Economic Weekly 13/2026, April 3, 2026

Published: 03/04/2026

Table of contents

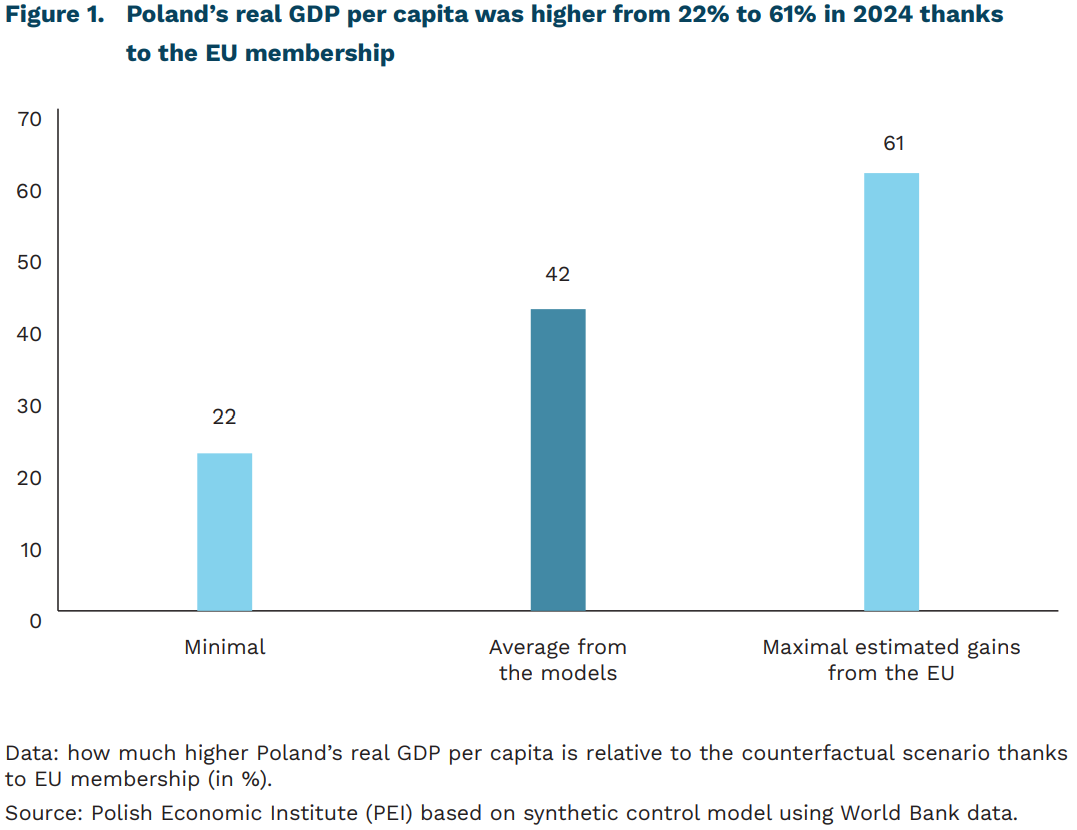

Poland gained 42% in GDP per capita from EU membership

around 42% higher is Poland’s real GDP per capita thanks to joining the EU

from 22% to 61% of GDP this is the range of our estimated gains from accession across 396 econometric models

Accession to the European Union significantly and permanently increased Poland’s prosperity. We used the synthetic control econometric method to estimate the benefits. By 2024 Poland had gained around 42% in GDP per capita as a result of EU membership relative to a counterfactual scenario. In other words, without accession to the EU, Poland’s real GDP per capita would currently be about 30% lower, roughly at its 2015 level. These gains stem largely from the benefits of joining the European single market, which facilitated trade, international investment, and improvements in institutional quality. We discussed these mechanisms in greater detail in the report The Great Enlargement: 20 Years of Central Europe’s EU Membership. Compared with those earlier calculations, here we use real data in constant U.S. dollars rather than purchasing power parity, as this better captures Poland’s international economic strength. Nevertheless, calculations based on PPP suggest similar gains from accession.

The synthetic control method involves constructing a counterfactual Poland composed of a group of countries (hereafter: donors [1]) that, in the pre-accession period, were at a similar stage of development and shared similar economic characteristics (hereafter: explanatory variables [2]). For this study, we selected 22 countries forming a pool of potential donors that are not and have never been members of the European Union. We then trace the development path of this counterfactual Poland through 2024 and compare it with the actual path of Poland’s real GDP per capita. The difference between the two trajectories represents the benefits resulting from the EU accession.

