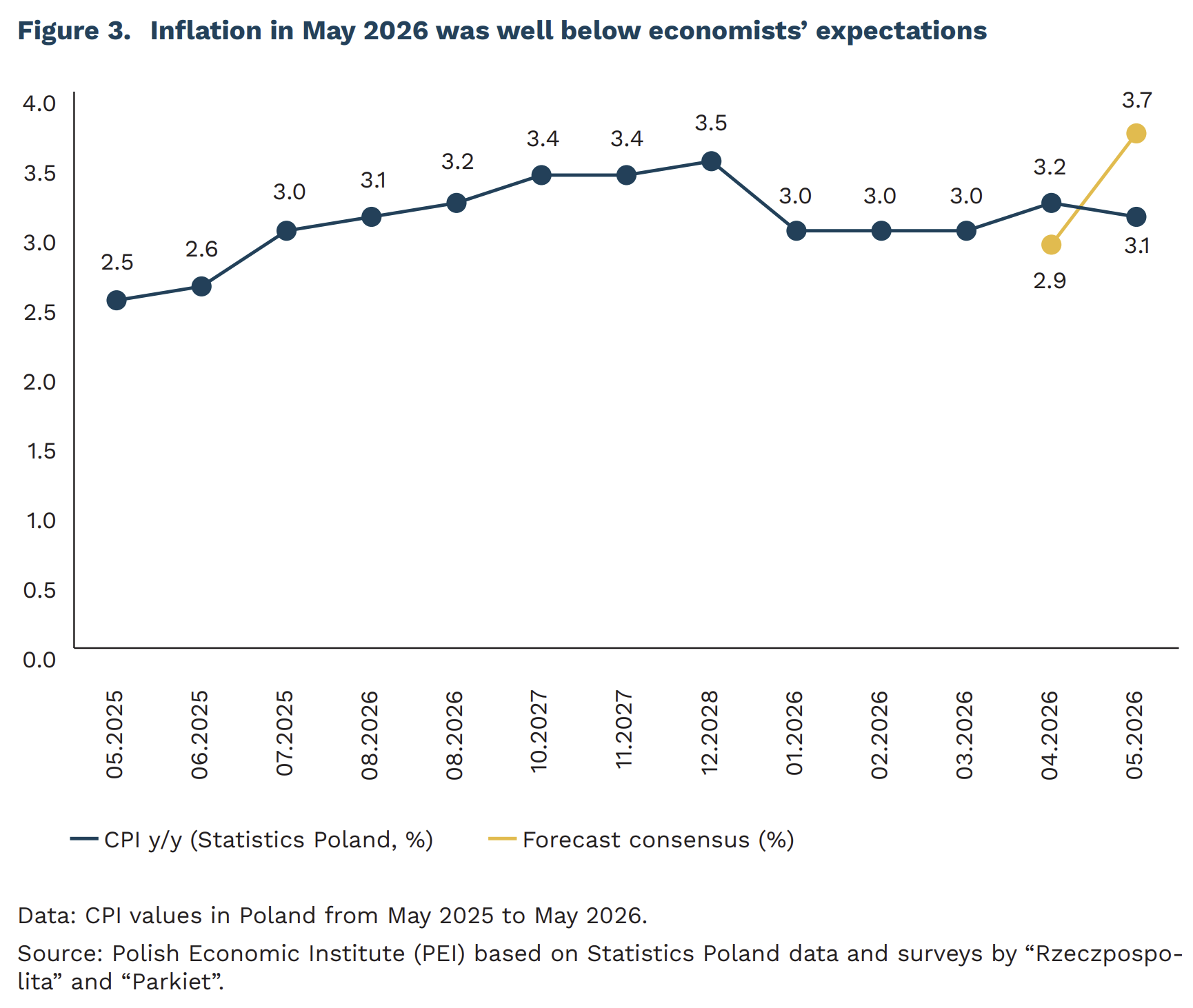

3.1% CPI inflation in May 2026 (consensus: 3.7%)

The European Commission’s spring forecast brought downward revisions to growth projections for almost all economies. Germany lost 0.6 percentage points from its growth forecast, Sweden 0.8 percentage points, and Romania as much as 1.0 percentage point. Poland was one of three EU countries whose forecast was not revised down. The Commission maintained its November 2025 forecast for Poland, projecting GDP growth of 3.5%, supported by resilient private consumption and large investments financed by EU funds.

