Economic Weekly 23/2026, June 12, 2026

Published: 12/06/2026

Table of contents

The European Union is strengthening its technological sovereignty

Europe’s moment of independence’ – this is how some circles have described the proposals put forward by the European Commission on 3 June, which aim to reduce Europe’s technological dependence on foreign suppliers. In recent months, the debate on technological sovereignty has become the main topic of discussion on economic policy both within the EU itself and at the level of individual Member States, including Poland. The next stage is to move on to concrete action. And this is where the EC’s package of proposals comes in, which we discuss in most of the articles in this issue of “PEI Economic Weekly”.

The proposals raised high hopes, but the history of failures and ineffective policies in this area also fuelled scepticism. The presentation of the package was postponed several times, and some proposals – such as a certification system for data centres reflecting their environmental impact – were dropped from the final text. As a result, the Commission presented two proposals for regulations – the Cloud and AI Development Act (CADA) and the Chips Act 2.0 – as well as a strategy to support open-source software and a Strategic Roadmap for Digitalisation and AI in Energy.

The Commission is attempting to combine several distinct elements into a single package: building its own digital technology ecosystem; maintaining openness to international cooperation; and integrating technological development into sustainable development goals. On the one hand, this is a response to changes in geopolitics, the weaponisation of technology and its use as a tool of pressure, but it also aligns with the direction set by Ursula von der Leyen’s second Commission, which has emphasised the importance of technological sovereignty from the outset. On the other hand, the ‘sovereignty’ narrative must be tempered by the ongoing trade negotiations with the US; communications constantly emphasise that the new rules are not directed against any specific country, do not aim at isolation or protectionism, and that the entire process fits within the existing framework of ‘open strategic autonomy’. In turn, the EU’s “green” policies are utilised both as a resource (advanced energy transition projects and renewable energy sources provide data resources and the opportunity to develop proprietary AI models and promote standards), and as a lever for development – the certification of data centres and the promotion of energy-efficient processors are intended to act as a lever for the development of the European technology sector.

In ‘PEI Economic Weekly’, we describe only some of the solutions that make up these comprehensive objectives:

- proposals for cloud computing certification;

- the use of AI in the energy sector, particularly the role of smart meters (both in terms of potential benefits and behavioural challenges on the part of users);

- Poland’s trade dependencies in the microchips sector (as part of the diagnosis, a starting point for actions under the Chips Act 2.0).

It is also worth highlighting the convergence of the EC’s proposals with initiatives promoted by PEI in previous years. The Commission proposes an approach based on ‘grand challenges’ – long-term, complex projects designed to utilise the scientific base to stimulate demand for new solutions, whilst also addressing real societal problems. This is an extension of innovative public procurement, also mentioned in the document. It also identifies the energy sector as a priority area for the development of European AI. We presented such solutions a year ago in our work on the Polish strategy for the development of artificial intelligence.

Ignacy Święcicki

The European Commission proposes specific criteria for sovereign cloud computing services

15% share of European companies in the EU cloud computing market

4 number of union assurance levels proposed for cloud services in a new regulation by the European Commission

3 full-time positions will be needed to ensure compliance with the new regulations on the part of service providers

In its proposal for the Cloud and AI Development Act, the European Commission has proposed four levels of assurance (read: sovereignty) for cloud computing service providers. This is yet another attempt to introduce standards for public procurement in the EU regarding data storage and processing in the public sector. Previous attempts were either blocked at the legislative stage (the European Cybersecurity Certification Scheme for Cloud Services – EUCS) or used only to a limited extent (the 2025 Cloud Sovereignty Framework used by the EC in a single tender so far). However, previous proposals were not intended to be mandatory for contracting authorities, whereas this time the proposed criteria have been included in a proposal for a regulation – a directly applicable legal act.

The new criteria would apply to procurement by public entities in EU Member States and EU institutions. Higher assurance levels (2-4) would be required for services critical to the maintenance of public order (in accordance with the annexes to the NIS 2 Directive), with the lowest level applying to other services. Member States would also be required to conduct a risk assessment of their systems and, on that basis, assign services to the new security levels. If these provisions come into force, this will entail changes to new contracts as well as a potentially large-scale migration of services and data from currently used systems to new providers offering services compliant with sovereignty requirements. The EC estimates that around 20% of services will require the second assurance level, 9% the third, and 1% the fourth level.