Estimates are robust to changes in specification. For the purposes of this analysis, we estimated 396 models incorporating different combinations of country groups and excluding selected explanatory variables. In every scenario, Poland clearly benefited from accession to the EU. The estimated gain in 2024 ranges from 22% in the most conservative estimate to 61% in the most optimistic one, with an average of around 42% of real GDP per capita. This means that our estimate of the gains from joining the EU is not statistical noise resulting from the inclusion of a particular variable or from the economic failure of a single donor country, but rather a systematic effect.

Models also pass the placebo test. This involves performing analogous calculations in each model for the donor countries used in it. We then check whether the results achieved by those countries relative to their own “hypothetical” counterparts were as impressive as in Poland’s case. In the ten years following EU accession, more than 80% of the countries we examined were unable to achieve a comparable result. This share increased further over the past five years, indicating that Poland continues to benefit from joining the European single market, for example through growth in trade and the inflow of foreign investment. As a result of the energy crisis in 2023, these potential gains diminished, although in 2024 they once again reached 42%.

[1] Argentina, Australia, Brazil, Belarus, Canada, Switzerland, Chile, Algeria, Indonesia, Israel, Japan, South Korea, Morocco, Mexico, Malaysia, New Zealand, the Philippines, Russia, Serbia, Turkey, Ukraine, and Uruguay.

[2] We use the shares of agriculture and industry in value added, the share of the working-age population, population growth, the share of people with secondary education, the share of investment in GDP, and additionally the distance from Poland.

Marcin Klucznik, Marek Wąsiński

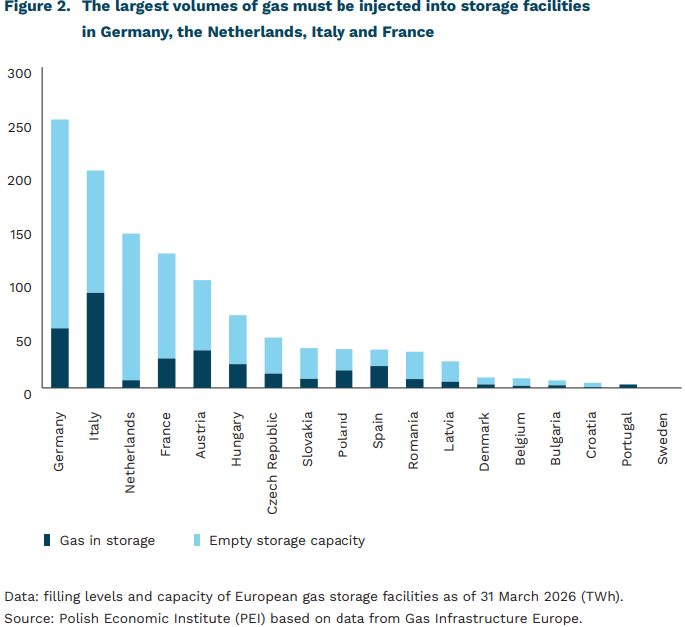

EU gas storage facilities are only 28% full

320 TWh of natural gas is currently held in European storage facilities, after a cold spell in January and February has led to a rapid decline in gas stocks. This is the lowest level since April 2022

90% of total capacity is the EU target for filling the national gas storage facilities before the next winter, although following changes in 2025, Member States may reduce this figure by 10-15 percentage points

Natural gas prices (TTF) in Europe have doubled since the beginning of January due to the harsh winter and then the war in the Persian Gulf

Low temperatures in January and February led to a rapid drawdown of gas from European storage facilities. According to data from Gas Infrastructure Europe, in January 2026, gas levels fell by as much as 240 TWh – since 2011, deeper monthly declines have only been recorded in January 2017 and 2021. However, a warm March brought some relief. In Poland, the impact of the winter was slightly less pronounced due to the smaller role of natural gas in district heating, domestic heating and electricity generation. Our storage facilities are currently around 45% full.

The current total capacity of EU gas storage facilities is 1,143 TWh. During the winter, these facilities meet 25-30% of Europe’s natural gas demand (the remainder is covered by current production and imports). The largest storage facilities are in Germany (251 TWh), Italy (203 TWh) and the Netherlands (144 TWh). Among neighbouring countries, Ukraine has a large storage facility (319 TWh).