The European Commission has solid grounds for maintaining its projections, as confirmed by macroeconomic data. The GDP estimate for Q1 2026 points to real year-on-year growth of 3.4%, in line with the pace forecast for the full year. Seasonally adjusted GDP increased by 0.5% quarter on quarter, confirming that the economy is maintaining a stable growth rate despite global turbulence. It is also worth noting that the IMF, despite its April revision to 3.3% from the 3.5% forecast in January, continues to have higher expectations for the Polish economy than it did in October 2025, when it projected growth of 3.1%.

Sustained growth is significantly supported by the stabilization and absorption of funds from the Recovery and Resilience Plan, as highlighted by the European Commission. The Commission points to record absorption of RRF funds in the final year of the plan’s implementation as a key factor sustaining Poland’s investment momentum. Higher public investment co-financed by EU funds is expected to offset the anticipated slowdown in private consumption in 2026, keeping overall growth on a solid footing.

The optimistic picture of the Polish economy is confirmed by the May inflation reading, which surprised the market to the downside. Statistics Poland reported that CPI inflation in May 2026 stood at 3.1% year on year, compared with 3.2% in April and a market consensus of 3.7%. The main source of the surprise was food, which fell by as much as 1.0% month on month, despite the seasonal tendency for prices to rise in May. Core inflation was also lower than forecast, estimated at around 3.0% year on year, suggesting that the fuel shock has not yet translated into broader price pressure.

The scale of May’s inflation surprise is particularly telling in the geopolitical context that was expected to push prices higher. The closure of the Strait of Hormuz in early March, following the conflict in the Middle East, triggered a sharp rise in oil prices and was the main argument for an acceleration of inflation in Poland. Meanwhile, the May reading shows that the Polish economy proved surprisingly resilient to this energy shock. The government’s rapid fiscal response also played an important role: a reduction in VAT and excise duty on fuels, along with a daily price cap introduced at the end of March, which the European Commission cites as a factor easing inflationary pressure. Reports of possible progress in US-Iran talks have contributed to oil price declines in recent days, reducing inflation risks for the Polish economy in the coming months.

Jakub Kubiczek

Despite demographic challenges, local authorities are not scaling back their investments

81% of local government officials consider demographic changes to be a major or very major challenge to development