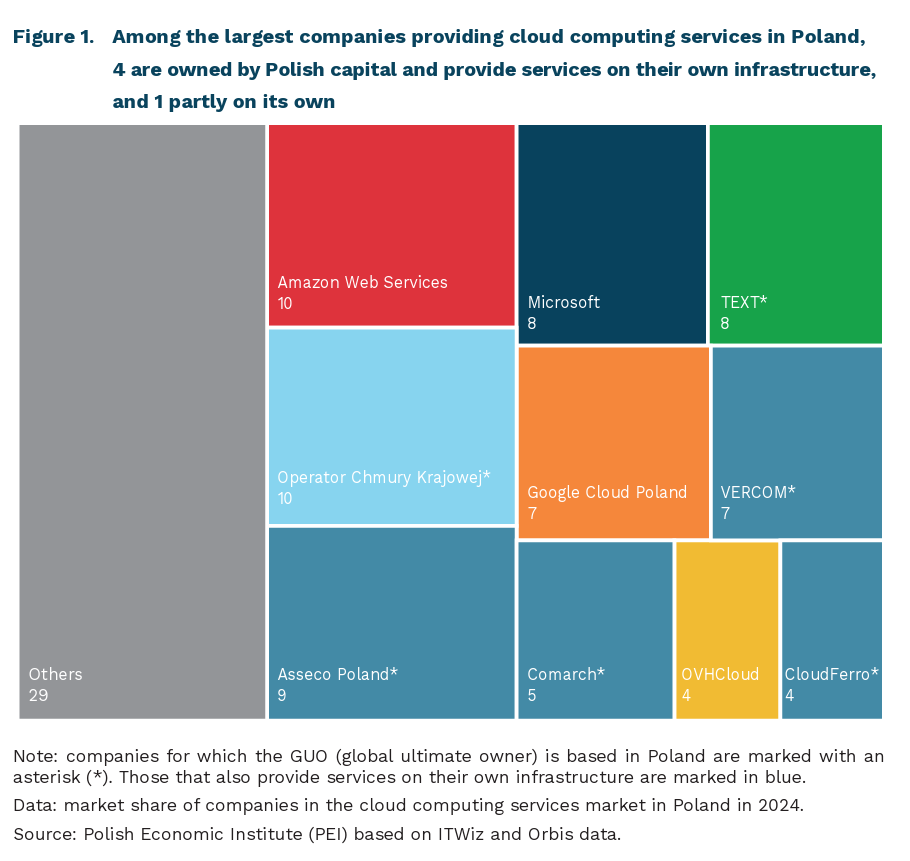

In its regulatory impact assessment, the EC indicates that only services fully controlled by EU entities will be able to ensure the highest levels of security – US providers are suitable for Level 1 or, if operating as part of a consortium, for Level 2. The main criterion for sovereignty is the geographical criterion – the provider’s registered office and the location where data is stored, and at higher levels also the subcontractors and staff involved in providing the service. The control also covers supply chains, including software subcontractors. Such restrictions naturally generate costs for providers (estimated at 3 full-time equivalents per year, plus the costs of the required audit), but the benefit is expected to be an increase in contracts for European companies, which will in turn allow them to capture a share of the large and rapidly growing cloud computing market. It is estimated that only around 15% of the cloud computing market in the EU is held by European suppliers. In Poland, according to market estimates, the figure was slightly higher in 2024 – among the ten largest providers, four are Polish-owned and provide services on their own infrastructure, and one provides services under a hybrid model (own infrastructure and the sale of other providers’ services).

The EC’s new proposals have been long awaited, and strengthening sovereignty is a desirable course of action – both from a security and an economic perspective. However, much depends on legislative work and the determination of Member States. The regulation already provides for the possibility of creating exceptions, so it is to be expected that the proposed rules will be the subject of active lobbying (from both European and non-European companies).