As a challenging winter approached, European gas storage facilities were at their lowest levels since 2021. Since Russia’s invasion of Ukraine in February 2022, the European Union has paid particular attention to securing gas supplies ahead of the heating season. By 1 November 2022, Member States were required to reach at least 80% of their national storage capacity, whilst in subsequent years the target was 90%. Between 2022 and 2024, storage levels on 1 November reached 95-99%. In 2025, a decision was made to extend this regulation, albeit with some added flexibility. The filling target may be achieved between 1 October and 1 December. In the event of difficult market conditions, Member States may reduce the target by 10 percentage points (and a further 5 percentage points by means of a delegated act of the European Commission). This flexibility was intended to reduce the costs of filling storage facilities – mandatory purchases within a strictly defined timeframe resulted in higher prices. As a result of these changes, storage levels at the beginning of November 2025 reached only 83%.

In March, gas prices in Europe occasionally reached their highest levels since the start of 2023, although prices have since fallen. Replenishing depleted gas storage facilities ahead of the next heating season was already identified as a challenge even before the US and Israeli attack on Iran. Since the outbreak of the war, the situation has deteriorated significantly. Gas prices (TTF index) have risen since late February, from €31 to €50/MWh, reaching as high as €64/MWh on 19 March. Some LNG supplies destined for Europe have already been redirected to even more expensive Asian markets, which are directly threatened by shortages stemming from reduced Middle Eastern exports. Further price rises cannot be ruled out should the conflict drag on, or should there be further attacks on extraction infrastructure or LNG terminals, although prices have fallen in recent days.

Summer storage filling could be the most expensive since 2022. In response to rising prices, the European Commission has called on Member States to make use of the permissible flexibility and aim to fill storage facilities to 80% capacity. This approach is intended to prevent a build-up of demand and further cost increases. Even at a price of €50/MWh, the cost of the gas needed to fill storage facilities from 320 to 914 TWh would amount to €29.7 billion (although the actual cost will also be influenced by long-term contracts, additional transport costs and infrastructure costs).

Michał Smoleń

The share of Poles who cannot meet their material and social needs is declining

2% was the rate of severe material and social deprivation in Poland in 2025

0.7% was the deprivation rate in metropolitan areas in 2025

24.4% of people reported being unable to afford a one-week holiday for all household members in 2025

According to data published earlier this week by Statistics Poland, in 2025 2% of people living in Poland reported being unable, for financial reasons, to satisfy at least 7 out of 13 material and social needs. This share reflects the so-called severe deprivation rate and is estimated for people living in private households (collective living facilities are excluded from the study). Over the past decade, this indicator has declined significantly – from 7.8% in 2015 to 2.6% in 2020. During the pandemic it increased slightly, reaching 3% in 2023, but data from the last two years indicate a return to a downward trend (2.3% in 2024).

The thirteen needs analysed in the study cover five categories: physiological (ability to consume meat or fish every other day and adequate home heating), financial security (paying bills on time and ability to cover unexpected expenses), material (replacing worn-out furniture and clothing, access to a car and the internet), social (ability to regularly spend small amounts on personal needs and to meet friends or family), and leisure (ability to afford a holiday for all household members at least once a year and to regularly participate in active leisure activities).

The greatest improvement in Poles’ ability to finance basic needs over the past decade has been in access to a one-week annual holiday: in 2015, as many as 44% of people could not afford it, compared with 24.4% in 2025. There was also a significant decline in the share of people unable to cover unexpected expenses – from 42.3% in 2015 to 22% in 2025.

A territorial breakdown shows that the lowest deprivation rate is observed in metropolitan areas (cities with over 500,000 inhabitants) – 0.7%, while the highest is found in small towns (below 20,000 inhabitants) and densely populated rural areas outside agglomerations – 2.6% and 2.5% respectively. This is directly linked to income differences between large cities and smaller localities. In the largest cities, average annual disposable income in 2025 was estimated at PLN 86.2 thousand, compared with just under PLN 64 thousand in small towns and PLN 57.5 thousand in rural areas.

Despite income differences, the level of satisfaction of basic physiological needs (food, heating) and material needs (timely bill payments) is similar in urban and rural areas. The largest differences are observed in leisure spending: 31.1% of rural residents, compared with 20% of urban residents, could not afford a holiday for all household members.