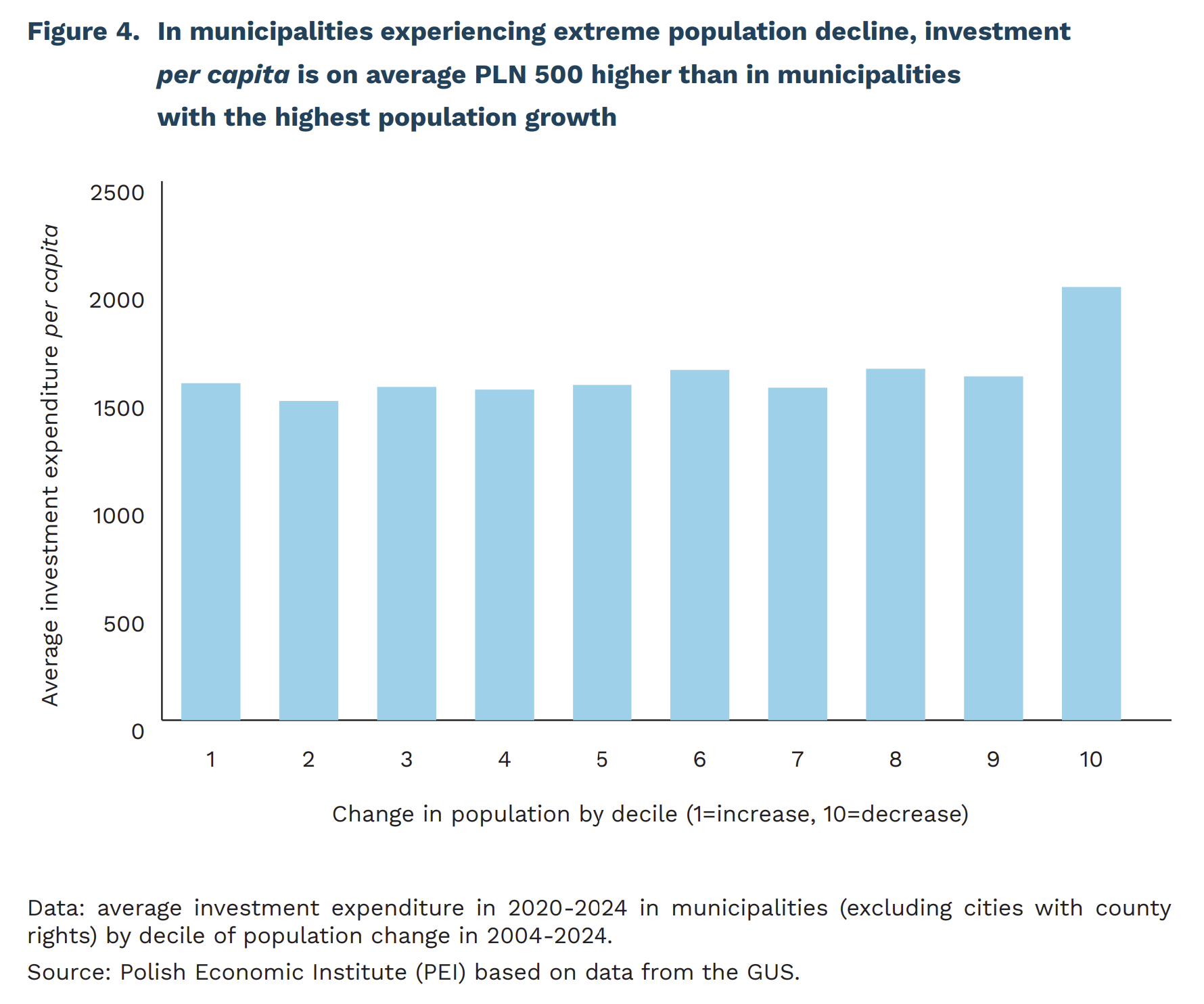

PLN 500 more on investment per capita spent by municipalities experiencing extreme depopulation than those with growing populations.

67% of municipalities, despite shrinking populations, cite road infrastructure as a priority in local spending

The consequences of demographic change are now one of the most significant challenges facing local authorities. Research by the Foundation for the Development of Local Democracy (FRDL) in spring 2026 shows that 81% of local government officials view depopulation and an ageing population as a key strategic issue. Nevertheless, they most often regard infrastructure as the policy area requiring the largest expenditure from the local budget. The current landscape of local governance in Poland is defined by the gap between the recognition of demographic challenges and the policy responses adopted by local governments.

Despite demographic pressures, spending priorities continue to follow the established pattern of investing in infrastructure. According to the FRDL report, as many as 67.0% of local authority officials identified road infrastructure as the area requiring the most urgent support. Water supply and sewerage (48.7%) and education and pre-school care (41.5%) followed. In the face of a systematic exodus of young people and shrinking school cohorts, such a logic seems inconsistent. Whilst expenditure on maintaining existing infrastructure is, to some extent, a necessity regardless of demographic conditions, expanding the road network or establishing nurseries in depopulating areas runs contrary to the declining number of their future users. The explanation for this phenomenon, however, lies in the field of political economy. A common feature of these three priorities is their high visibility. A lack of action regarding roads or the water supply network is immediately noticed by residents. Conversely, successful projects provide tangible and easily communicated evidence of a mayor’s effectiveness ahead of elections.

The results of PIE analyses based on econometric models confirm that depopulation does not lead to a proportional reduction in investment expenditure. The relationship between the number of residents and investment expenditure is asymmetrical. A rapid increase in per capita expenditure is evident in the group of smaller, depopulating local authorities. This results from several mechanisms. Water and sewerage networks or roads cannot be easily scaled back as residents leave, and the cost of maintaining them is spread across a smaller number of users. Another key factor driving this expenditure is the availability of external grants, including targeted national subsidies and EU funds, as well as the political and budgetary cycle – investment expenditure rises in pre-election and election years.

Although high levels of investment activity may improve living conditions, maintaining them under conditions of persistent depopulation also creates long-term risks. The costs of maintaining infrastructure investments over a 10- to 15-year period could place a significant burden on the budgets of depopulating municipalities

Beyond the infrastructure investments themselves, mitigating the long-term effects of depopulation is becoming a key challenge for local authorities. This requires careful consideration of the reorganisation of public service provision, adjusting the number and location of schools, nurseries and other public institutions to the changing population, as well as the development of inter-municipal cooperation. It may also mean moving away from the assumption that all municipalities can carry out the same range of public tasks.