Ignacy Święcicki

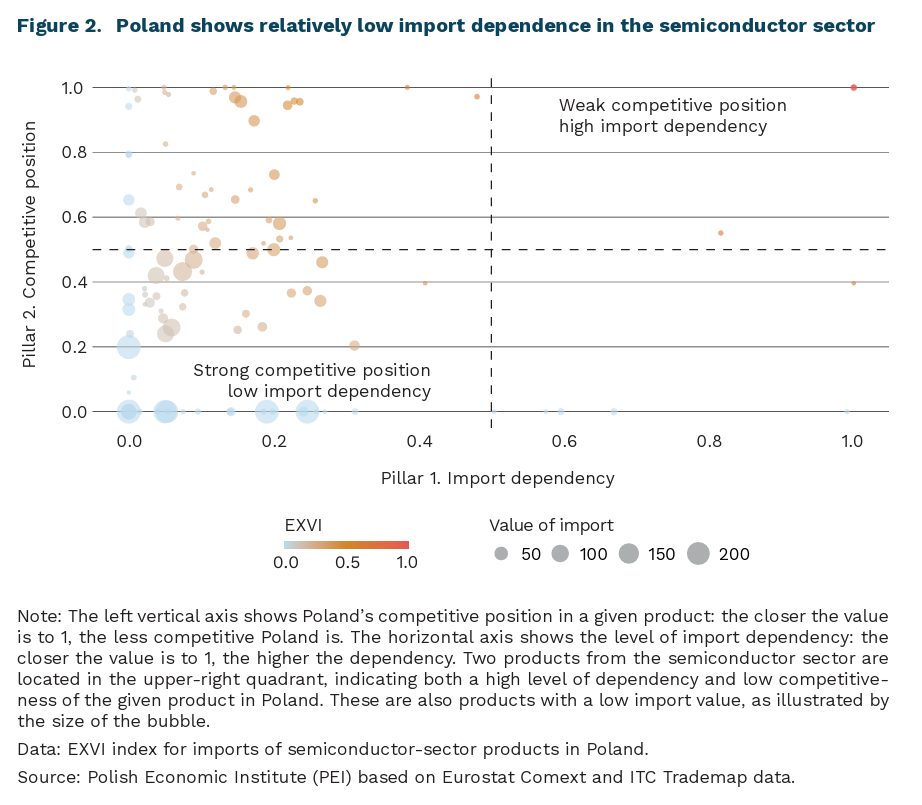

Poland’s dependencies in microprocessors are among the five lowest in the EU

in 10 out of 57 products in the microprocessor sector, China is the main partner in 2025

4 products in the microprocessor sector show a critical dependency

4.3% is Poland’s share in the value of EU imports of products and intermediate goods from the microprocessor sector

In the microprocessor sector, Poland relies much more on finished products and lacks a developed production chain – this is the conclusion drawn from the analysis of trade data. Poland primarily imports finished microprocessors – as much as 75% of Poland’s imports in the microprocessor sector consist of products classified as final goods, of which 60% are various types of integrated circuits [1]. Imports of these products are relatively diversified. Among these products, imports are relatively diversified – the EXVI [2] (External Vulnerabilities Index), which combines measures of dependency and competitiveness in a given product, is close to zero, indicating a low level of dependency. Their main suppliers are other European countries. The only finished microprocessor product showing a high level of dependency in Poland’s imports is integrated circuits in the form of amplifiers, often used in audio systems or telecommunications. The EXVI index for these products is 0.45, but this dependency is on the Netherlands, meaning it is insignificant from a security perspective.

Poland records a high level of dependency in raw materials. For three materials used in the semiconductor sector, we identified a high EXVI dependency index in Poland, above 0.4, while one intermediate product was close to 0.4. However, these goods together account for less than EUR 40 million, or 0.1% of the value of Poland’s imports of products from the sector. The highest level of dependency concerns imports of two raw materials with a combined value of only EUR 4 million in 2025.

Poland’s average dependencies among microprocessor-related products are the fifth lowest in the EU. In 2025, Poland’s average EXVI score stood at 0.18, compared with 0.22 for the EU. Interestingly, taking into account Poland’s potential indirect imports (through other Member States) in this sector does not increase dependence on non-EU countries. In only two cases does the inclusion of indirect intra-EU flows within this sector lead to a change in the main supplier – in one case to China, and in the other to South Korea. However, in neither case do the values exceed the thresholds indicating the criticality of these import dependencies.

Economic security policy is intended to protect Poland and the EU against the risk of supply-chain disruptions. According to the WSTS forecast, the value of the European semiconductor market will increase by 6.1% in 2026, reaching USD 56.2 billion. The Chips Act 2.0, proposed last week, envisages deeper support for the sector than before, not only at the level of semiconductor production, but also through the protection of the entire production chain. This includes support for demand for European chips, as well as shortening and streamlining permitting procedures to twelve months for semiconductor-sector investments. These measures are necessary because, at the current level of investment, the EU’s share in global semiconductor production may increase to only around 11.7% in 2030, rather than the 20% targeted in the 2023 Chips Act. In Poland, the photonics segment is developing particularly strongly, and this is likely where potential benefits for Poland may be found.

- The HS codes used in this analysis are from: OECD (2025).

- In the case of the EXVI index, the results are given in the range from 0 to 1. More about the EC methodology: https://single-market-economy.ec.europa.eu/publications/external-vulnerability-index-exvi_en

Katarzyna Sierocińska, Marek Wąsiński

The European Commission is betting on the further deployment of AI in the energy sector

by 40% the European Commission ultimately wants to increase the transmission capacity of power grids using AI

USD 110 billion per year the potential global savings in 2035 from applying AI to power-plant operation and maintenance

9.5 million smart meters installed in Poland as of the end of 2025

One of the most important elements of the Strategic Roadmap for the Digitalisation and Artificial Intelligence of the Energy Sector is the use of AI in developing the power system, especially smart grids. In the document, the European Commission highlights the need to make grids resilient to climate change and to unexpected events such as natural disasters, by using geospatial data and artificial intelligence. This can be achieved, among other ways, through smart metering systems that can enable demand-side response, and through electricity tariffs with dynamic pricing.