It is also worth noting that Poland ranks among the EU countries with the lowest deprivation rates. According to Eurostat data, in 2024 only Slovenia (1.8%) and Croatia (2%) recorded lower rates, while the highest (double-digit) levels were observed in Romania (17.2%), Bulgaria (16.6%), and Greece (14%).

Agnieszka Wincewicz-Price

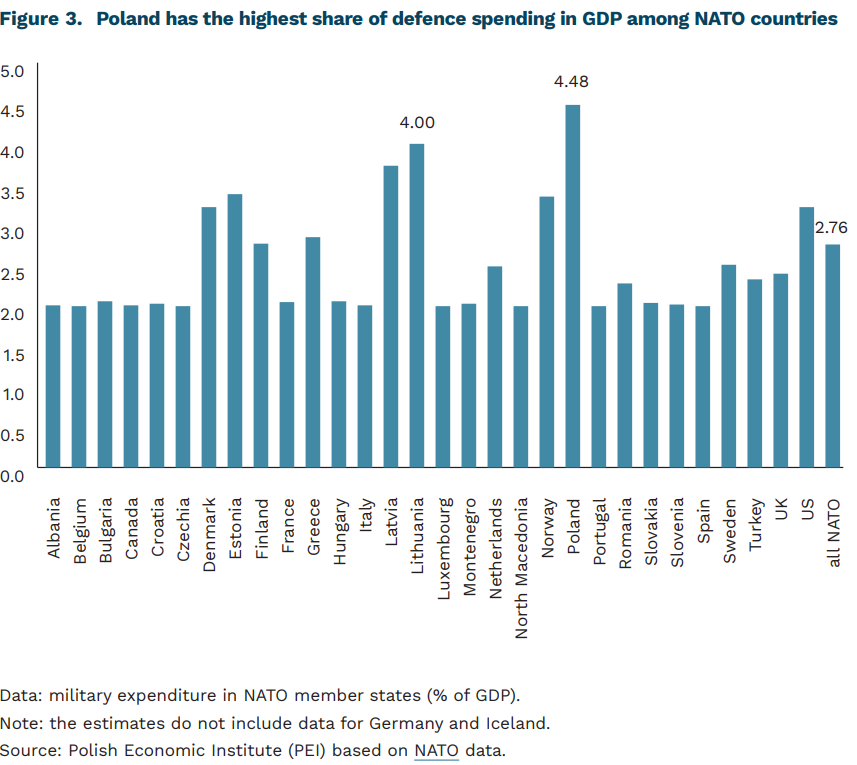

The new EU program is intended to address the most urgent defence needs of the Member States

EUR 115 million is the budget of the AGILE project

just under 4.5% of GDP is the share of Poland’s defence spending

The AGILE project is intended to complement the existing instruments supporting defence development and remain complementary to SAFE and all other existing military spending. Its role is to fill a functional gap in the EU defence support system, as it focuses on innovations of a microeconomic nature and is addressed primarily to SMEs, startups, and scaleups. This instrument is meant to provide rapid financing for technology projects at the development, testing, and deployment-preparation stages. SAFE has a macro-financial and demand-side character: it provides for up to EUR 150 billion in long-term loans for Member States intended for joint procurement and the large-scale development of defence capabilities.

EUR 115 million has been allocated to AGILE. AGILE will cover between 20 and 30 projects, offering up to 100% financing of eligible costs. The programme will also introduce a mechanism for the retroactive reimbursement of expenditures incurred up to three months before the closure of the call for applications, which is additionally intended to accelerate the pace of innovation work. This amount is meant primarily to support small and medium-sized enterprises, including startups and firms in a phase of dynamic growth.

The instrument is to be closely tailored to the most urgent needs of the European Union Member States. The aim is to ensure the innovativeness of the European defence sector and its readiness to respond immediately. The draft regulation establishing the AGILE programme is to be presented to the European Parliament and the Council of the EU. The document will be processed under ordinary legislative procedure. It is assumed that the instrument will become operational at the beginning of 2027, which is expected to enable the rapid deployment of new technologies in European armed forces.

According to NATO estimates, in 2025 Poland allocated the highest share of GDP to defence among the Alliance’s member states. Poland was also the only country in which defence spending reached nearly 4.5% of GDP. By comparison, the NATO average amounted to just over 2.7% of GDP. At the same time, many countries maintain a high share of equipment expenditure in total defence spending. Particularly high levels were recorded in: Poland (54.4%), Norway (31.4%), Spain (32.3%), as well as Lithuania (22.8%).