Agata Mróz

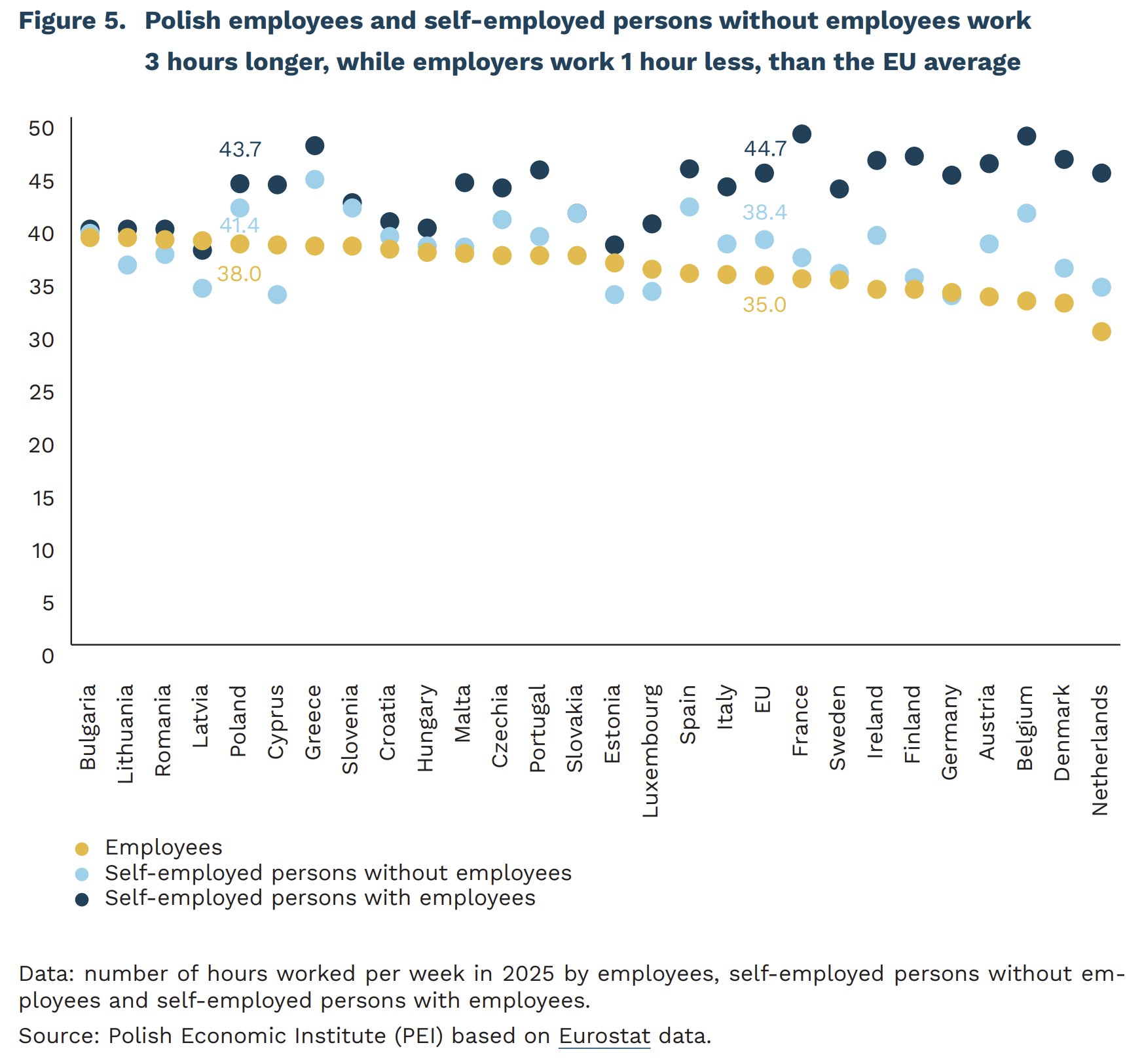

Poles are among those who work the longest in the EU

38 hours per week (average) work employees in Poland (EU average: 35 hours)

6.2% of Poles work part-time (EU average: 17.7%)