One of the key goals set by the Commission is to reduce grid-expansion costs by 35% [3] and to increase grid transmission capacity by up to 40% [4]. In addition, in 2026-2027 the Horizon Europe programme will allocate EUR 75 million to AI technologies in the energy sector – in particular for grids, self-consumption, energy sharing and grid-scale energy storage – as well as additional EUR 190 million for broader digital solutions in the areas of renewable energy, building renovation and energy efficiency.

The Commission also stresses the need to train AI models on European data for the energy sector. One initiative in this area is AI.Grids, which aims to create the first shared artificial-intelligence model serving the needs of interconnected power systems, and which was also joined in early May this year by Polskie Sieci Elektroenergetyczne (PSE, Poland’s transmission system operator).

Optimal management of the power system requires the widespread adoption of smart meters, which automatically transmit energy-consumption data to the operator. The European Commission plans to present minimum installation targets for each EU country in the second half of the year. This, in turn, allows for wider use of dynamic tariffs and the introduction of additional system-management mechanisms, such as vehicle-to-grid5. In Poland, as of the end of 2025, 9.5 million such meters were installed – in almost half of all Polish households.

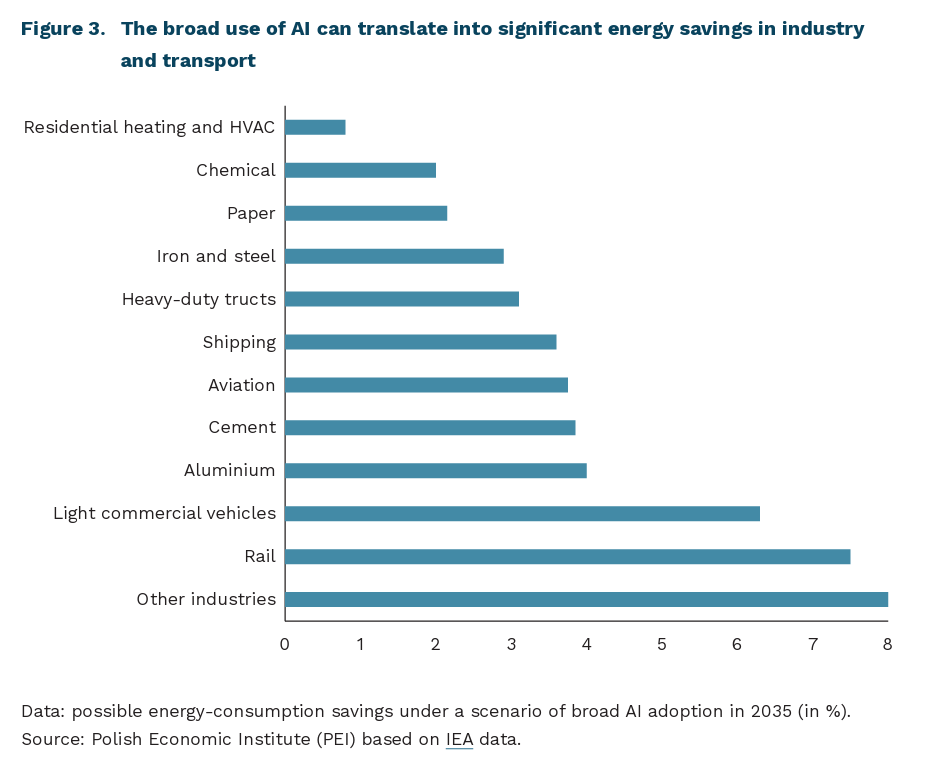

The broad use of AI in the energy sector is one of the most promising areas for the development of this technology. According to the International Energy Agency (IEA), the widespread deployment of AI in power-plant operation and maintenance could, by 2035, deliver potential global savings of up to USD 110 billion per year, by avoiding part of the fuel consumption and lowering operating costs. AI will also enable greater integration of renewable electricity into the grid, which could unlock up to 175 GW of additional transmission capacity on existing lines. Reductions in energy consumption of a few percent can also be achieved in industry and transport with the help of AI-assisted systems.

AI support also significantly improves the accuracy of day-ahead energy-demand forecasts – by 15% to 25%. This, in turn, can translate into an increase in the output of photovoltaics and wind farms of 12-20%. Advanced AI-based systems also assist in monitoring the condition of critical energy infrastructure, which makes it possible to reduce outage durations caused by faults by up to 50% and to lower renovation and repair costs by 10% to 40%.