Jakub Kubiczek, Szymon Chudziak

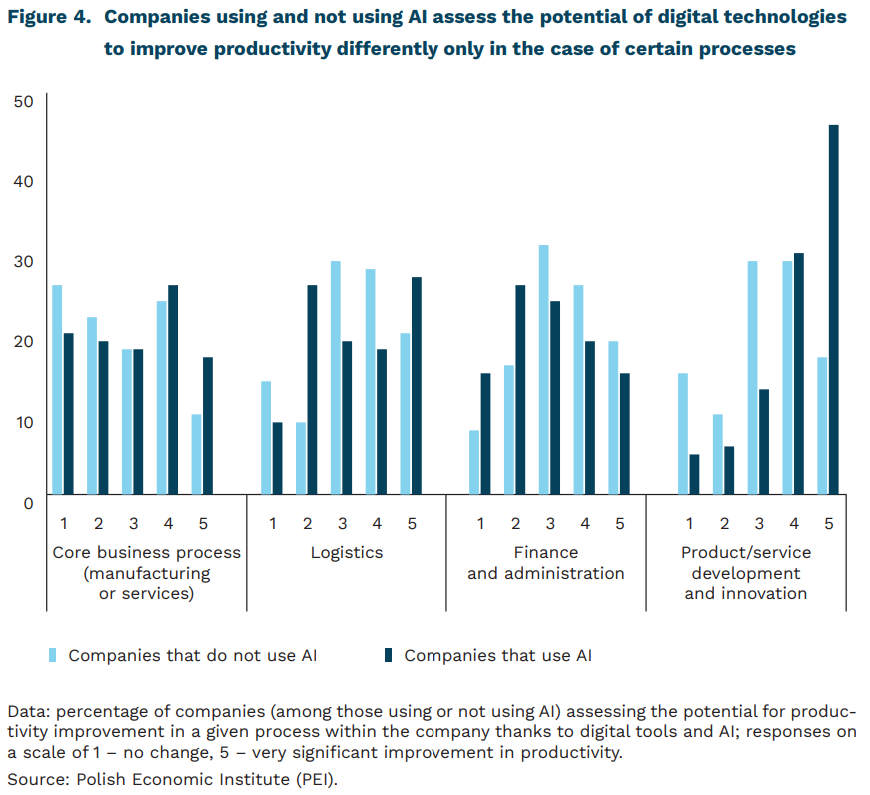

Polish companies are very optimistic about the use of AI

4.02 is the average rating for the potential to improve productivity in IT processes through digital tools and AI (on a scale of 1-5)

companies that have already implemented AI rate the potential for productivity improvements in purchasing and procurement processes at just 2.35 (on a scale of 1-5)

46% of companies that have already implemented AI rate the potential for productivity improvements in the development of new products/services through digital tools at 5

Polish companies are most optimistic regarding the use of AI to improve productivity in IT and information management processes, as well as in the development of new products, services and innovation. One in three companies surveyed by PIE[3] sees the potential to improve productivity in its core area of operation, i.e. in the production or delivery of services on which its business model is based. However, respondents rated the potential of AI in this area slightly lower than in the aforementioned processes. The average rating of the potential for productivity improvement through digital tools and AI, obtained in the PIE survey conducted at the end of last year, stands at approximately 4.02 for the first of the above areas and 3.48 for the second (on a 5-point scale, where 1 = no change, 5 – very significant improvement in productivity), whilst for the company’s core process it was approximately 2.82. Of all processes, the lowest potential for digital technologies was identified in purchasing and procurement (approximately 2.5).[4]

Significant differences in the assessment of the potential of digital solutions are evident in the assessment of certain processes between companies that already use AI technology and those that do not use such solutions. Companies declaring the use of artificial intelligence see greater potential for increasing productivity in the company’s core process, but also in new product development and innovation. Conversely, when it comes to the impact on finance and administration, the result is the opposite – it is companies without AI that believe in the potential for increased productivity (average rating 3.31) to a greater extent than companies with AI (2.94). A similar, somewhat surprising result was also observed in the case of purchasing and sales processes, although in these cases it is not statistically significant.