1 hour less than the EU average work in Poland self-employed persons without employees

Self-employed persons usually work more hours per week than employees. In Poland in 2025, self-employed persons without employees worked an average of 41.4 hours per week, while self-employed persons with employees worked as much as 43.7 hours. For the self-employed without employees, the EU average is 38.4 hours. The shortest hours among the self-employed without employees were recorded in Germany (33.1 hours), Estonia (33.2 hours), Cyprus (33.2 hours) and Luxembourg (33.5 hours), while the longest were in Greece (44.1 hours). Business owners who employ staff devote even more time to work – an average of 44.7 hours per week in the EU. In this group, entrepreneurs work the least in Latvia (37.4 hours) and Estonia (37.9 hours), and the most in France (48.4 hours), Belgium (48.2 hours) and Greece (47.3 hours). The longer working hours of entrepreneurs, especially those who employ staff, are probably due to the need to combine the roles of owner and manager.

In 2025, employees in Poland worked an average of 38 hours per week, which was the fifth-highest result in the EU – after Lithuania (38.6 hours), Bulgaria (38.6 hours), Romania (38.4 hours) and Latvia (38.3 hours). The EU average was 35 hours. The shortest working hours were recorded in the Netherlands (29.7 hours), Denmark (32.4 hours), Belgium (32.6 hours), Austria (33.0 hours) and Germany (33.4 hours). The difference between the countries with the shortest and the longest working hours for employees was 5.2 hours. Poles worked 3 hours longer than the EU average. The largest differences in working time usually occur between employees and entrepreneurs who employ staff. This may result from the fact that some self-employed persons without employees provide services exclusively to a single client. In practice, this implies a form of work similar to regular employment, referred to as “bogus self-employment”, which can be both a choice motivated by higher income and a solution imposed by an employer. The scale of bogus self-employment may also help explain why in Poland the working time of the self-employed without employees is shorter than the EU average.

In countries with a higher share of part-time work, weekly working time is clearly shorter. In Poland, only 6.2% of employees work part-time, which is among the lower figures in the EU. By comparison, across the EU this share averages 17.7%. The highest shares of part-time workers are found in the Netherlands (42.7%), Austria (30.1%) and Germany (29.4%), and the lowest in Bulgaria (1.7%). The difference in working time between fulltime and part-time employees was 1.2 hours in Poland, while in the Netherlands – where part-time work is most popular – it was as much as 6.6 hours. Part-time work not only supports a better work-life balance, but also enables labour-market participation for people who, for family or health reasons, cannot work full-time.

Longer weekly working hours do not necessarily lead to higher productivity. In the EU, the highest productivity is achieved, among others, by Luxembourg, Belgium, Denmark, the Netherlands and France – countries where employees’ working hours are among the shortest. Extended working time may be associated with excessive workload, which in turn can contribute to lower productivity. At the same time, these are countries where entrepreneurs who employ staff (managers) work the longest, which may indicate better management quality. In Poland, relatively lower productivity may also result from the structure of the economy – namely, the high share of construction and agriculture in GDP. These are sectors that require long working hours while also being characterised by lower levels of automation and more limited use of modern technologies.