The Strategic Roadmap for the Digitalisation and Artificial Intelligence of the Energy Sector aligns with global trends in optimising power systems using AI. The adoption of comprehensive new public policies in this area is essential, especially in the face of energy prices for energy-intensive industry that are higher than in the US and China, and of ambitious climate targets whose achievement is to be based largely on non-dispatchable renewable energy sources.

3. According to CurrENT Europe, whose calculations the Commission relies on, the investments required in power grids – if innovative grid technologies (IGTs) are not deployed at large scale – could, by 2040, amount in Europe to around EUR 1,000 billion in transmission grids and around EUR 1,000 billion in distribution grids. Deploying innovative grid technologies would make it possible to reduce the need for expansion by about 35%, which would translate into savings of around EUR 700 billion (not counting the expenditure on smart-grid-related improvement investments).

4. This is possible thanks to the use of systems such as Dynamic Line Rating (DLR). This solution allows for a variable assessment of a line’s permissible loading, based on local conditions rather than on fixed design assumptions.

5. The bidirectional electric-vehicle charging technology, vehicle-to-grid, makes it possible to use electric cars as additional batteries for the power system, which can feed electricity back into the grid. Besides making a significant contribution to energy security (with a fleet of several million battery vehicles, just 100,000 available at any given moment are enough to provide power comparable to a nuclear power plant), this solution is also expected to translate into savings for electric-vehicle users (from EUR 450 to nearly EUR 3,000 per year).

Adam Juszczak

The European Commission seeks to accelerate the deployment of smart metres

One of the tools proposed in the Strategic Roadmap for Digitalisation and Artificial Intelligence in the Energy Sector is to accelerate the rollout of smart meters, which enable consumers to monitor their energy consumption and can help reduce electricity bills. The European Commission has announced that later this year it will present legislative proposals establishing quantitative targets for Member States regarding the minimum level of smart meter deployment. Smart metering systems are crucial for enhancing demand-side flexibility and enabling consumers to enter into dynamic electricity price contracts.

Research suggests, however, that access to smart energy-monitoring technologies alone does not necessarily encourage consumers to adopt more energy-efficient and, consequently, less costly patterns of electricity use. While dynamic tariffs provide incentives to shift consumption to periods when electricity prices are lower, doing so requires changes in habits and routines that do not occur automatically. Consumers are often either unwilling or unable to monitor their electricity use on a regular basis. In addition, concerns about the accuracy of measurements and the security of the data collected by smart meters may constitute barriers to their large-scale deployment.

To achieve more efficient energy use, feedback and personalized guidance on how to optimize consumption within a given household are essential. Electricity bills – particularly electronic ones – remain the most common form of feedback. Additional monitoring tools and technologies, such as smartphone applications, can also be helpful by providing detailed information on which appliances consume the most electricity and at what times of day. A number of studies conducted in the United States have shown that the use of smart meters combined with supplementary monitoring devices can reduce peak electricity demand by 27-44%. Behavioral messages also play an important role, including those that appeal to social norms or highlight the public health benefits of energy conservation.

Electricity bills are received by all consumers and therefore constitute a key channel for effective communication and for providing additional incentives to use electricity more efficiently. A successful reform aimed at improving bill transparency and equipping consumers with easily understandable information on how to reduce their energy costs was implemented in Australia several years ago. Among other changes, electricity bills were required to include a prominent question: “Could you save money on another plan?” together with a reference to a website offering clear comparisons of available plans and suppliers. The reform helped engage consumers who had previously been passive in the energy market and increased their sense of control over the costs they incur.

The Polish Ministry of Energy has also taken steps to simplify electricity bills. However, it may be worth considering complementing the proposed changes with additional behavioral tools that would not only make the information provided to energy consumers easier to understand, but also – following the Australian example – offer clear guidance on the actions consumers can take to reduce their energy costs.

Agnieszka Wincewicz-Price

Digital sovereignty is becoming crucial for the collection of data on international migration