The difference in the assessment of the usefulness of digital tools for product and service development between companies using and not using AI was the highest of all the areas surveyed – it amounted to as much as 0.83 points. At the same time, as many as 46 per cent of companies already using AI indicated that digital tools can improve the productivity of this process to a very large extent. This result may be indicative of the potential of digital technologies as revealed in the day-to-day operations of companies. At the same time, given the low level of digital technology adoption in Poland as a whole, it may suggest a growing divide amongst businesses. The group that is quicker to embrace digital transformation, utilising new tools to create productivity-enhancing innovations, will increasingly stand out from other companies. Conversely, a significant difference in the opposite direction, in the case of financial processes, may stem from a certain disappointment with the promises behind AI – perhaps the results achieved in this area (accounting, controlling, internal communication) have not met expectations.

[3] Survey conducted on a sample of 1,000 companies in December 2025 using the mixed CATI/CAWI method.

[4] The survey asked about the following processes: the company’s core process (manufacturing or services); logistics; purchasing and procurement; finance and administration; IT and information management; product/service development and innovation; sales and marketing; HR and personnel management.

Ignacy Święcicki

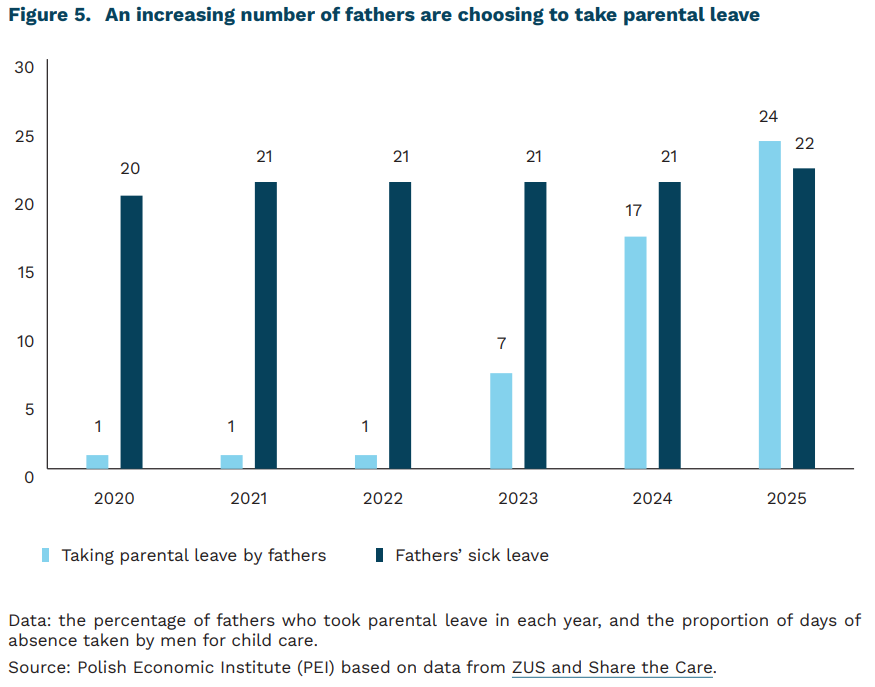

Although the care gap is narrowing in Poland, women are still primarily responsible for caring for children

24% of fathers took parental leave in 2025

17% of fathers took parental leave in 2024

78% of all absences from work due to a child’s illness were taken by women

In 2025, the percentage of fathers who took parental leave was 24%, marking a record high and a 7 percentage point increase compared to 2024. The proportion of fathers taking parental leave has been steadily increasing since 2023, when the EU Work-Life Balance Directive was implemented into Polish law. It granted each parent the right to 9 weeks of parental leave, with the stipulation that this right cannot be transferred to the other parent. In practice, this means that if the father does not take the leave, the child’s mother cannot take it.

The Work-Life Balance Directive aims to support women in the labor market by increasing men’s involvement in childcare. Research suggests that greater involvement of fathers in household and caregiving responsibilities improves women’s situation in the labor market and enables them to combine motherhood with professional development. Without fathers’ involvement, women are unable to achieve these two goals. As a result, some women give up either their plans to have children or their professional careers. Research indicates that in countries where men are not involved in household and caregiving responsibilities, the greatest differences between men and women in the desire to have another child are also observed.