Anna Szymańska

The housing crisis affecting young Europeans continues to deepen

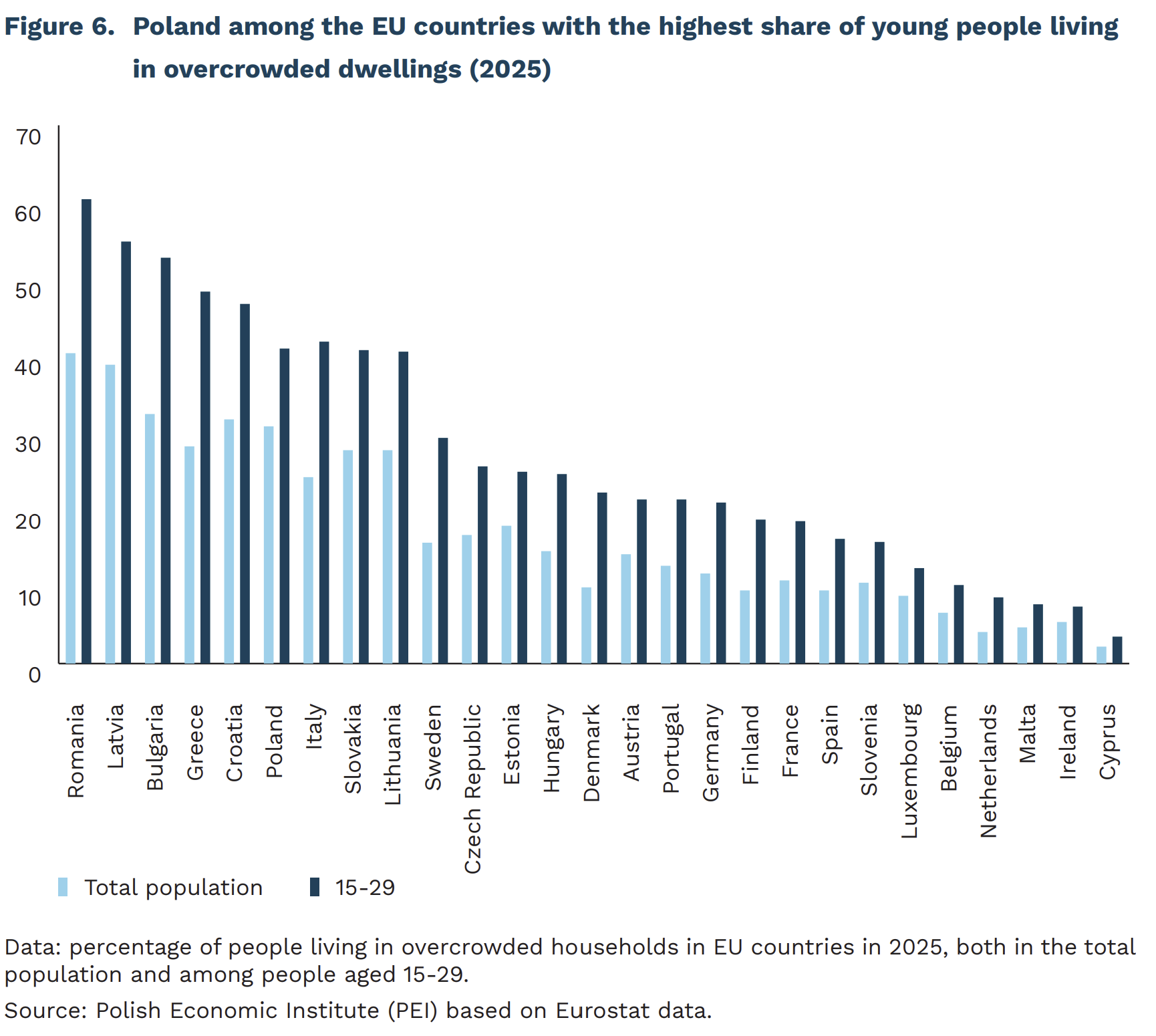

41% of people aged 15-29 in Poland were living in overcrowded households in 2025

3.9% of people aged 15-29 in Poland lived in households experiencing a housing cost overburden, with housing expenditures exceeding 40% of disposable household income in 2025

At the end of the previous quarter, the European Commission published a report examining the housing situation of young people in the EU and the public policy instruments used across Member States to improve housing affordability and access. The report highlights that the housing crisis – described by the President of the European Commission as a social crisis – has a particularly severe impact on young people. It hampers, and in some cases prevents, their ability to live independently, which in turn delays major life decisions such as starting a family.

In 2024, 27% of people aged 15-29 in the EU lived in overcrowded households, compared with 17% of the total population. This share rises to 42% This share rises to 42% among young people at risk of poverty. In the same year, more than 10% of young Europeans lived in households where housing costs exceeded 40% of their income, even though housing expenditure is generally considered affordable when it does not exceed 30% of income. The rate of housing exclusion – defined as the share of the population living in overcrowded dwellings that also fail to meet basic housing standards (e.g., lacking a toilet, shower, or bathtub, having a leaking roof, or inadequate lighting) – stood at 7% among young people (14% among young people at risk of poverty), compared with 4% in the overall population.

According to an OECD report, young people face significant barriers to obtaining mortgage loans due to limited accumulated wealth and the prevalence of unstable employment arrangements.

Poland ranks among the worst-performing EU countries in terms of housing overcrowding. In 2025, 31% of the total population lived in dwellings with insufficient living space, placing Poland fifth highest in the EU. Among young people aged 15-29, the overcrowding rate reached 41%, ranking Poland sixth highest in the EU. Only Romania, Latvia, Bulgaria, Greece, and Croatia recorded worse outcomes.