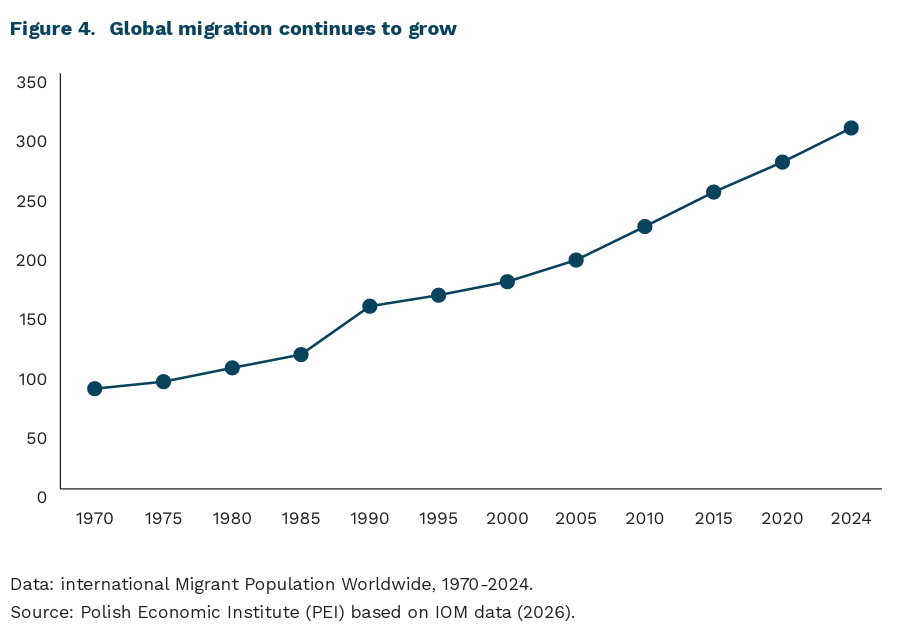

304 million international migrants worldwide in 2024 (3.7% of the global population)

EUR 376 million in EU funding for AI-related projects in border management and customs controls

EUR 81 billion proposed for migration, border management, and security under the EU’s 2028-2034 Multiannual Financial Framework

Migration control is no longer based solely on the regulation of state borders; instead, the governance of data is becoming increasingly important. Digital systems, databases, and artificial intelligence have emerged as key tools for managing human mobility, shifting the focus of migration policy toward information infrastructures. According to the World Migration Report 2026, the number of international migrants reached 304 million in 2024, although their share of the global population remained relatively modest at 3.7%. At the same time, the importance of sudden and large-scale migration movements driven by armed conflicts, climate change, and humanitarian crises is increasing. These developments require the creation of systems capable of rapidly collecting and processing data, facilitating the relocation of migrants, and monitoring their integration and adaptation processes.

A key transformation is taking place in the governance of migration. The European Union is developing extensive digital ecosystems, including SIS, VIS, Eurodac, EES, ETIAS), which collect visa information, biometric data, and records of border crossings. Increasingly, these systems are used not only to record and store information but also to support risk assessment, identity verification, and the detection of irregularities. Their interoperability, enables the real-time exchange and integration of data, while decisions regarding entry and mobility are increasingly supported by algorithmic analysis. Systems such as ETIAS and EES are becoming the digital equivalent of traditional passport control, reflecting a broader shift toward data-driven migration management.

The scale of investment underscores the importance of this policy direction. Between 2015 and 2024, the European Union funded 75 research projects related to the use of artificial intelligence in border management and customs controls, with a total budget of approximately €376 million. In the proposed EU Multiannual Financial Framework for 20282034, around €81 billion has been earmarked for migration, border management, and security, including approximately €34 billion dedicated to the direct management of migration flows. These investments support the development of technologies and systems for automated risk assessment, identity verification, and the detection of irregularities, among other applications.

The expansion of digital infrastructure is making digital sovereignty an increasingly important dimension of both national and European security. The European Commission has emphasized the need to reduce dependence on external technology providers and to strengthen strategic autonomy in the development and deployment of key digital technologies, particularly in areas of public and strategic importance. This includes systems for the collection, storage, and processing of data on migrants and migration flows. As a result, migration governance is becoming increasingly data-driven and reliant on digital technologies.

This reflects a broader transformation in the understanding and governance of migration. The ability of states to regulate migration flows increasingly depends not only on the control of territorial borders, but also on the governance of data, algorithms, and digital infrastructures. Consequently, technological sovereignty has become a critical factor influencing the effectiveness of contemporary migration policy.

Katarzyna Zybertowicz

The European Union reconciles fiscal rules with spending on defence and energy

0.3% of GDP is the annual limit proposed by the European Commission for energy expenditure covered by fiscal flexibility