Despite the increase in fathers’ use of parental leave, women still shoulder the majority of child-care responsibilities. In 2025, women accounted for 94 percent of all parental leave days taken and 78 percent of all sick days taken from work due to a child’s illness. Furthermore, in 2025, only 58% of men took advantage of the two-week fully paid paternity leave. There is strong evidence that the persistently low uptake by men of the childcare leave to which they are entitled may stem from men’s fear of negative evaluation by their employer. In a survey conducted by PIE in 2022, 60% of fathers of young children admitted that they would expect an unfavorable reaction from their supervisor if they expressed a desire to take parental leave. Meanwhile, another quasi-experimental study confirms that employers viewed the resumes of men who declared they had taken parental leave more negatively than those of men who did not report career breaks. Despite these challenges, the research suggests that fathers taking the parental leave to which they are entitled can positively impact their well-being, helping to build family bonds and overcome issues related to burnout.

Paula Kukołowicz

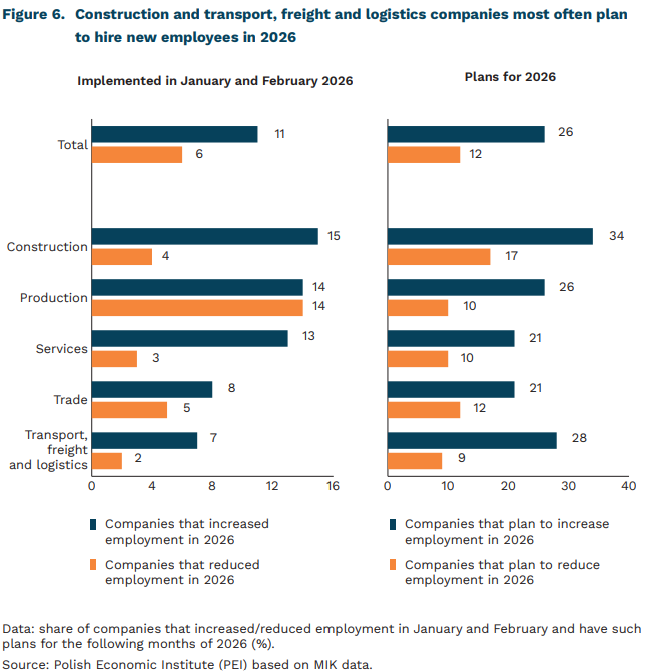

In 2026, more companies plan to hire new employees than to lay them of

11% of companies increased their workforce, and 26% want to increase the number of employees in 2026

34% of construction companies want to hire new employees in 2026

6% of companies reduced their workforce, and 12% want to reduce employment in 2026

Despite high labour costs, companies still want to hire new employees. A survey conducted by PIE as part of the Monthly Business Climate Index (MIK) shows that by the end of February 2026, 11% of enterprises had hired new employees, and more than twice as many (26%) plan to do so by the end of the year. Among companies that increased employment, as many as 77% plan to hire additional employees in the following months of 2026. By contrast, among companies that did not increase employment, 19% plan to recruit by the end of 2026.

More than one-third of construction companies plan to increase employment in 2026. This is due to the seasonality of the sector – during the spring and summer period, workers performing construction work are more in demand than in other parts of the year. Transport, freight and logistics companies also often declare plans to hire new employees (28%). Both of these sectors far more often than others indicated that problems with the availability of workers hinder their operations. According to the March MIK reading, as many as 58% of construction companies and 59% of transport, freight and logistics companies reported that labour shortages are of major or very major importance for their functioning.

Only 6% of companies reduced employment, and 12% have such plans by the end of 2026. Manufacturing companies most often decided to lay off employees – 14% of entities in this sector have already done so in the first two months of 2026, and a further 10% plan such actions in the coming months. In other sectors, indications of employment reductions are only a few percent, while such plans are usually reported by around 10-12% of companies. An exception is construction, where as many as 17% of firms plan layoffs by the end of the year, although hiring plans (34%) still outweigh layoff plans. Among companies that have carried out layoffs, 57% plan further employment reductions by the end of the year. By contrast, among those that have not taken such action so far, only 10% plan layoffs in the following months of 2026.

Rising labour costs are the main barrier to business activity, cited in the MIK survey by nearly 70% of companies, but this does not prevent firms from hiring new employees. It is true that in February 2026 registered unemployment reached a higher level than in previous months – 6.1% – but this may be due to changes in the rules for registering as unemployed. At the same time, according to the Labour Force Survey (BAEL), the unemployment rate in Poland has not fluctuated significantly and remains one of the lowest in the EU, while the number of people in employment is increasing.

Anna Szymańska