At the same time, Poland performs considerably better in terms of housing cost overburden, which includes mortgage payments, rent, and housing maintenance expenses. In 2025, 4.1% of the total population and 3.9% of young people aged 15-29 lived in households where housing costs exceeded 40% of household income. In most Western European countries, these rates are higher, particularly among young people (France: 7.4%, Germany: 14.3%, Denmark: 26.9%). These differences may be explained by variations in housing tenure structures – young people in Western Europe are more likely to live in rented accommodation – as well as by the higher levels of overcrowding and the longer period that young people in Poland tend to remain in the parental home.

Most EU countries have measures in place to improve access to housing, including housing allowances, rent subsidies, social housing, tax incentives, and support for obtaining mortgage financing. However, the authors of the report emphasize the need for housing support programmes specifically tailored to the needs of young people. Such targeted schemes currently exist only in Belgium, Ireland, and Turkey.

Among the initiatives highlighted in the report are a Portuguese programme supporting students from low-income families who have moved away from their parental homes for educational purposes, and a Romanian programme that provides incentives for young people to remain in or return to rural areas.

The report also praises the educational component of Poland’s former social housing programme, “Housing, Work, Community” (“Mieszkanie, Praca, Społeczność”). In addition to housing support, young beneficiaries received assistance with job searches, financial and economic literacy training, and mentoring

Agnieszka Wincewicz-Price

A place-based approach makes industrial policy more effective

Embedding public interventions locally can increase the effectiveness of investments, strengthen democratic legitimacy, and distribute the benefits of development more equitably. This can be illustrated by the example of industrial policy, which today encompasses many overlapping objectives – technological autonomy, national security, and climate transition. In a new publication titled Place-Based Industrial Policy, the authors point out that such a territorially rooted approach to industrial policy can yield significantly better results than purely top-down decisions made at the central level.

The transformation of the steel industry in Port Talbot is an example of the lack of a place-based industrial policy. The steelworks provided well-paid, stable jobs even to those without high qualifications – wages were 36% percent higher than the regional average, despite the city’s educational attainment being lower than the national average. At the same time, the steel produced was losing its competitiveness – mainly due to overproduction in China and high energy costs. However, government interventions took the form of reactive crisis management, without a long-term strategy for the region. This process was characterized by centralized decision-making and the marginalization of Welsh authorities and trade unions. The result of this transformation was a weakening of the local labour market and a reduction in the country’s steel production capacity, which is crucial from the perspective of strategic autonomy. Approximately 2,500 jobs were lost, and another 2,800 indirect jobs are at risk. Retraining programs did not meet the needs of the regional economy, while new jobs in the green industry are expected to be created gradually, reaching full scale only around 2050. This has reinforced a sense of abandonment and injustice within the local community.

A successful example is the multi-sectoral, place-based industrial policy implemented in Pori, Finland. Today, the city is a cluster for robotics, green technologies, and, increasingly, artificial intelligence applications in industry. In response to the crisis of the 1990s, the city chose not to build entirely new industries, but rather to develop the engineering and technical capabilities already present in Pori, focusing on automation and robotics. In 1992, a technical university strongly focused on collaboration with local industry was established. At the same time, other specializations were also developed. Key factors included: the proactive exercise of municipal authority, the strategic alignment of local actions with national and EU priorities, and coordination between the administration, universities, and business. Post-industrial regions often experience deep economic marginalization. Against this background, Pori’s ability to maintain a relatively stable position in the national economy – despite a decline in its share of national gross value added from 2.24% in 2000 to 1.97% in 2023 – can be considered a significant success of this strategy.

The two case studies described above show that effective industrial policy must, above all, be tailored to local conditions. In the Polish context, this perspective is particularly important in industrial, post-industrial, and coal-mining regions. It is crucial not only to offset the costs of transitioning away from old sectors but also to build new regional specializations based on existing competencies, traditions, resources, and value chains. This requires not only proactive engagement by local authorities and institutions but also openness on the part of the central administration to the co-design of policy measures. Investments in quality of life are also a key element of this approach. The ability of regions to attract and retain talent is now becoming one of the prerequisites for the success of industrial policy.

Filip Leśniewicz