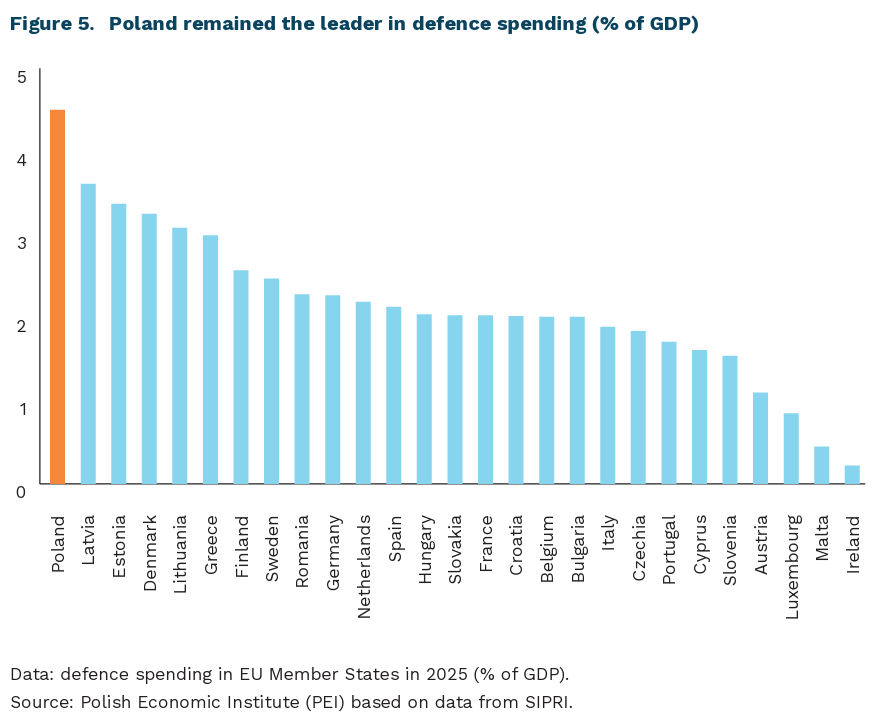

4.5% of GDP was Poland’s defence spending in 2025

EUR 14.5 billion was the cost of shielding measures introduced by EU Member States in response to high energy prices since the escalation in the Middle East

Alongside the economic analyses published as part of the European Semester, the European Commission proposed expanding the exemptions from fiscal rules to include spending on decarbonisation. Member States could therefore, upon request, use this fiscal space to reduce their dependence on imported fossil fuels, including by supporting investments in storage facilities and clean energy sources. The need for such flexibility stems from the rising cost of shielding measures following the outbreak of the war in the Middle East, estimated at EUR 14.5 billion, or 0.07% of EU GDP. At the same time, the Commission notes that fiscal safeguards remain in place, while energy expenditure would be subject to a separate ceiling of 0.3% of GDP per year in 2026-2028 and 0.6% of GDP in total.

In recent years, defence spending has also become a particularly significant burden on Member States’ budgets. The Commission stresses that strengthening defence readiness is no longer a temporary response to a crisis, but one of the lasting priorities of economic policy. In 2025, EU Member States spent an average of 2.2% of GDP on defence, while Poland was the regional leader in armaments spending relative to GDP, at 4.5% of GDP. Latvia (3.6%), Estonia (3.4%) and Denmark (3.3%) were also among the top performers. In practice, however, this means additional pressure on public finances, especially in countries that are simultaneously financing the energy transition and social policy.

Defence spending has already been covered by additional flexibility under EU fiscal rules. The Commission maintains the national escape clause for defence expenditure, which does not exclude this spending from the deficit, but allows it to be treated more leniently when assessing Member States’ compliance with EU fiscal rules. This flexibility is limited to 1.5% of GDP in additional expenditure in 2025-2028. The clause therefore creates a buffer for spending deemed strategic.

The changes to EU fiscal rules therefore represent a loosening of the rules, but with restrictions maintained. They seek to reconcile budgetary discipline with Europe’s new security priorities: defence and energy resilience amid unstable energy prices and rising geopolitical tensions. The key issue will therefore be not only how much Member States spend, but above all what they allocate the additional fiscal space to. The Commission is trying to distinguish between spending that permanently worsens the state of public finances and spending that strengthens security, reduces strategic dependencies and increases the resilience of the European economy.

Piotr Kamiński

Hosting the World Cup is becoming too expensive for a single country

On June 11, 2026, the 23rd FIFA World Cup will kick off in the United States, Mexico, and Canada – the first tournament of its kind to be hosted by three countries. Previously, the World Cup had been organized by more than one host country only once in history – in 2002, when Japan and South Korea co-hosted the tournament. Of this year’s hosts, two have previously hosted the event as sole hosts: the United States in 1994 and Mexico in 1970 and 1986.

It is already clear that the 2026 tournament will be no exception in terms of its organizational model. The next championship – in 2030 – will also be hosted by three countries: Spain, Portugal, and Morocco, whose bid competed against a joint bid from Argentina, Uruguay, and Paraguay [6]. Thus, a trend is evident that has been observed for some time in the case of the UEFA European Football Championship – namely, the joint organization of the tournament by several countries (looking only at future events: the next two editions will be hosted by the United Kingdom and Ireland in 2028 and Italy and Turkey in 2032). This trend will also be reinforced by FIFA’s decision to increase the number of participating teams.

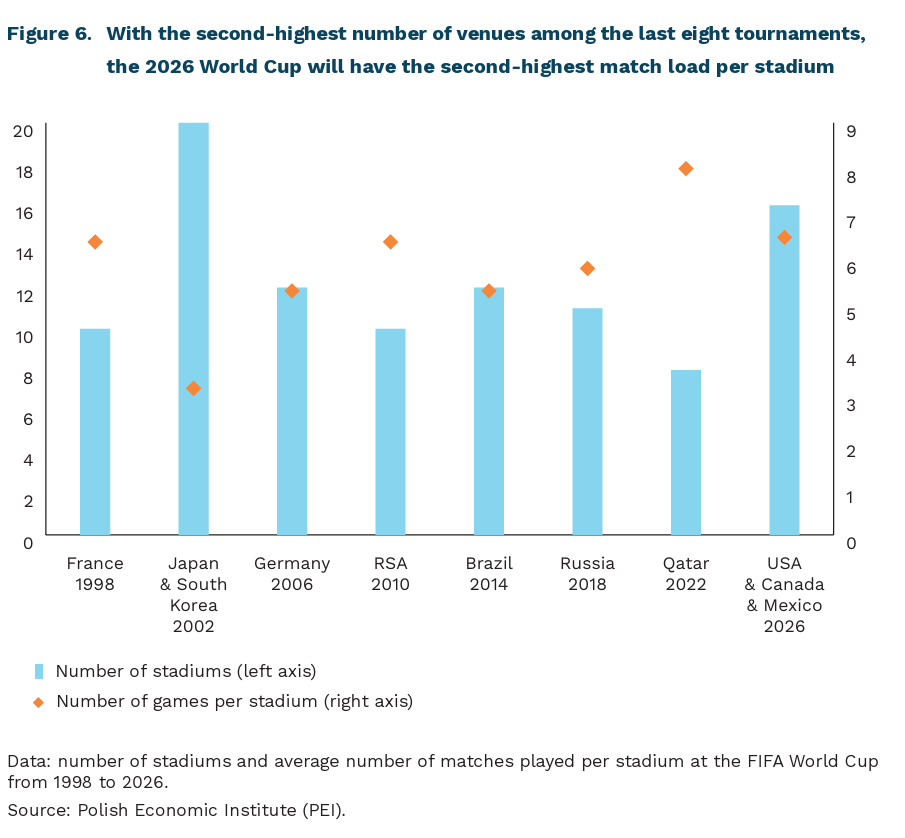

Starting this year, 48 teams will compete in the World Cup, which means higher costs and greater logistical challenges for current and future organizers. This represents an expansion of the format in place since 1998 by 16 teams. When 32 teams were participating in the World Cup, organizers typically used 12 stadiums. In that configuration, each stadium hosted an average of 5.4 matches. At this year’s World Cup, 104 matches will be played across 16 stadiums, which will mean 6.5 matches per stadium. This shows that even with the addition of four venues, the workload on stadiums and host cities in this year’s tournament will be greater than the average over the past two decades. In recent years, the only tournament with more matches per stadium was the 2022 World Cup in Qatar (which was held at just 8 stadiums).

It is estimated that the 2026 World Cup will cost approximately USD 14 billion, of which USD 11 billion will be covered by the United States, which will host 75% of all tournament matches. If this forecast proves accurate, it will be the third most expensive World Cup after the 2022 tournament in Qatar and the 2014 tournament in Brazil [7]. Unlike previous World Cups, hosting the 2026 World Cup did not require the construction of new stadiums and will rely on existing facilities. However, the costs of organizing such a tournament include not only stadium construction but also adapting existing infrastructure to FIFA requirements, as well as costs related to logistics, security, and providing fan zones.

In the coming years, we can expect to see more joint bids to host the championships. On the one hand, this will be driven by the expanded tournament format and the need to secure enough stadiums meeting specific standards; on the other hand, by the desire to spread the costs and risks associated with hosting such an event. For these reasons, among others, bidding as a co-host will be more attractive for many countries, and in some cases will be the only option. The mere fact that joint bids are becoming more common does not mean that individual countries will not be selected as hosts. Tournaments such as the FIFA World Cup will continue to be used by some countries to improve their international standing, enhance their prestige, and sometimes also improve their image through so-called “sportwashing”. A case in point is Saudi Arabia, which is set to host the World Cup in 2034.

6. Ultimately, FIFA decided that the World Cup would be hosted by Spain, Portugal, and Morocco, while, to mark the tournament’s 100th anniversary, one match each would be held in Argentina, Uruguay, and Paraguay.

7. According to various sources, the World Cup in Brazil cost approximately USD 15 billion, in Russia USD 12 billion, and in Qatar USD 220 billion.

Jędrzej Lubasiński